Research Article: 2021 Vol: 25 Issue: 4

Controllings Accounting Support at Trading Companies in the Context of Sustainable Development

Valentyna Kostyuchenko, Kyiv National University of Trade and Economics

Anastasiia Kamil, Kyiv National University of Trade and Economics

Pavlo Petrov, Kyiv National University of Trade and Economics

Liubov Kolot, Kyiv National University of Trade and Economics

Iryna Mykolaichuk, Kyiv National University of Trade and Economics

Abstract

Intensification of trade relations, growth of their dynamics, expansion of geographical direction are the objective consequences of the globalization processes in the modern world. International scientific community pays a lot of attention to the problem of ensuring the sustainable development of economic systems, especially in the Western world. Implementation of sustainable development concept by enterprises is an important condition for belonging to the most progressive market participants. Ukrainian trade enterprises, which are focusing on integration with the European Union (EU), should implement the most advanced practices of this concept. There are two main points in transition to sustainable development: to build system of essential indicators and to choose an effective mechanism for quantitative and qualitative assessment of this very complex and multifaceted process. The measurement system must convey clearly and fully information on the state of the components of sustainable development. Usually, indicators that were developed and proposed by international organizations require a large amount of information, which is sometimes hard to obtain. Thus, there is a need to improve accounting support of sustainable development that would allow management and society to assess the effectiveness of the chosen strategy in this context. Of particular importance in these conditions is controlling, as a functionally separate area of economic work in a commercial enterprise. Modern company management needs to make decisions based on a large amount of information, which is often simply impossible to fully cover and properly evaluate in a short time. Controlling helps to solve this issue as it provides managers with already analysed, generalized information that is directly related to the problem that needs to be solved. Nowadays, it's very important that controlling's accounting support at the trade enterprise reorients the vector of its activity considering the goals of sustainable development.

Keywords

Controlling, Sustainability, Indicator, Accounting Support, Trade Enterprise.

JEL Classifications

F17, M41, Q01, Q56.

Introduction

Today, trading companies around the globe operate in conditions of high uncertainty and dynamism of the external environment, fierce competition and crises in both economic and environmental spheres. Ukrainian trade enterprises are no exception. The development of Ukraine's economy, integration into the European community and the market, high competitionin the world market, as well as the current socio-environmental situation encourage companies to seek new ways and directions of development. The new system of values of society requires a change in the target settings of enterprise development. Priority is given to its socio- environmental aspects, which, in turn, requires a reorientation of views on the choice of criteria for development and assessment of effective economic growth. This change in priorities necessitates a more detailed study of the development of the trading company as a socio- ecological system (Lepeyko & Mazorenko, 2017).

In the context of sustainable development, society's demand for information on global challenges, including poverty, gender inequality, climate change, environmental degradation, peace and justice, is increasing. Now, in the developed countries of the world 80% of the 250 largest companies have non-financial reporting, and among developing countries with 2.2 thousand companies - 45%. However, in contrast to the international practice in Ukraine (Vorobey, 2019), among the 100 largest companies, only 10% compile and publish such reports. This situation significantly complicates the receipt of complete and reliable information about the environmental and social activities of enterprises in compliance with all standards during the sale of products and prevention of negative environmental impact. At the heart of solving these issues of managing the sustainable development of the enterprise is controlling, which allows a holistic, comprehensive approach to the process of various subsystems' interaction that are involved in managerial procedures.

Literature Review

Theoretical and methodological aspects of controlling and its implementation have found some coverage in the works of such leading scientists (Verzhbytskyy, 2009; Holov, 2007; Babyak, 2007; Pushkar, 2004; Mayer E., Mann R. and others). An important role in the scientific development of issues of sustainable development management of enterprises belongs to such scientists as Ackoff (2002), Galbraith (1979), Drucker (2008), Karloff (2004), Fayol (1992), who considered the development of enterprises from the standpoint of society, the development of management theories, firms. Ukrainian scientists have made a thorough scientific contribution to the development of the methodoloy for assessing the management of sustainable development of various socio-economic systems: Bilous (2006), Vasyutkina (2014), Herasmchuk (2007), Karpinskyy (2005) and many others, which focused on economic, social, environmental, corporate systems and their formation and interaction in strategic development.

