Research Article: 2022 Vol: 25 Issue: 1S

System approach as a paradigm for the development of business processes

E. Yu. Sidorova, Financial University under the Government of the Russian Federation

L. V. Polezharova, Financial University under the Government of the Russian Federation

I. V. Muradov, National University of Science and Technology MISIS

D. K. Savinova, National University of Science and Technology MISIS

I. V. Lipatova, Financial University under the Government of the Russian Federation

O. O. Skryabin, National University of Science and Technology MISIS

Citation Information: Sidorova, E. Y., Polezharova, L. V., Muradov, I. V., Savinova, D. K., Lipatova, I. V., & Skryabin, O. O. (2022). System approach as a paradigm for the development of business processes. Journal of Management Information and Decision Sciences, 25(S1), 1-10.

Abstract

The improvement of the process of calculating the capability of manufacturing a new product at the enterprise is described in the study. To achieve high profitability indicators of business processes, their radical redesign is required. For this purpose, reengineering is applied through a process approach to management. The object of the study was Novolipetsk Steel PJSC, the main production site of the international NLMK Group. The presented figures and tables were the result of analytical work performed by a team of researchers. The scientific novelty consisted in clarifying the definition of a business process and developing an economic model for the process of analyzing the capability of manufacturing new products. As a result, the concept of a business process was formulated, an economic model was developed for analyzing the capability of manufacturing new products and the characteristics of this process were identified. The capability of obtaining an economic effect from improving the business process was justified. At the same time, the specified business process was organized from the point of view of a system approach so that it can be replicated in the case of business enlargement in the form of a proven algorithm.

Keywords

Business process; System approach; Process approach; Process construction.

Introduction

The review of the literature was carried out according to the systematic review process defined by Centobelli et al. (2020); Altarawneh et al. (2020) and Wadesango et al. (2020) that are well-known in the field of literature reviews concerning managerial topics. Activities aimed at creating a specific product or services are described as a business process by modern management science. At the same time, there is no single definition of a business process at the moment. Erickson in his study (Ericsson Quality Institute, 1993) proposed the following definition: “a business process is a chain of logically connected, repetitive actions that use the resources of an enterprise to process an object (physically or virtually) in order to achieve certain measurable results or products to satisfy internal or external consumers”. The authors of the reengineering concept M. Hammer and J. Champy (1993) define a business process as “a set of different activities, within which one or more types of resources are used “at the input” and as a result of this activity, a product is created “at the output” that is of value to a consumer”. B. Anderson (2003), agreeing with the definition of Erickson, classified business processes in terms of the possibility of their improvement. M. Porter (1980;1985;2006) classifies all business processes of the company in terms of their participation in the creation of values perceived by customers: the main (primary) (which directly create a set of values), serving (secondary) business processes (not directly involved in the creation of values, but necessary for the normal functioning of the main business processes) and management processes that coordinate the activities of the two above-mentioned groups. Russian authors formulate the definition of a business process as follows: a stable, purposeful set of interrelated activities that, using a certain technology, transforms inputs into outputs that are valuable for a consumer (a client) (Repin, 2013; Kostyukhin, 2016, 2019; Kruzhkova et al., 2018; Kostyukhin & Savon, 2020).

There is also a significant number of works that apply the process approach in various areas of the economy to describe the business models of companies (Erasmus et al., 2020; Waszkowski & Nowicki, 2020). According to ISO 9001-2015 (Rosstandart, 2015), the process approach includes the systematic identification and management of processes and their interactions in such a way as to achieve intended results in accordance with the quality policy and strategic direction of the organization. From our point of view, it is appropriate to supplement the definition of a business process with the imperative of making a profit as a result of its application, since making a profit is the main goal of any business (Barcho et al., 2020; Samarina et al., 2020).

The scientific novelty of the study lies in the clarification of the definition of the business process within the framework of the use of the process approach to the preparation of the release of new products and the development of an economic model of the process of analyzing the possibility of manufacturing new products. The research objectives consisted of the study of problematic elements of the process of developing a new product at an enterprise, determining the possibility of improving the process using reengineering methods and developing an economic model for analyzing the possibilities of producing new products.

