Research Article: 2021 Vol: 25 Issue: 1

Assessment of Environmentally-Oriented Stakeholders Coherent Security as a Prerequisite of Sustainable Enterprise Development and the Role of Non-Financial Statements in that Regard

Mishchuk Ievgeniia, Kryvyi Rih National University

Nusinov Volodymyr, Kryvyi Rih National University

Polischuk Serhii, Igor Sikorsky Kyiv Polytechnic Institute

Kutova Nataliia, Kryvyi Rih National University

Stolietova Iryna, Kyiv National University of Trade and Economics

Abstract

The article aims to assess coherent security of environmentally-oriented stakeholders as a prerequisite of sustainable enterprise development and determine the role of non-financial statements in that regard. Cost minimization is considered to be one of the directions of economic growth of an enterprise. However, environmental expenditures are an exception. It is substantiated that financing environmental actions is of greater interest for individual groups of stakeholders than for the enterprise as an economic entity. There are suggested methodological approaches to assessing impacts of outstanding environmental expenditures of the enterprise on coherent (dependent on its activity) security of environmentally-oriented stakeholders. These expenditures are the difference between the amount of financing required to enhance the environmental conditions at the enterprise location and the actual amount financed for environmental programmes. Ukrainian mining and concentration enterprises-polluters do not prepare non-financial statements and therefore they do not provide complete information on amounts of environmental expenditures. As a result, impacts of their activities on the environment cannot be adequately determined. It is suggested to enhance the current form of “Management report” through disclosing information on outstanding environmental expenditures and specific emissions of pollutants. Data of Ukrainian mining enterprises has enabled testing the suggested methodological approaches. Implementation of the suggested methodological approaches into practices of industrial enterprises will extend their managerial analytics with data on impacts of environmentally-oriented stakeholders’ coherent security. The above is important for understanding possible pressure from this group of stakeholders and hindrance to economic development of enterprises in the medium and long term.

Keywords

Security, Environmentally-Oriented Stakeholders, Outstanding Environmental Expenditures, Mining Enterprises, Non-Financial Statement.

Introduction

According to the United Nations Framework Convention on Climate Change, human activities have caused significant growth of greenhouse gas concentrations in the atmosphere which lead to increase of the greenhouse effect and may lead to additional warming of the Earth’s surface and atmosphere, impact negatively natural ecosystems and humanity (United Nations Framework Convention on Climate Change, 1992). The documents of the IPCC state that compounds belonging to “greenhouse gases” (first of all, carbon dioxide and methane) are the largest contributors to Summary for Policymakers (Climate Change, 2007). Indeed, atmospheric air is one of the most important natural resources and environmental conditions and human health depend greatly on its quality. So, regular diagnostics of industrial enterprises’ impacts on the environment and atmospheric air quality should become one of priorities of their sustainable development.

Among security scientists, the prevalent approach is identification of environmental security of the enterprise as a separate type of economic security. The notion “environmental component” of economic security of the enterprise is widely used now. However, in practice, in most cases enterprises are forced to finance environmental measures by corresponding national and local normative legal acts and the community. It should be noted that it is enterprise employees and local communities in the neighborhood that are first interested in the enterprise financing these measures. Local and governmental institutions represent the interests of the employees and the community. They together form a chain of environmental security stakeholders. We suggest the name environmentally-oriented stakeholders for the latter. So, unlike other existing approaches that consider environmental security of enterprises, we suggest considering coherent (i.e. dependent on activities of a particular enterprise and, in its turn, impacting it) security of environmentally-oriented stakeholders. This approach shifts the focus from the enterprise to those subjects who are really interested in financing environmental measures and programmes. In our opinion, appropriate methods of assessing consequences of inadequate financing of environmental protection measures by enterprises can be developed on the basis of the suggested approach.

In European countries, preparation and publication of non-financial statements are regulated and controlled by the government. Ukraine faces the opposite situation. On the one hand, the country endorses important UN-sponsored international documents on corporate social responsibility and sustainable development (Rio Declaration on Environment and Development, 14 June 1992; the Programme for the Further Implementation of Agenda 21 adopted by the UN General Assembly, 28 June 1997; Report of the World Summit on Sustainable Development, 4 September 2002; Resolution A/RES/66/288 “The future we want” adopted by the UN General Assembly, 27 July 2012; Resolution A/RES/70/1 “Transforming our world: the 2030 Agenda for Sustainable Development” adopted by the UN General Assembly, 25 September 2015, etc.). On the other hand, there are no relevant organizational and institutional preconditions for their implementation in Ukraine.

