Research Article: 2018 Vol: 22 Issue: 4

Burnout and Auditors Judgment Decision Making: an Experimental Investigation Into Control Risk Assessment

Murad Abuaddous, Al-Balqa' Applied University

Hanady Bataineh, Al-Balqa' Applied University

Enas Alabood, Al-Balqa' Applied University

Abstract

Burnout as a dysfunctional stress syndrome is expected to impact the auditors’ Judgment Decision Making (JDM). Evidence suggests that the burnout’s effect intensified during busy season but no evidence thus far investigates this effect on auditors’ JDM. Therefore, the study’s objective is to investigate whether burnout’s three interrelated factors defined in Maslach Burnout Inventory (MBI) have an effect on auditors’ JDM. Using an experimental design method tested on a multiple linear regression for 104 auditors, our results suggested that emotional exhaustion and personal accomplishment have a significant impact on auditors’ judgment over the client’s control, while no evidence was found to support that depersonalization has a significant effect on auditors’ judgment. Moreover, the study compared the reported level of burnout among auditors with other fields and found that the auditors’ burnout level was high but fell below healthcare practitioners indicating serious but not severe phenomena.

Keywords

Burnout, Maslach Burnout Inventory, Auditors, Auditor’s Burnout, JDM, Control Risk Assessment, Emotional Exhaustion, Depersonalization, Reduced Personal Accomplishment, Behavioral Auditing.

Introduction

Since the 1970s, a thrive in behavioral auditing literature has enhanced the comprehension of dysfunctional stress syndrome effect on the negative outcomes of audit practice. Many factors have been found to be responsible for the increase of such stress on auditors’ ability to generate an accurate audit judgment. In addition, evidence suggests that stress arousal factors are common in audit practice and even escalate during busy season.

During audit busy season, stress was found to amplify negative outcomes with a direct impact on audit quality. Persellin et al. (2014) found that auditors often work an extra 20 h per week during the busy season. Moreover, the busy season (usually December year-end) is the period where most of the audit practices are conducted and 70 percent of total audit practice is implemented (Francis et al., 2005; Hertz, 2006). Prior studies suggest that stress arousal factors such as job overload, conflicts, time pressure and ambiguity go up during busy season. This in turn affects the audit JDM process and in many cases leads to lower quality of audit judgment (Abuaddous et al., 2015).

Burnout as a dysfunctional stress syndrome is also intensified during busy season (Sweeney & Summer, 2002). Higher level of burnout was found to be related to negative behavior such as increasing turnover, reducing performance and job satisfactions (Fogarty et al., 2000; Smith et al., 2017). However, to our knowledge, no existing empirical research has addressed the effect of burnout on auditors’ JDM.

To fill in this gap, this study focuses on the effect of burnout on auditors’ JDM during busy season. The study adopted an experimental design method including 104 experienced auditors who were requested to assess a hypothetical audit client. To reach such assessment, the study furnished those auditors with a structural decision aid before assessing the client’s control risk in order to avoid extra burden in memory (Fredrik, 1991). Moreover, the study’s experimental material was prepared according to Libby (1995) and Libby and Luft (1993) expert paradigm, which determined the ability, knowledge and experience required for measuring performance. The results of the experiment were interpreted through a multiple linear regression on SPSS to measure the three interrelated factors of burnout namely, Emotional Exhaustion (EE), Depersonalization (DE) and Reduced Personal Accomplishment (RPA) and to find out whether each individual factor has a significant effect on auditors’ JDM.

The study hypothesizes a significant relationship between burnout's three interrelated factors, adopted from Maslach et al. (1986) and known as MBI and auditors’ judgment over the control assessment. Results detected a significant positive relation between EE and control risk assessment. In addition, the study found a significant negative relation between RPA and control risk assessment. However, no significant relation was captured at any level between DE and control risk assessment indicating that this factor does not affect auditors’ JDM. The results were positioned carefully in literature due to the rare prior researches tackling this topic. Nevertheless, some studies such as Fogarty et al. (2000) and Smith et al. (2017) found similar results when measuring the impact of these three factors on auditors’ performance.

The study also found that auditing as a profession falls above the average level of burnout jobs when compared to other demanding professions, indicating the seriousness of this syndrome in audit practice during the busy season. Prior studies were aware of such phenomena such as Buchheit et al. (2015) and Sweeney and Summer (2002) who claim that burnout levels among auditors reached levels rarely reported in audit research.

The subsequent sections proceed as follows: literature review and hypotheses development, methodology, descriptive and empirical results, discussion and conclusion, limitations and recommendations for future studies.

Literature Review and Hypotheses Development

Burnout

Job burnout is observed when employees are vulnerable to EE, DE and RPA. In psychology, two streams of literature were developed as a manifestation for the existence of the three interrelated symptoms indicating job burnout. According to Schaufeli et al. (2009) the first stream of literature focused on demand/resource imbalances which appeared in the job causing a depletion of employee’s energy. The second stream of literature considered the motives rather than the energy which appear when a misfit between the employee’s values and the environment is observed.

The main difference between these two streams is that the first stream focuses on the work environment as an expression of job burnout. In fact, this may explain the wild utilization of the three defined work role stressors (role overload, role ambiguity, role conflict) as indicators of burnout (Fogarty et al., 2000; Smith et al., 2017). The second stream focuses on the misfit between the individuals’ beliefs and the work environment to predict job burnout (Leiter and Maslach, 2003; Tong et al., 2013; Foley and Murphy, 2015; Gong et al., 2017).

Schaufeli et al. (2009) estimated 6,000 publications on burnout. Despite the plethora of studies on burnout, there is still an obvious gap in audit literature regarding auditors’ burnout indicators. Although many studies have investigated the existence or the absence of auditors’ burnout, a very few studies focused on the triggering factors for burnout. As of date, two studies adopted the role stressor factors as indicators for auditors’ burnout (Fogarty et al., 2000; Smith et al., 2017). Interestingly, the interaction between the individuals and the work environmental which was formulated in the second stream of psychology literature is still not investigated in the auditing context.