Review of Sustainability Requirements to Businesses

The key idea of sustainable development is to find a ratio of nature management and socio-economic development that would ensure the efficient use of natural resources, maintain the environmental security of society and guarantee the necessary quality of life and well-being of the population (Dovgan, 2008). European law requires that all EU policies, including trade, promote sustainable development. As emphasized in the Sustainable Development Strategy (2006), the EU and its Member States are committed to making efforts to use international trade and investment as a means to achieve the goals of sustainable development, namely:

1. Adhere to international labour and environmental standards and agreements;

2. Effectively apply their environmental and labour legislation;

3. Do not deviate from environmental and labour laws to encourage trade;

4. Ensure sustainable trade in natural resources, such as timber and fish resources;

5. Fight against illicit trade in species of flora and fauna that are threatened with extinction;

6. Encourage trade that supports the fight against climate change;

7. Promote practices such as corporate social responsibility.

Consideration of trade activities of enterprises through the prism of sustainable development affects both its controlling's accounting support and the organization as a whole. The reliability of the prepared and submitted reports is the basis for the successful operation of economic entities. Hence, there is a need to improve accounting support of sustainable development reporting, which is the main base for the formation of indicators. Analysis of existing indicators for assessing sustainable development at the enterprise level, proposed by a group of scientists: Vakhramov & Markaryan (2008), Kondaurova (2012) Parshyn Yu. (2016) and at the national and international levels proposed by the UN Commission, the Organization for Economic Co-operation and Development, and the World Bank, European Community, Institute of Applied Systems Analysis of the National Academy of Sciences of Ukraine and the Ministry of Education and Science of Ukraine (Zgurovskyy, 2009) allowed to establish that the algorithm for calculating the level of sustainable development is based mainly on indicators of financial sustainability. To overcome these problems, the Global Reporting Initiative (GRI) published the 2002 GRI Sustainability Reporting Guidelines based on the concepts of sustainable development (Lin & Wang, 2004; Thompson, 2002). The GRI guidelines propose principles and general indicators to report an organization’s performance in terms of the TBL: economic, environmental, and social dimensions. Indicators for sustainable business practices can be expressed in many different forms (e.g., qualitative or quantitative, general or specific, and absolute or relative), in accordance with objectives and applications of an indicator. Quantitative indicators are measured in terms of mass, volume or number of environmental pollutants or physical materials (Smardon, 2011).

Based on this, we strongly recommend to look at controlling's accounting support at the trading company in combination with environmental and social points of view, as these processes are interrelated and affect the economic component of the firm. After studying the reports on sustainable development of international trade enterprises, such as Adidas (2020), METRO (2020), Morrison's (2018), Apple (2019), Tesco (2016) and others, the most commonly used indicators of sustainable development were identified in Table 1.

| Table 1 The Most Popular Sustainability Indicators of Trade Enterprises | ||

| Economic | Environment | Social |

|

energy and water consumption

|

|

It should be noted that when using foreign experience, in the process of choosing indicators for Ukrainian trade enterprises, it is necessary to take into account the specifics and economic features of Ukraine. However, the correction of traditional economic indicators considering environmental and social factors can lead to their significant reduction, and sometimes to negative values (Filipishina, 2017). In addition, the dominance of the accounting and analytical component in controlling has led to the fact that business leaders are increasingly dissatisfied with the controlling services, blaming them for being too trivial and obsessed with in-depth analysis of financial and managerial accounting data (Panasyuk, 2016).

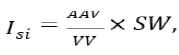

To solve the above problems, we have proposed an Integrated sustainability indicator (ISi), which is based on a comprehensive and systematic approach to research, which allows to present the sustainable development of a commercial enterprise as a multicomponent phenomenon in the form of a set of factors of sustainable development and indicators that shape them.

(1)

(1)

?AV - actual average value of the indicator

VV - valid value of indicator

SW - specific weight

In the calculation (1), we use the ratio of actual data (based on selected sustainable development criteria) (AAV) to their normative values (VV), multiplied by the proportion of each (SW). To test the presented integrated assessment of sustainable development, we conducted a survey among trade enterprises in Ukraine. The sample combined retailers and wholesalers, including 17 large, 13 medium and 7 small firms. As an example, we chose the "environmental component" which consists of 5 criteria for sustainable development Table 2.

| Table 2 Trade Enterprises' Poll Data Summary | |||||||

| Environment criteria | Large trade enterprises | Medium trade enterprises | Small trade enterprises | SW | |||

| AVV | VV | AVV | VV | AVV | VV | ||

| Noise pollution, dB | 57,3 | 60 | 59,1 | 50 | 58,40 | 40,00 | 0,2 |

| Energy consumption, kJ/year | 4,5 | 4,2 | 1,9 | 2,1 | 1,10 | 1,07 | 0,2 |

| Solid waste disposal, kg/m³ | 80 | 77 | 49,7 | 52 | 33,00 | 34,00 | 0,2 |

| Wastewater treatment, kg/m³ | 47,8 | 50 | 41,2 | 40 | 31,60 | 30,00 | 0,2 |

| Recycling of raw materials, kg/m³ | 161 | 180 | 150,8 | 154 | 101,1 | 112 | 0,2 |