The research aims to assess coherent security of environmentally-oriented stakeholders as a prerequisite of sustainable enterprise development and determine the role of non-financial statements in that regard.

Literature Review

Foreign scientific economic developments focus on the enterprise as a key object of study at the microlevel (Laplume et al., 2009; Mcconnell et al., 2009). In spite of the fact that foreign researches have long been suggesting ways of reaching success in entrepreneurship on the basis of growth and challenges of the XXI century (Davidsson et al., 2003, ?.315; Druker, 2012), interconnections between enterprise economic security and the level of satisfaction of stakeholders’ ecological interests (eco-interests) still remain uncovered.

Development of the managerial paradigm has enabled understanding of importance of a scientifically substantiated approach to restructuring the enterprise management system (Drlja?a, 2015, ?.78; Tiller, 2012, ?.20), but stakeholder-oriented management and development of corresponding security provision models are still unaddressed.

Studies of security issues in foreign scientific literature can be reduced to two directions. The first one describes security of households (The Aspen Institute, 2019) but environmental issues are not touched upon there either. The other direction deals with thorough and comprehensive coverage of national security where environmental security is one of the components (Tamoši?nien? et al., 2015). Foreign researchers do not identify enterprise security as an independent direction. Instead, risk-management related to it is widely dealt with (Giannopoulos, 2012, ?.12; Ianioglo, 2016). Economic events of recent decades have led to deceleration in all economic spheres in East European countries. That is why; representatives of these countries have started addressing economic security at the enterprise level as a separate branch of knowledge (Susca, 2018, ?.18). However, environmental security issues as a component of economic security of the enterprise (the microlevel) are not practically dealt with in such researches. While developing the policy of enhancing environmental security, assessment of its level is one of the initial stages. Various indicators are used for this purpose. These indicators obviously possess various contents at different levels of the economic security hierarchy: some on the international level, some – on the governmental and regional level and some on the level of enterprises. In particular, the United Nations Commission on Sustainable Development (CSD), International Institute for Sustainable Development (IISD, the Scientific Committee on Problems of the Environment (SCOPE), world-famous universities (in particular, Yale University) are involved in development of such indicators on the international level. In Ukraine, there is no consistent approach to complex assessment of the environmental security level. The same situation remains for the micro level as well. Enterprises whose production activities deteriorate environmental situation in cities do not have a consistent approach either.

Lack of a dialogue with society resulted from non-disclosure of relevant information in non-financial statements is the factor that adds to negative effects from enterprise activities. This can be explained by the fact that statements of this kind are mainly prepared by large international companies but not by national enterprises.

The above said conditions need for specifying indicators and developing methods to assess impacts of enterprise activities on the level of satisfaction of environmentally-oriented stakeholders’ eco-interests.

Methodology

Coherent security of environmentally-oriented stakeholders can be characterized by the level and the state of satisfying their eco-interests associated with activities of the enterprise. The level and the state are described by a numeric value and a corresponding term-set. Indicators of the level of satisfaction of environmentally-oriented stakeholders’ eco-interests are values of outstanding environmental expenditures as of a certain date.

In our opinion, these expenditures are formed in the following directions (Mishchuk, 2020):

As the difference between amounts of financing of actually fulfilled environmental measures (programmes) (FEpr). Here arises the task of finding environmental programmes that are necessary from the stakeholders’, not the enterprise’s, point of view. There are many developed and implemented environmental programmes in Ukrainian cities. For instance, “The city programme for solving environmental problems and enhancing environmental conditions in the city of Kryvyi Rih for 2016-2025” allows for 48 actions in the field of atmospheric air protection and enhancement to be fulfilled by the enterprises. However, every year some of the programmes remain unfulfilled. The situation should be taken into account that the number of programmes planned by an enterprise as well as the amount of expenses of their funding (FEpl) appears smaller than necessary (FEnes). In this case, the following condition should be fulfilled:

FEpl ≥ Fenes, (1)

As the difference between calculated environmental amounts that could be paid by the enterprise according to foreign environmental legislation and amounts of environmental payments paid according to Ukraine’s legislation. For instance, the amount of outstanding environmental tax (ΔF?t) is suggested to be calculated as follows:

ΔF?t = ETfor – Etukr, (2)

Where ET for is the amount of the environmental tax calculated according to foreign environmental legislation, c.u.;

ETukr is the amount of the environmental tax calculated according to the Tax Code of Ukraine, c.u.