On the other hand, other fields of jobs focused on capturing the most suitable individual and environmental predictors for burnout. Leiter and Maslach (2003) conducted a comprehensive study of 11 different fields in different countries by defining 6 areas (i.e. workload, control, reward, community, fairness and values) that could generate a potential mismatch between the individual and the work environment. Their results suggest two unified predictors which are workload and fairness but different interpretations were found in the other four areas. Foley and Murphy (2015) argued that teachers’ burnout can be predicted by a combination of individual, environmental and coping factors. Gong et al. (2017) argued that Chinese police officers’ burnout can be predicted when environmental indicators are mediated by individual factors.

In essence, job burnout is subjected to the unique setting of the job itself and impacted by the cultural context. To inform this debate, the unique setting for individual and environmental predictors that were found in the real world auditing can be coveted and further broken down in order to determine the best predictors for auditors’ burnout. This can be achieved through an extensive scrutiny of the individual and environmental various aspects of auditors’ behavioral, psychological, sociological and governmental/ political aspects found in their practice. These aspects should in turn influence the three burnout factors EE, DE and RPA to indicate the most suited auditors’ burnout predictors.

Auditors are routinely occupied with various audit clients, following restricted schedules, mentoring, and goals achievement, and conducting many training sessions during the year. Therefore, it is not surprising that some auditors work extra 5 hours per week before the busy season (Persellin et al., 2014). The demanding nature of audit practice becomes more challenging and time consuming during the busy season as auditors are subjected to more time pressure and late working hours, and encounter more risky decisions (Lopez and Peters, 2012). Buchheit et al. (2015) find that burnout is in fact a present phenomenon in audit bureau, especially in large audit firms. They conducted a survey including 1063 accounting professionals to investigate the effect of family-working conflict on the level of auditors' burnout. Their results suggest that auditors at the Big 4 reported higher levels of employees’ burnout than those in smaller offices. They also find that public accounting professionals reported higher levels of employee burnout than CPAs in industry.

Regrettably, there are few studies in audit literature which tackled the effect of burnout on auditors. Fogarty et al. (2000) were among the first to raise the attention for the impact of burnout on auditors’ outcomes. They constructed a model to enable separating the functional and dysfunctional role of stressor on job outcomes through understanding burnout effect. The model describes the three role stressors moderated by burnout and resulting in three job outcomes (satisfaction, performance, and turnover intentions). A replica of their study was conducted by Smith et al. (2017) and enhanced by studying the interaction between the three interrelated symptoms of burnout as moderator for the same role stressors and job outcomes.

The factors determined by Fogarty et al. (2000) were briefly studied in audit literature. A survey conducted by Herda and James (2012) found that auditors under job burnout yielded greater turnover intentions. Their results were consistent with Pradana and Salehudin (2015) findings that work overload had a significant effect on increasing turnover intention through both job satisfaction and work related stress. Sweeney and Summer (2002) investigated the effect of increasing working load during the busy season on auditors' level of burnout. Their results matched those of Persellin et al. (2014) that working load significantly increased during auditors' busy season. In addition, they reported that this increase in work-load resulted in a significant increase in the level of burnout among auditors. In fact, they argued that auditors' burnout reached levels rarely reported in audit research.

Burnout and audit performance were another but rare trend in audit literature. Two notable attempts by Forgaty et al. (2000) and Smith et al. (2017) found a significant association between burnout and performance. Forgaty et al. (2000) concluded that burnout symptoms negatively impacted auditors’ performance while Smith et al. (2017) found that RPA was the only factor of burnout to negatively associate with auditors’ performance. Both studies captured this relation through self-reporting auditors who were asked to evaluate their performance relative to other colleagues'.

All in all, prior audit research reported the existence of burnout as a factor of stress during auditors' busy season. These studies found that working load, conflicts and ambiguity triggered factors for burnout which in turn impacted job satisfaction, performance, and turnover intentions. We must stress again that, to our knowledge, no existing empirical research has addressed the question of the effect of burnout on auditors’ JDM.

Burnout and JDM

In Psychology researches, well established systematic empirical studies on burnout were presented in the late 1970s and early 1980s (Iwanicki & Schwab, 1981; Maslach & Jackson, 1981). Maslach et al. (1986) provided the most utilized and well defined method for burnout measurement, also known as MBI. The conventions of the MBI allowed more researchers to explore the level of burnout among various professions. Signs of burnout were found in social worker (Abdallah, 2009), firefighters (Katsavouni and Benek, 2015), medical Students (Dos Santos Boni et al., 2018), pharmacy practice (El-Ibiary and Lee, 2017), accounting and finance academics (Byrne et al., 2011) and auditors (Sweeney and Summer, 2002; Herda and James, 2012; Buchheit et al., 2015).

Another line of Psychology research focused on the effect of burnout on performance and factors that could moderate the effect of burnout. Maslach et al. (1985) found that burnout is responsible for decreasing the quality and quantity of job performance. Van Dam et al. (2011) concluded that burnout patients perform poorer than healthy controls on attention and memory tasks. Moreover, the motivation to spend effort is relatively permanently decreased in burnout which may lead to reduced cognitive performance. They constructed an experiment to explore whether burnout patients would respond better if their motivation was boosted in the experiment. Instead, results showed that burnout patients did not improve their performance and experienced more aversion to spending effort. Diestel et al. (2013) found that the error rate and reaction times increased for emotionally exhausted nurses when they were subjected to demanding tasks.