After data collection, we calculated ISi for each of the enterprises Table 3 and compared them with the normative values (Standard) contained in the legislation of Ukraine. The smaller difference between the value of ISi and Standard, the higher level of compliance of the enterprise with the reference criteria for sustainable development. The results of the calculations showed that only large enterprises fully meet the regulatory values. The explanation of this is: if you want to meet the goals of sustainable development, in particular, environmental standards, constant funding is needed. In the meantime, for Ukrainian SMEs this is a quite problematic, especially during a pandemic.

| Table 3. Trade Enterprises` Ecological Results Comparison | |||||||||

| Criteria | ??? Large | Stand ard | ??? Mediu m | Stand ard | ??? Small | Stand ard | Deviation, % | ||

| Large | Medium | Small | |||||||

| Noise pollution, dB | 11,5 | 12 | 12 | 10 | 12 | 8 | 4,71 | -15,40 | -31,51 |

| Energy consumption, kJ/year |

0,9 | 0,84 | 0,4 | 0,42 | 0,2 | 0,2 | -6,67 | 10,53 | -2,73 |

| Solid waste disposal, kg/m³ | 16 | 15,4 | 9,9 | 10,4 | 6,6 | 6,8 | -3,75 | 4,63 | 3,03 |

| Wastewater treatment, kg/m³ | 9,56 | 10 | 8,2 | 8 | 6,3 | 6 | 4,60 | -2,91 | -5,06 |

| Recycling of raw materials, kg/m³ | 32,1 | 36 | 30 | 30,8 | 20 | 22 | 11,89 | 2,19 | 11,18 |

| Total, points | 70,1 | 74,2 | 61 | 59,6 | 45 | 43 | 5,91 | -1,49 | -3,43 |

Integrated sustainability indicator will allow the controller to identify and analyse deviations from the established norms in time, and also will provide a number of advantages:

1. Simplicity - can be calculated on demand by both the controller and the manager of any level.

2. Efficiency - availability of data for estimation.

3. Complexity - taking into account all components and factors of sustainable development.

4. Versatility - the ability to use regardless of the size or nature of the trading company.

5. Conciseness - the results of the calculation are clear to both external and internal users.

In this case, indicator ISi serves as centre for providing accurate state of accounting information for controlling of environmental performance indicators of the enterprise. As noted by Pushkar M. (2008) system of controlling has place for all subsystems of accounting, which form the database, determining the content, selection and evaluation of data, a set of economic indicators that characterize the quantitative and qualitative state of objects, as well as factors influencing their functioning. Having generalized data ISi on each of the elements of sustainable development, controller can advise senior management how to fully reflect the activities of each structural unit of the enterprise, as well as the level of detail of actual data, which is determined by the ability to collect info and the need for all management levels.

Conclusion

Modern business must quickly adapt to changes in the environment without which it is impossible to secure its future. The activity of any organization is manifested in the constant development, activity, identification of new and new opportunities, the disclosure of existing potential, which allows to increase its revenues. Properly chosen vector of the company's development is an integral part of its organization, which can ensure the viability of the organization, and this can only contribute to a comprehensive and in-depth assessment of sustainable development of the enterprise. In addition, it will find vulnerabilities and develop a set of measures to overcome negative consequences and improve activities of developed sectors of the structure. The introduction of controlling in the practice of a commercial enterprise is an objectively determined necessity, as well as a prerequisite and basis for creating an appropriate information base for making sound management decisions and monitoring their implementation. The role of controlling's accounting support is to identify changes in the external and internal environment based on the information obtained and to develop a strategy for sustainable development. The use of the Integrated sustainability indicator will allow to systematize such credentials for their further interpretation by controller and further by company's management. The system of controlling's accounting support is able to determine the sustainable development of trade entrepreneurship, however, only in terms of its competent organization, compliance with legal requirements, and most importantly - the availability of highly qualified specialists in this field. Because otherwise accounting can become a means of fraud, falsification, criminal acts, which can result in negative consequences both at the enterprise level and at the state level as a whole.