It should be noted that it is expedient to choose foreign legislation with the strictest environmental requirement as a pattern. Currently, Ukrainian enterprises are facing high-level requirements to observe the EU law. Besides, as a separate case, it is reasonable to consider environmental legislation of a country importing products of Ukrainian enterprises. If it is more liberal, the amount of outstanding expenditures on environmental payments should be considered equal to zero. In case of infringement of environmental legislation, it is necessary to additionally consider amounts of fines and damages paid. Here, it is advisable to determine the difference between amounts of such fines and damages calculated on the basis of foreign and Ukrainian environmental laws. Analysis conducted by us demonstrate that scanty amounts paid by Ukrainian mining and concentration enterprises are due to poor methods of calculating such fines and penalties stated in national legal acts and standards (Mishchuk, 2020):

ΔF?fp = ?FPfor – ?FPukr, (3)

Where ΔF?fp is the difference between calculated amounts of fines and penalties (including payment of damage), estimated on the basis of foreign and Ukrainian legal acts and standards, c.u.;

?FPfor is the amount of fines and penalties (including payment of damage), calculated on the basis of foreign environmental legal acts and standards, c.u.;

?FPukr is the amount of fines and penalties (including payment of damage), calculated on the basis of Ukrainian environmental legal acts and standards, c.u.

Thus, the amount of outstanding environmental expenditures (ΔF?) equals the following value:

ΔF? = ΔF?pr+ΔF?t+ΔF?fp. (4)

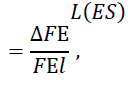

The level of security of environmentally-oriented stakeholders (L(ES)):

(5)

(5)

Where F?l is the liminal amount of environmental expenditures which is the sum of actually settled expenses and their outstanding value, c.u.

In linguistic terms, the obtained value of the security level can be described applying the scale suggested in (Mishchuk et al., 2020):

- 0 = L(ES) - zero level satisfaction of environmentally-oriented stakeholders’ eco-interests;

- 0 < L(ES) < 0.25 – minimum level of satisfaction of environmentally-oriented stakeholders’ eco-interests;

- 0.25 ≤ L(ES) < 0.5 – low level of satisfaction of environmentally-oriented stakeholders’ eco-interests;

- 0.5 ≤ L(ES) < 0.75 – mean level of satisfaction of environmentally-oriented stakeholders’ eco-interests;

- 0.75 ≤ L(ES) < 1.0 – high level of satisfaction of environmentally-oriented stakeholders’ eco-interests;

- L(ES) = 1.0 – very high level of satisfaction of environmentally-oriented stakeholders’ eco-interests.

Unlike other scientists, we believe that payment of damages resulted from environmental pollution and infringement of the environmental legislation cannot be a clear marker of the catastrophic level of environmentally-oriented stakeholders’ coherent security. It is also conditioned by the fact that amounts of such claims are so scanty and do not enable adequate determination of the damage. Penalties, fines and claims can only be used for rapid assessment of the level of enterprise activity impacts on satisfaction of environmentally-oriented stakeholders’ eco-interests.