Other psychology studies suggest that burnout is responsible for altering the cognitive ability for the decision maker in terms of memory tasks, performance, judgment style and ethical decisions. This alteration of judgment process is expected to impact auditors who are fitted in the demanding job genre. McGee (1989) argued that burned-out personnel are coping with their status by avoiding the involvement in sensitive decisions. The potential explanation for this reaction could refer to the anxiety which appeared in tandem with burnout (Moreno-Jiménez et al. 2008). In addition, management practice (democratic or autocratic) has proven to impact the level of burnout and thus JDM (Sunar et al., 2009). Ethical JDM and burnout were yet another important area which has been investigated in prior studies. Teixeira et al. (2013) found a positive relation between ethical JDM and burnout in the nursing field. Their results show that burnout could alter JDM when an ethical manner presents itself.

A more recent study conducted by Michailidis and Banks (2016) argued that when the job required an important decision to be made, employees under burnout were found to be prone to risky decision making. They also found that when those employees were aware of the serious consequences of their decision, burnout effect could fade away in order to prevent additional feelings of burnout rising, leading burnout employees to choose less risky option. The results of Michailidis and Banks (2016) indicate that burnout and JDM have an interactive relationship where the mindset of the decision maker at the moment of the decision is an essential factor to determine the value of the decision. A main point of contrast here is that even in the psychological context, the evidence for such interaction is still at its early stages.

Since the main objective of the current study is to examine the effect of burnout on auditors’ JDM over the control risk, the next section discusses the main prior contributions regarding the topic.

Control Risk Assessment and JDM

Auditor judgment over control risk assessment requires specific knowledge, skills and ability. Other involved environmental factors have also been considered in order to achieve the best means of control risk assessment. Luckily, behavioral audit studies related to audit judgment were extensively carried out during the 1980s and 1990s. The notable work of Libby (1985) and Libby and Luft (1993) resulted in establishing a model that became the foundation for predicting the role of audit expertise in judgment; later on, this model was called “the expertise paradigm”. Libby (1995) focused on the relationship between auditors’ ability, knowledge, and experience in performance by constructing a model that contained two inputs (ability and experience), one moderator (knowledge), and performance as an output. Libby (1995) further explained that most studies which covered auditors’ JDM tended to make two assumptions. First, stimulation and the resulting mental effort are not different among individuals and exceed the least requirements of learning and task performances. Second, environmental factors such as stress factors are taken into consideration only when they affect the correlation between knowledge and ability. Therefore, a key to successful experimental study that deals with knowledge-related determinations of performance should specify the knowledge requirements for the task on the one hand, and specify the cognitive processes involved in performing a specific task, on the other.

Following this logic, the knowledge requirement for assessing the internal control was described by Abdolmohammadi and Wright (1987) who argued that internal control’s evaluation over a payroll system was found to be semi-complex for beginner auditors. Moreover, Plumlee (1985) found that internal auditors with specific prior experience appeared to rely on memory when reviewing an internal control system, while internal auditors who lacked specific prior experience were less able to organize their general knowledge to critically review an internal control system. Therefore, internal control evaluation can be described as a semi-complex task that required a moderate level of experience to be accomplished. Although there are only few studies to enhance this argument, Abuaddous et al. (2015) supported this view as they found that surrogates failed to achieve an acceptable consensus with experts when assessing the client’s control risk.

Another aspect of Libby’s (1995) model is the cognitive processes involved in internal control evaluation. Tortman and Wood (1991) found that the difference in the level of consensus in the internal control judgment examined, could be accounted for by sampling error alone, and that none of the moderator variables, such as number of cases, number of cues presented, and type of internal control system, had a significant effect on the level of consensus. Therefore, the memory retrieval for cues and information is the main challenge for subjects evaluating the client’s internal control. Frederick (1991) found that auditor's retrieval of internal controls from memory not only depends on the auditor's level of experience, but also on the way in which the auditor's knowledge of controls is organized through structure. In fact, many studies found that the existence of audit structure when dealing with complex tasks improves auditors’ performance and the effectiveness of their judgment when compared to the absence of such structure (Butler, 1985; Kachelmeier and Messier, 1990; McDaniel, 1990; Messier et al., 2001; Zimbleman, 1997). Thus, a structural presentation was found to overcome the issue of information overload and other factors that cause a burden on the memory.

So far, evidence suggests that burnout is a real phenomenon in audit practice especially during busy season. Determining the effect of burnout on audit JDM is still missing in audit literature. Few studies in psychology literature have indicated that burnout tends to affect JDM, but there is no consensus regarding the nature of this effect. As mentioned before, burnout is measured by the MBI which tests the level of burnout characterized by three interrelated symptoms of EE, RPA and DE. Control risk assessment requires a reasonable level of audit experience and a structural decision form to overcome memory burden.

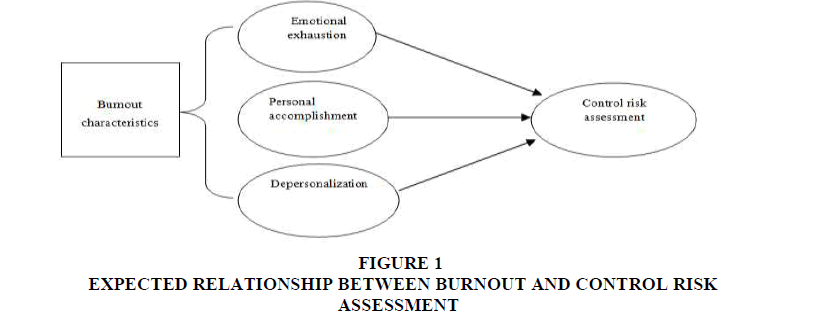

Considering the aforementioned summary, this study speculates that burnout can impact auditors’ JDM when assessing the control risk. The suggested form of relation is expressed through Figure 1.

Figure 1: Expected Relationship Between Burnout and Control Risk Assessment

Therefore, this study hypothesizes the following relations:

H1: There is a significant relation between emotional exhaustion and control risk assessment.

H2: There is a significant relation between depersonalization and control risk assessment.

H3: There is a significant relation between reduced personal accomplishment and control risk assessment.

The sections below furnish the study methodology, results, discussion and conclusion, limitations and recommendations for future studies.