Methodology

The research methodology is based on the system approach that assumes that any system consists of interrelated elements and it is simultaneously an element of a higher-order system. For this reason, the use of only analytical research methods in these conditions is not enough. Although the system approach does not deny analytical methods of cognition, analysis must be complemented by synthesis. As a method of improving business processes in the study, the method of re-engineering through a process approach to management was chosen. The process approach used in the study made it possible to create an integration scheme of the functional area “Budget Management".

Results and Discussion

The object of the study is NLMK PJSC, an enterprise with a full metallurgical cycle: from the production of raw materials for the iron and steel smelting to the final product, i.e. flat rolled metal with high added value. All business processes of NLMK PJSC should be divided into a sequence of functional areas, including the management of the following objects: budget, personnel, costs, production, finance, maintenance and repairs, sales, purchases.

The main tasks of these areas are discussed below. The fundamental task of the “Budget Management” functional area is the formation, control and maintenance of the execution of the cash flow budget. The integration scheme for the “Budget Management” functional area is shown in Figure 1.

Figure 1: The Integration Scheme For The “Budget Management” Functional Area

As can be seen, the “Budget Management” business process is built into the overall enterprise management system and it is closely interconnected with other business processes. Other functional areas are similarly integrated into the overall management system. For example, the integration scheme of the “Personnel Management” functional area is shown in Figure 2.

Figure 2:The Integration Scheme Of The “Personnel Management” Functional Area.

The main tasks of other functional areas are further discussed:

1. “Accounting/Finance” is the organization of activities for the maintenance of accounting and tax accounting of operations and financial and economic activities of the organization. 2. “Procurement and material flows” is material and technical support of the enterprise and inventory management in all warehouses. 3. “Sales” is responsible for sales of NLMK products. 4. “Maintenance and repairs” is responsible for ensuring uninterrupted operation of equipment, as well as excluding defects, unplanned downtime, and accidents. 5. “Manufacturing control” is responsible for production planning and management and quality control at every stage of production.

In the process of forming and implementing business processes at NLMK PJSC, a number of problems were identified in each of the described functional areas. The main problems of business processes at NLMK PJSC are summarized in Table 1.

| Table 1 The Main Problems Of Business Processes At Nlmk Pjsc |

|

| Functional area | Main problems |

|---|---|

| Cost management | a) Incompleteness of the necessary regulatory base for accounting; b) Difficulty in coordinating plans of various structural divisions manually. |

| Budget management | a) Lack of automation of procedures for the formation and execution of the budget; b) Duplication of data entry into various systems; c) Lack of integration among systems. |

| Accounting/Finance | a) Fragmentation of information resulting from the use of various software; b) Slowdown of information flows. |

| Procurement and material flows | a) Lack of centralized management of main data, miscellaneous data. |

| Sales | a) Lack of a fully automated subsystem for supporting sales functions. |

| Maintenance and repairs | a) Lack of an automated system. |

| Manufacturing control | a) Lack of methods for forming standards for the consumption of goods and energy resources; |

| Personnel management | a) Repetition of human resources data; b) Need to transfer information between various functional personnel. |

Based on the identified problems at this stage, it was decided to optimize the process of calculating the capability of manufacturing a new product. As a method of improving the process of calculating the capability of manufacturing a new product in the study, the method of reengineering using a process approach to management was chosen.

The calculation of the capability of manufacturing a new product usually begins with receiving a request from a customer. The indicators of this process were identified as the duration of the process (implementation time); compliance with the requirements of local internal regulations (LIR); the number of errors in the calculations of the capability of manufacturing.

The “process duration” indicator characterizes the calculation execution time that passed from the moment of receiving an order for the production of a new type of product to giving a response to a customer about the capability of manufacturing the ordered products. This indicator is influenced by two groups of factors: objective and subjective. Objective factors include the workload of a specialist performing the calculation and the complexity of the calculation. Subjective ones include unforeseen situations, such as illnesses of a specialist performing the calculation.

The “compliance with the LIR requirements” indicator during the implementation of the process is characterized by the number of deviations from the LIR requirements during the implementation of the process. For example, non-compliance with the terms of calculation or the procedure for calculating the capability of manufacturing products.

The “number of errors in the calculation of the capability of manufacturing” indicator characterizes the number of erroneous conclusions about the capability or incapability of manufacturing a new product.