In Ukraine, environmental control bodies are not often allowed to enterprise sites for inspections. So, fines and penalties as clear markers of security level assessment are also problematic in such cases. It should be noted that if enterprises-polluters are located in one city (e.g. as in Kryvyi Rih), the majority of environmentally-oriented stakeholders (local community) belong to all enterprises. That is why, the level of satisfying these stakeholders’ eco-interests should be determined by the worst case. This means that if at least one enterprise has the zero (or low) of satisfying eco-interests, the total level of satisfying these interests of environmentally-oriented stakeholders is considered zero (low) regardless of the levels of other enterprises. However, to determine influence of security of environmentally-oriented stakeholders on economic security and, consequently, economic development of the enterprise, it is reasonable to estimate the total amount of outstanding environmental expenditures. The higher their value is, the lower the economic security level of the enterprise is. The technique of influence of the outstanding expenditures on economic security is described in (Mishchuk et al., 2020). Unlike assessment of the level of eco-interests satisfaction, assessment of their state involves time-based measurements. Time is a summarizing indicator describing how and where the enterprise is moving and depends on the level, resources and processes available at the enterprise within a certain time period without additional interference of its management. We suggest the temporal approach providing for determination of time necessary for environmentally-oriented stakeholders’ coherent security indicators to achieve their threshold. In this case, application of value indicators used for level assessment is not reasonable due to impacts of the price factor and impossibility to determine a threshold value through environmental expenditure values. This especially pertains to volumes of financing necessary environmental programmes. That is why, to assess the security state of environmentally-oriented stakeholders, we suggest the specific pollutant emissions indicator (Ajdari & Asgharpour, 2011).

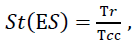

The environmentally-oriented stakeholders’ coherent security state (St(?S)) is calculated by the formula:

(6)

(6)

Where ?r is the time period during which the indicator of environmentally-oriented stakeholders’ coherent security will reach its threshold, years;

?cc is the corrected time period (cycle phases), years.

The Kitchin cycle (3 years) or one fourth of the Juglar cycle may be chosen as the corrected time period. In economics, generation of the Kitchin cycles is connected with time lags in production facilities employment, that of the Juglar cycles – with fluctuations of investments in fixed capital. Cyclic economic recessions are known to represent one of the phases of the Juglar cycle. As it consists of four phases – recovery, prosperity, recession and depression, we have chosen the length of one phase i.e. 3 years on average. When the actual time of the indicator reaching threshold (Tr) exceeds the corrected length of the cycle (cycle phase) (Tcc), the following condition is accepted for further calculations:

Tr=Tcc. (7)

To linguistically express the obtained value of the state of satisfaction of environmentally-oriented stakeholders’ eco-interests, the scale similar to the above mentioned should be used: St(ES) = 0 – zero state of satisfaction of environmentally-oriented stakeholders’ eco-interests; St(ES) = 1.0 – perfect state of satisfaction of environmentally-oriented stakeholders’ eco-interests, etc.

Results and Discussion

Let us test the suggested approach to assessment of the level of satisfaction of environmentally-oriented stakeholders’ eco-interests through the example of mining enterprises of Kryvyi Rih region and the PrJSC “ZZRK” (Zaporozhye Iron Ore Plant, Zaporizhzhia). Based on the data obtained during state environmental inspections in Dnipropetrovsk, Zaporizhzhia oblasts, we have defined that during 2018-2019 there were no damage claims at the JSC “Southern GZK” (Southern mining and processing plant, Kryvyi Rih), the PrJSC “KZRK” (Kryvyi Rih Iron Ore Plant, Kryvyi Rih) and the PrJSC “Sukha Balka” (Kryvyi Rih). The other enterprises paid the claims Table 1.

| Table 1 Amounts to Cover Losses Caused by Environmental Pollution and Infringement of Environmental Legislation, Uah / € | ||

| Enterprises | 2018 | 2019 |

| PrJSC Northern GZK (Northern mining and processing plant, Kryvyi Rih) | 6827 / 246.57 | 28997 /1001.56 |

| PrJSC Central GZK (Central mining and processing plant, Kryvyi Rih) | 0 | 1725 / 59.58 |

| PrJSC InGZK (Inguletsky mining and processing plant, Kryvyi Rih) | 0 | 254 / 8.77 |

| PrJSC ZZRK (Zaporozhye iron ore plant, Zaporizhzhia) | 52439 / 1893.90 | 0 |

Thus, the amounts of claims paid by the PrJSC Northern GZK (2018-2019), the PrJSC ZZRK (2018), the PrJSC Central GZK, the PrJSC InGZK (2019) are scanty.