Methodology

Sample and Procedures

Participants are auditors from two Jordanian public accounting firms. Both firms are among the big 4 audit firms in the country. The case material was furnished by two audit partners who volunteered to assess the research questions and accomplish the experiment. The case material stated that the study was solely for research purposes and subjects would keep anonymous. Responses were collected in two sessions for each firm, both of which were held in mid-December 2017. A total of 110 auditors submitted the case material and a total of 104 fully completed the experiment with useful information. This study relied on self-reporting measures by the auditors to test the study variable. Thus, we adopted the following steps to avoid common method variance. First, the case material was designed in a simple language and with a measuring scale that auditors were familiar with. This treatment was achieved by reviewing the case by auditors’ partners before conducting the experiment. Second, the case material included some reverse-coded questions in The Committee of Sponsoring Organizations’ (COSO) framework assessment in order to reduce contamination by the consistency motif (Podsakoff et al., 2003).

This study adopted an experimental designed setting to answer the study hypotheses. The experiment included four parts. First, subjects were requested to furnish some personal information related to gender, marital status, years of experience and number of dependents. This information was requested based on Cordes & Dougherty (1993), who summarized the relationship between demographic variables and the burnout components from prior literature. Second, we prepared a hypothetical case material about a company specialized in pharmaceutical industry. The case material was based on academic research literature (Abdolmohammadi & Wright, 1987; Abdolmohammadi, 1999; Ketchkova et al., 2013; Abuaddous et al., 2015), professional auditing standards, and textbooks (Lemon et al., 2000). Third, subjects were requested to assess 27 factors covering the main points in COSO’s framework. The factors in COSO’s framework were assessed by an internal audit partner who adjusted some of the terms to imitate those in practice. Subjects were asked to assess these factors in a Lickert-scale of 1-7 in order to reach a conclusion about the client’s control risk assessment which was measured on a scale of 1-9. The reason for including the framework was to adopt a structural decision framework mimicking the one found in practice. In addition, the framework was expected to maintain a professional judgment by avoiding arbiter decisions and avoiding decisions conducted out of a structural form (Frederick, 1991). Fourth, the final part of the experiment presented the three parts of the MBI which intended to test the level of burnout characterized by three interrelated symptoms of EE, RPA and DE on a scale of 0-6. The level of EE was measured with seven items (“I feel like my work is breaking me down”). Included in the DE subscale were seven items, such as “I feel tired when I get up in the morning and have to face another day at work”. Finally, RPA was measured in eight items (“I feel full of energy”). A high degree of burnout is reflected in high scores on exhaustion and DE and low scores on RPA.

Descriptive Results

Demographic information about the sample is shown in Table 1. Around two thirds of the sample were males (69%) compared to only (31 %) females; (44.2 %( were single while (55.8%) were married. The sample consisted of (27%) of auditors with an average of 3 years’ experience, (54%) with 6 years of experience and about (19%) of the sample with more than 10 years’ experience in practice. Number of auditor's dependents was also requested: (39.4%) were found to only support themselves, (45.2%) supported between 1-3 members, (13.5%) 3-5, and only (1.9%) supported more than 5 persons.

| Table 1 RESPONDENTS' DEMOGRAPHIC PROFILE |

|||

| Percent | Percent | ||

| Gender | Marital Status | ||

| Male | 69% | Single | 44% |

| Female | 31% | Married | 56% |

| Number of dependents | Responsibility level | ||

| Yourself | 39% | Entry level/staff | 27% |

| 1-3 | 45% | Experienced/senior | 54% |

| 3-5 | 14% | Supervisor/manager | 19% |

| More than 5 | 2% | ||

Table 2 presents the descriptive statistics for the independent and dependent variables as speculated. A multiple regression analysis was conducted in SPSS to test the study's three hypotheses. Table 2 summarizes the key descriptive statistics for the constructs under study. Nunnaly (1978) indicated that a (0.7) is an acceptable level of reliability coefficient in Cronbach's Alpha test. Thus, our results indicate an acceptable level of internal consistency among the three burnout symptoms; (0.739) for EE items, (0.775) for DE items and (0.866) for RPA items.

| Table 2 DESCRIPTIVE STATISTICS |

||||||

| N | Minimum | Maximum | Mean | Std. Deviation | Cronbach's Alpha | |

| CRA | 104 | 2.00 | 8.00 | 5.5577 | 1.47357 | |

| DP | 104 | 3.00 | 26.00 | 12.0481 | 5.42626 | 0.775 |

| EE | 104 | 10.00 | 42.00 | 24.0192 | 6.74642 | 0.739 |

| PA | 104 | 5.00 | 47.00 | 33.8269 | 7.50203 | 0.866 |

| Valid N (listwise) | 104 | - | - | - | - | - |

CRA: Control risk assessment, DP: depersonalization, EE: emotional exhaustion, PA: reduced personal achievement

The Mean score for control risk assessment is (5.56 out of 9). In addition, the three interrelated symptoms of burnout scored (24) for EE, (12) for DE and (34) for RPA. These results differ from those by Sweeney & Summer (2002) who find a score of (31) for EE, (13) for DE and (24) for RPA. This variation in results may be due to several reasons. First, enhancement of the audit profession over the last 15 years may have generated different challenges and stress types for auditors. Second, the cultural and economic differences between the two samples may be also responsible for this variation.