References

- Ackoff, R. (2002). About management. Saint-Petersburg, Piter. Adidas: Environmental impacts. Retrieved April 3, 2021, from https://report.adidas-group.com/2020/en/group-management-report-our-company/sustainability/environmental-impacts.html

- Azapagic, A. (2003). Systems approach to corporate sustainability: A general management framework. Trans IChemE, 81(B), 303-316.

- Babyak, N. (2014). Management accounting in the concept of the theory of constraints as a tool for strategic controlling at enterprises. Moscow, NPP Association of Controllers.

- Pushkar, M. (2004). Controlling: information subsystem of strategic management. Ternopil, Carte-blanche.

- Bilous, O. (2006). Global perspective and sustainable development. Kyiv, Interregional Academy of Personnel Management.

- Drucker, P. (2008). Effective enterprise management. Moscow, Williams.

- Fayol, A. (1992). General and industrial management. Journal Controlling, 112-116.

- Flilipishina, L. (2017). Intergral assesment of develomental stability of industrial enterprises. Global and national economic problems. Retrieved April 3, 2021, from http://global-national.in.ua/archive/19-2017/56.pdf

- Galbraith, J. (1979). Economic theories and goals of society. Moscow, Politizdat.

- Heresamchuk, V. (2007). Management vector of the economic component of sustainable development: Ukraine and the world. Economist, 9, 7-9

- Holov, S. (2007). Managerial accounting and controlling: concepts and applications. Bulletin of KNUTE, 5, 82-87.

- Karloff, B. (2004). Business strategy. Kyiv, Minorka

- Karpinskyy, B. (2005). Sustainable economic development: a generalized model.

- Kondaurova, D. (2012). Improving the mechanism of sustainable development of an industrial enterprise. Economics, management, finance: materials of the II international scientific conference, 130-132.

- Lepeyko, E., & Mazorenko, O. (2017). Development of the enterprise as a socio-ecological

- Lin, L., & Wang, L. (2004). Making sustainability accountable: A valuation model for corporate performance, Proceedings of the 12th IEEE international Symposium on Electronics and the Environment (ISEE) and the 5th Electronics Recycling Summit, 7-12.

- METRO , (2020). Key performens indicators and targets. Retrieved April 3, 2021, from https://reports.metroag.de/corporate-responsibility-report/2019-2020/key-performance-indicators-and- targets/key-performance-indicators.html

- Morrison's. (2018). Corporate responsibility report 2017-2018. Retrieved April 3, 2021, from https://www.morrisonscorporate.com/globalassets/corporatesite/corporateresponsibility/documents/2018/morrisons_cr_report_2018.pdf

- Panasyuk, V. (2008). Implementation of the controlling system and its impact on efficiency enterprise management. Collection of abstracts based on the materials of the scientific-practical conference: Prospects for the development of controlling as a science: theory and practice, 89-93.

- Parshyn, Y. (2016). The strategy of securing the economic development of the national government: theory, methodology and practice. Dnipro, University named after Alfred Nobel.

- Pushkar, M. (2008). Controlling concept. Collection of abstracts based on the materials of the scientific- practical conference: Prospects for the development of controlling as a science: theory and practice, 7-24.

- Smardon, R. (2011). Indicators of Sustainable Business Practices. State University of New York College of Environmental Science and Forestry. Retrieved April 23, 2021, from https://www.researchgate.net/publication/221912924_Indicators_of_Sustainable_Business_Practices

- Tesco, (2016). corporate responsibility update 2019. Retrieved April 3, 2021, from https://www.tescoplc.com/media/391787/corporate-responsibility-update_nov-2016-final.pdf

- Thompson, D. (2002). Tools for Environmental Management: A practical Introduction and Guide New Society, BC VOR/

- Vakhramov, Y., & Markanyan, D. (2008). Assessment of sustainable development and functioning of the enterprise: factors, criteria, features. Bulletin of the Astrakhan State Technical University, 4, 52-62.

- Vasyutkina, N. (2014). Management of sustainable development of enterprises: theoretical and methodological aspect.

- Kyiv, & Lira-KVerzhbytskyy, O. (2009). Process controlling in commercial enterprises. Bulletin of Socio-Economic Research, 36, 21-26

- Vorobey, V. (2019). What non-financial reports are silent about. Retrieved April 18, 2021 https://delo.ua/business/o-chem-molchat-nefinansovye-otche-142846/

- Zgurovskyy, M. (2009). Sustainable development of the regions of Ukraine. Institute of Applied Systems Analysis of the National Academy of Sciences of Ukraine and the Ministry of Education and Science of Ukraine. Kyiv, National Technical University of Ukraine Igor Sikorsky Kyiv Polytechnic Institute.