It is worth noting that information on planned and actually fulfilled and financed environmental programmes should be open to public. But currently, the enterprises consider such information confidential and not for public use. That is why; it is not possible to assess the value of environmentally-oriented stakeholders’ security. One of the reasons for that is the fact that no obligatory non-financial reporting is provided for in Ukraine including GRI-based statements. Besides, even if companies disclose certain environmental issues of their activities, assurance of their statements is not obligatory either. In particular, the mining and concentration enterprises under study do not prepare separate non-financial statements. Since 2018, they have begun to publish the integrated “Management report” which is the result of harmonization of Ukrainian and European legislation in furtherance of Directive 2013/34/EU and Directive 2014/95/ EU. Along with economic issues, the enterprises reveal certain environmental aspects. Thus, in 2019, they disclosed the following: amounts of capital invested in environmental projects; volumes of gross air emissions, specific emissions of greenhouse gases (??2); discharge of pollutants into surface and underground water reservoirs; volumes of waste disposal; environmental tax amounts paid to the budget; areas for improvements in energy efficiency and energy conservation management. Yet, the listed issues are just outlined in Ukrainian legislation, detailing is left to the discretion of the enterprise preparing “Management report”. It should be noted that no financial sanctions are specified in Ukrainian legislation for non-provision of the report. We believe that it is sufficient to introduce relevant outstanding environmental expenditure items into the integrated “Management report” as the first stage of disclosing environmental issues of activities of the mining and concentration enterprises Table 2.

| Table 2 The Suggested Additional Items to be Included into the Integrated “Management Report”, Section “Environmental Issues” | |

| Items | Explanation |

| 1. Environmental tax amount paid. | Enterprises disclose amounts of the charged tax only. |

| 2. Calculated environmental tax amount to be paid in case of assessment based on stronger environmental legislation of another country. | This enables assessment of outstanding environmental expenditures coming from tolerance of Ukrainian legislation. |

| 3. Penalty (claim) amount paid for infringement of Ukrainian environmental legislation. | In some cases, amounts of charged and collected penalties differ due to appeals against environmental inspection decisions in court. |

| 4. Amounts actually spent on environmental measures and programmes. | It is reasonable to add a list of all the programmes funded. |

| 5. Amounts required for financing environmental programmes enabling real enhancement of the environmental situation at the enterprise location. | This enables assessment of outstanding environmental expenditures resulted from underspending on necessary environmental measures and programmes. |

In future, it is advisable to prepare a complete non-financial statement using GRI indicators, the following being the most significant for mining and concentration enterprises: EN3 (direct use of energy by primary sources), EN5 (energy saved due to reduced energy consumption and increased energy efficiency), EN8 (total water withdrawal by source), EN10 (water recycled and reused), EN16 (direct and indirect greenhouse gas emissions with indicated weights), EN20 (NOx, SOx and other significant air emissions by type and weight), EN21 (total water discharge by quality and destination), EN30 (total environmental protection expenditures and investments by type). Disclosure of such articles to the country is not only an important component of environmental accounting, but also a tool for managers in solving environmental problems (Van et al., 2020).

Let us test the suggested approach to assessment of the state of satisfying environmentally-oriented stakeholders’ eco-interests through the example of the above mining enterprises. The state of satisfying environmentally-oriented stakeholders’ eco-interests of was determined on the basis of the specific air pollutant emission indicator. To assess the security state, the equation of this indicator trends during 2011-2019 is determined. The threshold of specific emissions of the enterprise is determined as the actual value of specific emissions of the corresponding enterprise in 2015 decreased by the decrease standard (-6%) established in the Law of Ukraine “On the basic principles (strategy) of the state environmental policy of Ukraine for the period up to 2030”. Table 3 presents the results of calculating the state of satisfying environmentally-oriented stakeholders’ eco-interests by mining enterprises.

| Table 3 Results of Calculating the State of Satisfying Environmentally-Oriented Stakeholders’ Eco-Interests by Mining Enterprises, 2018-2019 | ||

| Indicator | 2018 | 2019 |

| PrJSC Northern GZK | ||

| Annual threshold of the specific air pollutant emission indicator, kg/t | 0.841 | 0.841 |

| Year of reaching the threshold | 2019 | 2019 |

| Period of reaching the threshold (Tr), years | 1 | 0 |

| Coherent security state indicatorSt(ES) | 0.67 | 1.00 |

| PrJSC Central GZK | ||

| Annual threshold of the specific air pollutant emission indicator, kg/t | 0.441 | 0.441 |