Table 3 provides the frequency analysis of the interrelated burnout symptoms. Only 16% of the auditors reported low level of EE, 58% and 26% of the auditors reported moderate and high level of EE respectively. DE was high among auditors; only 11% reported a low burnout level on the scale while 43% and 46% of the auditors reported a moderate and high level of DE, which concludes that auditors’ response to the audit clients tends to be impersonal. Finally, RPA level was also found to be high as reported by 38% of the auditors and only 25% showed a sense of achievement.

| Table 3 ANALYSIS OF BURNOUT SYMPTOMS FOUND IN AUDITORS’ BUSY SEASON |

|||

| Burnout symptom | Ranges | Frequency | Percentage |

| Emotional Exhaustions | Low | 17 | 16% |

| Moderate | 60 | 58% | |

| High | 27 | 26% | |

| Depersonalization | Low | 11 | 11% |

| Moderate | 45 | 43% | |

| High | 48 | 46% | |

| Reduced Personal Accomplishment | Low | 26 | 25% |

| Moderate | 38 | 37% | |

| High | 40 | 38% | |

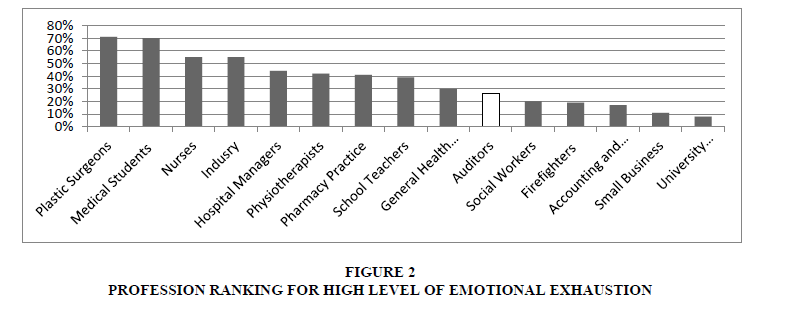

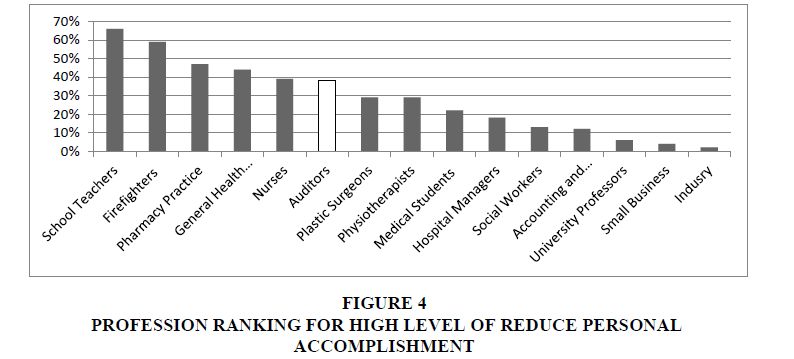

To reach a meaningful interpretation of these results, Table 4 provides a summary for burnout results in 14 other demanding jobs. In addition, it also shows the percentage of the high level of burnout reported in previous studies regarding other professions. Thus, Figures 2-4 shows the auditors’ level of burnout compared to other demanding jobs in order to understand the severity of auditors’ burnout.

Figure 2: Profession Ranking for High Level of Emotional Exhaustion

Figure 3: Profession Ranking for High Level of Depersonalization

Figure 4: Profession Ranking for High Level of Reduce Personal Accomplishment

| Table 4 SUMMARY OF PAPERS’ FINDINGS FOR BURNOUT LEVELS |

|||||||

| Authors, Year of Publication | Country | Sample Size | Gender | Profession | Prevalence High EE (%) | Prevalence High DP (%) | Prevalence Low PA (%) |

| Abdallah (2009) | Palestine | 180 | Males (33%) and females (67%) | Social worker | 20% | 47% | 13% |

| Al-Imam and Al-Sobayel (2014) | Saudi Arabia | 119 | Males (37%) and females (63%) | Physiotherapists | 42% | 34% | 29% |

| Byrne et al. (2011) | Ireland | 243 | Males (52%) and females (48%) | Accounting and Finance Academics | 17% | 15% | 12% |

| Aldrees et al. (2017) | Saudi Arabia | 38 | Males (74%) and females (26%) | Plastic Surgeons | 71% | 50% | 29% |

| Dos Santos Boni et al. (2018) | Brazil | 330 | Males (66%) and females (34%) | Medical Students | 70% | 52% | 22% |

| El-Ibiary and Lee (2017) | USA | 758 | Males (32%) and females (68%) | Pharmacy Practice | 41% | 10% | 47% |

| Hamaideh (2011) | Jordan | 181 | Males (56%) and females (44%) | Nurses | 55% | 34% | 39% |

| Katsavouni and Benek (2015) | Greece | 3289 | Males (84%) and females (12%) | Firefighters | 19% | 23% | 59% |

| Oakes and Booker (2013) | USA | 86 | Males (20%) and females (80%) | School Teachers | 39% | 9% | 66% |

| Padilla and Suarez (2017) | Colombia | 37 | Males (42%) and females (58%) | University Professor | 8% | 0 | 6% |

| Popescu et al. (2018) | Romania | 82 | N/A | Industry | 55% | 48% | 2% |

| Popescu et al. (2018) | Romania | 47 | N/A | Small Business | 11% | 11% | 4% |

| Yuguero et al. (2017) | Spain | 50 | Males (18%) and females (82%) | General Health Practitioners | 30% | 11% | 44% |

| Zopiatis and Constanti (2010) | Cyprus | 13 | Males (71%) and females (29%) | Hospital Managers | 44% | 46% | 18% |

Figure 2 indicates that auditors are below the average in terms of EE. This does not by any means indicate that auditors are not emotionally exhausted during busy season but rather that auditing is not among the highly emotional exhausting jobs. In addition, Figure 3 categorized the prior findings according to those who reported a high level of DE. Auditors were found to be above the average; exceeding other well-known sensitive jobs that usually report high level of DE, such as nurses and firefighters. Finally, Figure 4 shows that the sense of achievement among auditors is below the average indicating a high level of RPA.

It is important to note that auditors’ scores in MBI were close to medical field professions and other jobs with serious physical efforts. In contrast, auditors’ scores in MBI were far higher than accountant academics, social workers, small business owners and university professors. This indicates that auditors’ burnout is at a high level but does not match jobs that are very demanding in nature. Another potential explanation for auditors’ lower burnout level when compared to these demanding professions is that the peak of audit stress is a seasonal event compared to other high burnout fields that face stress on daily basis, which in return could be the reason for the reduction of the overall burnout level for auditors as they expect stress to be shortlived. Therefore, the study concludes that burnout in auditing is a serious phenomenon rather than a severe one.

Empirical Results

The results of the multiple linear regression analysis are presented in Table 5. The results indicate a significant positive relationship at p<0.01 between EE and auditor risk assessment. In other words, the more auditors feel emotionally exhausted the more tendency to increase the assessment of control risk for the audit clients. This result confirms the first hypothesis in this study; moreover, it captures a positive impact which indicates that the first MBI symptoms can cause a change in auditors’ perception of risk. The second hypothesis predicts a significant association between DE and auditor risk assessment. The study failed to capture such relation at any significant level. However, a significant negative relation was captured at p<0.01 between RPA and auditor control risk assessment. In other words, the lower auditors appreciate their accomplishment in work the more their assessment of control risk tends to increase.

| Table 5 MULTIPLE LINEAR REGRESSION ANALYSIS |

||||||

| Model | Unstandardized Coefficients | Standardized Coefficients | t | Sig. | ||

| B | Std. Error | Beta | ||||

| 1 | (Constant)a | 6.687 | 0.928 | - | 7.208 | 0.000 |

| EE | 0.066 | 0.022 | 0.3000 | 2.970 | 0.004 | |

| PA | -0.065- | 0.019 | -0.329 | -3.448 | 0.001 | |

| DP | -0.043- | 0.0280 | -0.158 | -1.532 | 0.129 | |

a. Dependent Variable: CRA

Discussion

Positioning these findings in the audit literature may be challenged by the scarcity of available sources. Despite the fact that some prior audit studies (Smith et al., 2017; Fogarty et al., 2000) measured the effect of the three interrelated symptoms of burnout on auditor performance, measurement of performance was captured through self-assessment by the auditors about how they perceived their performance relative to their colleagues'. Moreover, performance evaluation in these studies was not collected during the busy season period which has been proven to increase auditors’ burnout to a remarkable level (Sweeney & Summer, 2002). In addition to this, Fogarty et al. (2000) findings showed a significant negative relationship between EE and auditors' assessment of their performance. This result is related to our findings as we found a reverse impact with auditors’ assessment of control risk. To put it in other words, the more the auditors feel emotionally exhausted the more likely to report a lower performance compared to their colleagues', and this lead to an over-assessment of audit control risk when compared to that by those who did not show signs of EE. DE as a second individual symptom of burnout was found in prior studies to have an insignificant relation with performance (Smith et al., 2017) or a significantly negative relation with performance (Fogarty et al., 2000). We captured similar results as we found an insignificant but negative relation between DE and auditors' JDM for control risk assessment. Finally, Smith et al. (2017) and Fogarty et al. (2000) found a significant negative relationship between RPA and auditors' perception of their performance. This study captured a similar trend for auditors’ judgment regarding control risk. That is, when auditor’s personal accomplishment reduced, their assessment of control risk increased.

Regrettably, audit literature does not provide findings regarding the effect of burnout on auditor’s JDM. However, our study results concur with Buchheit et al. (2015) and Sweeney and Summer (2002) who showed that burnout is a serious issue in audit practice and is rarely reported and captured in previous studies. Moreover, both studies showed that this phenomenon goes up significantly during the audit busy season through comparing the MBI results before and during the busy season.

Our results revealed that auditors’ scores in MBI were less severe than those of medical field professions and other jobs with serious physical efforts but far higher than other less demanding jobs. The fact that audit stress is a seasonal event may explain the reduced level of auditors’ burnout compared to other demanding fields as auditors expect stress to be short-lived. Therefore, the study concludes that burnout in auditing is a serious phenomenon rather than a severe one.

In contrast, our results found that the burnout level among auditors falls below the medical fields which deviate from Sweeney and Summer (2002) as they found that the level of burnout among auditors exceeds the one found among teachers, post-secondary educators, social services, physicians and nurses in mental health centers even before the busy season.

Given the fact that most sensitive audit judgments are practiced during the busy season (Lopez and Peters, 2012), a serious question about the accuracy of burned and engaged auditors’ judgment should be raised during the audit process. As this has a direct impact on audit judgment quality and raises questions about whether the effect of burnout can alter or enhance an audit judgment that may be generated without burnout effect.

It is also worth mentioning that prior psychology studies are still debating how burnout may affect JDM. Some studies argue that the decision maker who is subject to burnout tends to increase attention to details, before executing the judgment, as a defense mechanism to avoid more problems that may worsen his/her life situation (Michailidis and Banks, 2016). Others relate job burnout to increasing error rates and reaction time (Diestel et al., 2013). Therefore, audit studies are still in their early stages and more need to be carried out to fill this gap in research about burnout impact on audit judgment.

Conclusion, Limitations and Recommendations for Future Studies

Burned out auditors are susceptible to various types of negative outcome, the current study has speculated a significant relationship between burnout's three interrelated factors and auditors’ JDM for control assessment. Our results confirmed that auditors who reported a high level of EE showed an increase in their risk assessment in comparison to engaged auditors. Consistent with EE results, auditors who reported low level of RPA were found to report a higher level of risk assessment. Finally, DE’s impact on auditors’ assessment of control risk was found to be inconclusive. These results indicate that auditors who show signs of burnout tend to cope differently than engaged auditors in terms of JDM. Several explanations can be drawn from psychology about burnout’s coping strategies which varies from a positive to a negative impact on the decision making quality. To this end, this study provides statistical evidence that burned out auditors are generating different audit judgment than engaged auditors which opens the door for further investigation regarding the quality of burned out auditors’ decision.