| Period of reaching the threshold, years | Over 3 years | Over 3 years |

| Period of reaching the threshold (Tr) considering the cycle, years | 3 | 3 |

| Coherent security state indicator St(ES) | 0 | 0 |

| PrJSC InGZK | ||

| Annual threshold of the specific air pollutant emission indicator, kg/t | 0.111 | 0.111 |

| Period of reaching the threshold, years | Over 3 years | Over 3 years |

| Period of reaching the threshold (Tr)considering the cycle, years | 3 | 3 |

| Coherent security state indicator St(ES) | 0 | 0 |

| JSC Southern GZK | ||

| Annual threshold of the specific air pollutant emission indicator, kg/t | 3.115 | 3.115 |

| Year of reaching the threshold | 2019 | 2019 |

| Period of reaching the threshold, years | 0.8 | 0 |

| Period of reaching the threshold (Tr) considering the cycle, years | 0.8 | 0 |

| Coherent security state indicatorSt(ES) | 0.75 | 1.00 |

| PrJSC Sukha Balka | ||

| Annual threshold of the specific air pollutant emission indicator, kg/t | 0.055 | 0.055 |

| Year of reaching the threshold | 2018 | 2019 |

| Period of reaching the threshold (Tr), years | 0 | 0 |

| Coherent security state indicator St(ES) | 1.00 | 1.00 |

| PrJSC ZZRK | ||

| Annual threshold of the specific air pollutant emission indicator, kg/t | 1.084 | 1.084 |

| Year of reaching the threshold | 2019 | 2019 |

| Period of reaching the threshold (Tr), years | 0.2 | 0 |

| Coherent security state indicator St(ES) | 0.94 | 1.00 |

As of 31 December, 2018 and 31 December, 2019, the security state indicator at the PJSC Northern GZK equals 0.67, thus, the coherent security state is good. As of 31 December, 2019, the indicator has grown to 1, because the enterprise reached the threshold of specific emissions (the coherent security state is perfect). At the JSC Southern GZK, the PJSC Sukha Balka and the PJSC ZZRK the state is perfect in both 2018 and 2019. At the other enterprises, the state of satisfaction of environmentally-oriented stakeholders’ eco-interests is zero. Based on the worst case methods, the state of satisfaction of environmentally-oriented stakeholders’ eco-interests at Kryvyi Rih community should be identified as zero.

In future, this situation may affect economic development of the enterprises due to possible pressure by population, community-based environmental organizations and governmental bodies. There are two types of control public and governmental. Surprisingly, public environmental control is more influential due to information disclosure in social networks and mass media. There is a fine line between legal and illegal requirements of people for clean environment. In their worst version, such requirements turn into pressure and are manifested as environmental raiding, environmental terrorism, and environmental racket. These concepts are now widely used by enterprise management and in mass media. They are implemented through public control. There are currently 5 community-based environmental organizations in Kryvyi Rih and 89 organizations of this kind in Dnipropetrovsk oblast. In case an enterprise provides grounds by infringing environmental legislation, there can be organized serious protest campaigns that can hinder economic development of the enterprise.

Conclusion

Thus, cost minimization is considered to be one of the directions of economic growth of an enterprise. However, environmental expenditures are an exception. It is substantiated that financing environmental actions is of greater interest for individual groups of stakeholders than for the enterprise as an economic entity. There are suggested methodological approaches to assessing impacts of outstanding environmental expenditures of the enterprise on coherent (dependent on its activity) security of environmentally-oriented stakeholders. These expenditures are the difference between the amount of financing required to enhance the environmental conditions at the enterprise location and the actual amount financed for environmental programmes. Ukrainian mining and concentration enterprises-polluters do not prepare non-financial statements and therefore they do not provide complete information on amounts of environmental expenditures. As a result, impacts of their activities on the environment cannot be adequately determined. It is suggested to enhance the current form of “Management report” through disclosing information on outstanding environmental expenditures and specific emissions of pollutants. Data of Ukrainian mining enterprises has enabled testing the suggested methodological approaches. Implementation of the suggested methodological approaches into practices of industrial enterprises will extend their managerial analytics with data on impacts of environmentally-oriented stakeholders’ coherent security. The above is important for understanding possible pressure from this group of stakeholders and hindrance to economic development of enterprises in the medium and long term.