We acknowledge several limitations of this study. The current study relied on self –report survey of auditors. Therefore, our results should be interpreted carefully when drawing the causal relationships among the variables. The study adopted some recommended procedures to mitigate consistency motif. However, self-reported data may have been influenced by common methods variance. In addition, the quality of the auditors’ decision making process can be better assessed in a simplified representation of auditing contexts than in the real world of auditing. Controlled experiment settings can never capture all the complexity of actual audit practice where the amount of the information and options available to the auditor during an experiment are more restricted.

Despite these limitations, this study provides some evidence on how burnout affects auditors JDM. It also acknowledges two important gaps in audit literature regarding burnout. The first is the absence of proper indicators to explain burnout within the audit practice. The second is the lack of prior studies that consider the accuracy of burned-out auditors’ decisions in comparison to engaged ones which has a direct effect on the audit quality.

The results can provide several implications for audit firms. Jordanian audit firms should realize that auditors are subjected to a serious level of burnout during busy seasons. Therefore, audit firms are advised to consider the mental health status of their staff who is subjected to work stress especially during busy seasons. This can be achieved by having more involvement of the human resource department in regards to their staff that shows signs of burnout. This can lead to a mitigation of the impact of burnout on auditors JDM quality and other detected negative outcome.

Future studies can focus on the indicators which are responsible for burnout in auditors. The misfit between the individual and the environmental indictors as a sign for burnout is still missing in audit literature. In addition, the accuracy of burned out auditors’ JDM compared to engaged auditors is another gap that is found in audit studies. Other studies can extend this subject by measuring other related factors required for audit judgment such as audit risk and business risk decisions using the well-established audit literature covering this topic.

References

- Abdallah, T. (2009). Prevalence and predictors of burnout among Palestinian social workers. International Social Work, 52(2), 223-33.

- Abdolmohammadi, M.J. (1999). A comprehensive taxonomy of audit task structure, professional rank and decision aids for behavioral research. Behavioral Research in Accounting, 11, 51.

- Abdolmohammadi, M., & Wright, A. (1987). An examination of the effects of experience and task complexity on audit judgments. Accounting Review, 62(1)1-13.

- Abuaddous, M., Hanefah, M., & Laili, N.H. (2015). Audit structure, time pressure and judgment accuracy: A comparison between strategic system audit and traditional audit. International Journal of Economics and Finance, 7(8), 53.

- Aldrees, T., Hassouneh, B., Alabdulkarim, A., Asad, L., Alqaryan, S., Aljohani, E., & Alqahtani, K., (2017). Burnout among plastic surgery residents: National survey in Saudi Arabia. Saudi medical journal, 38(8), 832-836.

- Al-Imam, D.M., & Al-Sobayel, H.I. (2014). The prevalence and severity of burnout among physiotherapists in an Arabian setting and the influence of organizational factors: An observational study. Journal of physical therapy science, 26(8), 1193-1198.

- Buchheit, S., Dalton, D.W., Harp, N.L., & Hollingsworth, C.W. (2015). A contemporary analysis of accounting professionals' work-life balance. Accounting Horizons, 30(1), 41-62.

- Butler, S.A. (1985). Application of a decision aid in the judgmental evaluation of substantive test of details samples. Journal of Accounting Research, 23(2), 513-526.

- Gong, Z., Zhang, J., Zhao, Y., & Yin, L. (2017). The relationship between feedback environment, feedback orientation, psychological empowerment and burnout among police in China. Policing: An International Journal of Police Strategies & Management, 40(2), 336-350.

- Cordes, C.L., & Dougherty, T.W. (1993). A review and an integration of research on job burnout. Academy of management review, 18(4), 621-656.

- Diestel, S., Cosmar, M., & Schmidt, K.H. (2013). Burnout and impaired cognitive functioning: The role of executive control in the performance of cognitive tasks. Work & Stress, 27(2), 164-180.

- Dos Santos Boni, RA., Paiva, C.E., de Oliveira, M.A., Lucchetti, G., Fregnani, J.H.T.G., & Paiva, B.S.R. (2018). Burnout among medical students during the first years of undergraduate school: Prevalence and associated factors. PloS one, 13(3).

- El-Ibiary, S.Y., Yam, L., & Lee, K.C. (2017). Assessment of burnout and associated risk factors among pharmacy practice faculty in the United States. American Journal of Pharmaceutical Education, 81(4), 1-9.

- Fogarty, T.J., Singh, J., Rhoads, G.K., & Moore, R.K. (2000). Antecedents and consequences of burnout in accounting: Beyond the role stress model. Behavioral Research in Accounting, 12(1), 32-67.

- Foley, C., & Murphy, M. (2015). Burnout in Irish teachers: Investigating the role of individual differences, work environment and coping factors. Teaching and Teacher Education, 50, 46-55.

- Frederick, D.M. (1991). Auditors' representation and retrieval of internal control knowledge. Accounting Review, 66(2), 240-258.

- Hamaideh, S.H. (2011). Burnout, social support, and job satisfaction among Jordanian mental health nurses. Issues in Mental Health Nursing, 32(4), 234-242.

- Herda, D.N., & Lavelle, J.J. (2012). The auditor-audit firm relationship and its effect on burnout and turnover intention. Accounting Horizons, 26(4), 707-723.

- Iwanicki, E.F., & Schwab, R.L. (1981). A cross validation study of the Maslach Burnout Inventory. Educational and psychological measurement, 41(4), 1167-1174.

- Kachelmeier, S.J., & Messier Jr, W.F. (1990). An investigation of the influence of a nonstatistical decision aid on auditor sample size decisions. Accounting review, 65(1), 209-226.

- Katsavouni, F., Bebetsos, E., Malliou, P., & Beneka, A. (2015). The relationship between burnout, PTSD symptoms and injuries in firefighters. Occupational medicine, 66(1), 32-37.

- Kochetova-Kozloski, N., Kozloski, T.M., & Messier Jr, W.F. (2013). Auditor business process analysis and linkages among auditor risk judgments. Auditing: A Journal of Practice & Theory, 32(3), 123-139.

- Leiter, M.P., & Maslach, C. (2003). Areas of worklife: A structured approach to organizational predictors of job burnout. Emotional and physiological processes and positive intervention strategies, 3, 91-134.

- Libby, R. (1985). Availability and the generation of hypotheses in analytical review. Journal of Accounting Research, 23(2), 648-667.

- Libby, R. (1995). The Role of Knowledge and Memory in Audit Judgment and Decision Making. Judgment and decision-making research in accounting and auditing, 176-206.

- Libby, R., & Luft, J. (1993). Determinants of judgment performance in accounting settings: Ability, knowledge, motivation, and environment. Accounting, organizations and society, 18(5), 425-450.

- López, D.M., & Peters, G.F. (2012). The effect of workload compression on audit quality. Auditing: A Journal of Practice & Theory, 31(4), 139-165.

- McGee, R.A. (1989). Burnout and professional decision making: An analogue study. Journal of Counseling Psychology, 36(3), 345-351.

- Maslach, C., & Jackson, S.E. (1981). The measurement of burnout. Journal of Occupational Behavior, 2(2), 99-113.

- Maslach, C., Jackson, S.E., Leiter, M.P., Schaufeli, W.B., & Schwab, R.L. (1986). Maslach burnout inventory. Palo Alto, CA: Consulting Psychologists Press.

- McDaniel, L.S. (1990). The effects of time pressure and audit program structure on audit performance. Journal of Accounting Research, 28(2), 267-285.

- Messier Jr, W.F., Kachelmeier, S.J., & Jensen, K.L. (2001). An experimental assessment of recent professional developments in nonstatistical audit sampling guidance. Auditing: A Journal of Practice & Theory, 20(1), 81-96.

- Michailidis, E., & Banks, A.P. (2016). The relationship between burnout and risk-taking in workplace decision-making and decision-making style. Work & Stress, 30(3), 278-292.

- Moreno-Jiménez, B., Rodríguez-Carvajal, R., Garrosa Hernández, E., & Morante Benadero, M.A. (2008). Terminal versus non-terminal care in physician burnout: the role of decision-making processes and attitudes to death. Salud mental, 31(2), 93-101.

- Nunnaly, J. (1978). Psychometric theory. New York: McGraw-Hill.

- Oakes, W.P., Lane, K.L., Jenkins, A., & Booker, B.B., (2013). Three-tiered models of prevention: Teacher efficacy and burnout. Education and Treatment of Children, 36(4), 95-126.

- Padilla, A.A.G., Bonivento, C.V.E., & Suarez, B.S.P. (2017). Burnout syndrome and self-efficacy beliefs in professors. Propósitos y representaciones, 5(2), 65-126.

- Persellin, J., Schmidt, J., & Wilkins, M.S. (2014). Auditor perceptions of audit workloads, audit quality, and the auditing profession. School of BusinessFaculty Research.

- Plumlee, R.D. (1985). The standard of objectivity for internal auditors: Memory and bias effects. Journal of Accounting Research, 23(2), 683-699.

- Podsakoff, P.M., MacKenzie, S.B., Lee, J.Y., & Podsakoff, N.P. (2003). Common method biases in behavioral research: A critical review of the literature and recommended remedies. Journal of applied psychology, 88(5), 879-903.

- Popescu, L., Iancu, A., Vasile, T., & Popescu, V., (2018). Stress and burnout of human resources at the level of Mehedinti County–Romania organisations. Economic Research-Ekonomska Istra?ivanja, 31(1), 498-509.

- Schaufeli, W.B., Leiter, M.P., & Maslach, C. (2009). Burnout: 35 years of research and practice. Career development international, 14(3), 204-220.

- Smith, K.J., Emerson, D.J., & Everly Jr, G.S. (2017). Stress Arousal and Burnout as Mediators of Role Stress in Public Accounting. Advances in Accounting Behavioral Research, 20, 79-116.

- Sunar, I.G., Omar-Fauzee, M.S., & Yusof, A. (2009). The effect of school coaches decision-making style and burnout on school male soccer players. European Journal of Social Sciences, 8(4), 672-682.

- Sweeney, J.T., & Summers, S.L. (2002). The effect of the busy season workload on public accountants' job burnout. Behavioral Research in Accounting, 14(1), 223-245.

- Teixeira, C., Ribeiro, O., Fonseca, A.M., & Carvalho, A.S. (2013). Ethical decision making in intensive care units: a burnout risk factor? Results from a multicentre study conducted with physicians and nurses. Journal of medical ethics, 40(2), 97-103.

- Tong, J., Wang, L., & Peng, K. (2015). From person-environment misfit to job burnout: Theoretical extensions. Journal of Managerial Psychology, 30(2), 169-182.

- Trotman, K.T., & Wood, R. (1991). A meta-analysis of studies on internal control judgments. Journal of accounting research, 29(1), 180-192.

- Tucker, R.R. (2000). Auditing: An Integrated Approach. Issues in Accounting Education, 15(4), 733.

- van Dam, A., Keijsers, G.P., Eling, P.A., & Becker, E.S. (2011). Testing whether reduced cognitive performance in burnout can be reversed by a motivational intervention. Work & Stress, 25(3), 257-271.

- van Dam, A., Keijsers, G.P., Eling, P.A., & Becker, E.S. (2012). Impaired cognitive performance and responsiveness to reward in burnout patients: Two years later. Work & Stress, 26(4), 333-346.

- Yuguero, O., Ramon Marsal, J., Esquerda, M., Vivanco, L., & Soler-González, J., (2017). Association between low empathy and high burnout among primary care physicians and nurses in Lleida, Spain. European Journal of General Practice, 23(1), 4-10.

- Zimbelman, M.F., (1997). The effects of SAS No. 82 on auditors' attention to fraud risk factors and audit planning decisions. Journal of Accounting Research, 35, 75-97.

- Zopiatis, A., & Constanti, P., (2010). Leadership styles and burnout: is there an association? International Journal of Contemporary Hospitality Management, 22(3), 300-320.