Author Contributions

1. Mishchuk Ievgeniia: ideas; coherent security assessment methodology and its approbation;

2. Nusinov Volodymyr carried out the general coordination of scientific work;

3. Polischuk Serhii analysis of European environmental legislation;

4. Kutova Nataliia analysis of Ukrainian environmental legislation;

5. Stolietova Iryna conducted a literature review.

References

- Ajdari, B., & Asgharpour, S.E. (2011). Human security and development, emphasizing on sustainable development. Procedia Social and Behavioral Sciences, 19, 41-46, https://doi.org/10.1016/j. sbspro.2011.05.105

- Climate Change. (2007). The Physical Science Basis. Summary for Policymakers. (IPCC) from http://www.slvwd.com/agendas/Full/2007/06-07-07/Item%2010b.pdf

- Davidsson, P., Katz, J., & Shepherd, S. (2003). The Domain of Entrepreneurship Research: Some suggestions. Advances in Entrepreneurship, Firm Emergence and Growth, 6, 315-372 from http://doi.org/10.1016/s1074-7540(03)06010-0

- Druker, P. (2012). Menedzhment. Vyzovy XXI veka. Mann, Ivanov i Ferber from https://www.libfox.ru/405163-11-piter-druker-menedzhment-vyzovyxxi-veka.html#book

- Drlja?a, M. (2015). Restructuring of the management system and the role of top management. Quality for Future of the World, International Academy for Quality, Budapest.

- Giannopoulos, G., Filippini, R., & Schimmer, M. (2012). Risk assessment methodologies for critical infrastructure protection. Joint Research Centre of Institute for the Protection and Security of the Citizen, Part I: A state of the Art, Luxembourg, 70.

- Ianioglo, A., & Polajeva, T. (2016). Origin and definition of the category of economic security of enterprise, The 9th International Scientific Conference proceedings : Business and Management 2016, Vilnius, Lituania from http://bm.vgtu.lt/index.php/verslas/2016/paper/viewFile/47/47

- Laplume, A., & Yeganegi, S. (2009). Entrepreneurship Theories. Spring from

- https://www. entrepreneurshiptheories. com/about/

- Mcconnell, C.R., Brue, S.L., & Flynn, S.M. (2009). Economics: Principles, problems, and policies. McGraw-Hill/Irwin, Boston.

- Mishchuk, I., Zinchenko, O., & Adamenko, M. (2020). Sustainable competitive innovative development and economic security of enterprises under unstable conditions: mutual dependency and influence. E3S Web Conf., 166 from https://doi.org/10.1051/e3sconf/202016613017

- Mishchuk, I.V. (2020). Development of modern directions of estimatology in the economic security of the enterprise. Technology Audit and Production Reserves, 6(4(56), 22-28.

- Susca, P.T. (2018). Using processes to prevent and predict risk. Professional Safety, 63(8), 18-21.

- Tamoši?nien?, R., & Munteanu, C. (2015). Current research approaches to economic security. The 1 st International Conference on Business Management , Valencia, Spain from http://ocs.editorial.upv.es/index.php/ICBM/1ICBM/paper/viewFile/1537/723

- The Aspen Institute. Financial Security Program. (2019) fromhttp://www.aspeninstitute.org/programs/financial-security-program/

- Tiller, S.R. (2012). Organizational Structure and Management Systems. Leadership and Management in Engineering, 12(1), 20-23 from http://doi.org/10.1061/(asce)lm.1943-5630.0000160

- United Nations Framework Convention on Climate Change. (1992). (ratified by the Law of Ukraine of 29.10.1996 ? 435/96-VR) from https://zakon.rada.gov.ua/laws/show/995_044

- Van, H.T.T., Anh, V.T.K., Ha, D.B., Hoang T.T. (2020). Application of The Global Reporting Indicators to Build Environmental Accounting Reports of Vietnamese Enterprises in The Economic Integration Period Academy of Accounting and Financial Studies Journal, 24, 4 from https://www.abacademies.org/articles/application-of-the-global-reporting-indicators-to-build-environmental-accounting-reports-of-vietnamese-enterprises-in-the-economic-9426.html