The model allows noting that the process of calculating the possibilities of manufacturing products with new parameters is performed manually. To optimize and improve the efficiency of NLMK PJSC, it was decided to use the business process reengineering method.

The reengineering method includes several stages, each of which is aimed at improving the performance of the enterprise.

A matrix of SWOT analysis of the strengths and weaknesses of reengineering was compiled and the weak and strong sides of the process approach to business process management were also analyzed.

The described strengths and weaknesses of the selected methods were further taken into account.

The main stages of business reengineering implementation included:

a) The development of a future state model; b) The analysis of the current state of the enterprise, construction of current schemes of functioning; c) Development of a new model of the enterprise or processes, as well as testing the activities of the new model; d) Introduction of the new model into the activities of the enterprise.

Based on the results of the SWOT-analysis, a model of the “as it will be” process for analyzing the capability of manufacturing new products was built. In the “as it will be” process, manual analysis was replaced by the analysis performed by a software product.

Any project must have a planned implementation period, for this it is necessary to set its duration for each stage of the project, determine which stages can go in parallel with others and determine the start date of the project.

To calculate the duration of the project, the network graph was used and a Gantt chart was also built.

The early or expected time period tp(i) of the ith event can be determined by the duration of the maximum path that precedes this event according to formula 1.

Where Lni is any path that precedes the ith event.

For i=0 (initial event), obviously tp(0)=0.

t(1)is further calculated, using formula 2.

For i=1: 0 + 1 = 1

Similarly, using formula 2,t(2-26) is calculated and the calculations of t(3)are also presented:

i=26: tp(27) = tp(26) + t(26,27) = 158 + 3 = 161.

Thus, the project implementation period is 161 days.

The network model over time is further analyzed. Critical path length is 161 days. The Gantt chart is presented in Figure 3.

Figure 3:The Gantt Chart.

The economic assessment of the effectiveness of the study was also carried out.

To calculate the project implementation costs and the amount of possible effect, an economic model of the process is developed.

Project development and implementation costs are calculated using the following formula:

Where: L is the labor coefficient of the development and implementation of the project by the employees of NLMK, man-hour;

DRsn is standard deductions rate for social needs;

CIC is the coefficient of indirect costs of the organization engaged in the development and implementation;

W is average hourly wages of NLMK specialists involved in development, rubles.

COS is cost of services for the development and implementation of the project of an outsourcing organization invited to implement “1C:Metallurgical plant management” and develop an application for it;

C1c is cost of the 1C software product, RUB.

The Cdip indicator is calculated based on the following numbers:

The number of working days in a month is 22;

The number of working hours per day is 8;

The wages of NLMK workers involved in the development of the improvement project, the number of plant specialists participating in the project is 10 people (a chief technologist, a chief metallurgist, 2 managers of the chief technologist's department, 2 managers of the chief metallurgist’s department, 4 programmers of the plant) - 350,000 rubles, hence the average hourly wages of plant specialists participating in the plant is 199 rubles/hour.

The coefficient of indirect costs of NLMK PJSC is 10% and the standard deductions rate for social needs is 30%.

Prior to the implementation of this project, the company used the software product “1C: Production enterprise management” and industry solutions based on it. As a result, to create a comprehensive enterprise management information system, it is recommended to use "1C: ERP Enterprise Management 2".

To implement the project, the purchase of “1C: Enterprise 8 PROF.ERP Enterprise Management”, the total cost of the “1C” package amounted to 3488,000 rubles. The cost of services provided by the partner organization of 1C Company, which implement the software product and develop the application, is approximately 1500,000 rubles. The total labor coefficients 1816 people per hour.

The one-off project implementation costs are calculated using the formula 4:

In addition to those included, the cost of development and implementation includes the cost of electricity for the operation of computers.

The cost of 1 kW for legal entities is 3.52 rubles, then the cost of electricity for the project Cel is 623.4 rubles.

The total costs TC of development and implementation were also calculated:

The main economic effect when implementing software and applications for process automation is achieved due to two factors:

1. Reduction of the time spent by the plant's specialists;

2. Reduction of customer churns due to long waiting for a response.

Labor savings are achieved by reducing the analysis time by automating the process. The calculation of savings due to reduced labor costs was made using formula 5.

Where W is average hourly wages of NLMK specialists involved in development, rub;

T1is engineering hours for the year before the implementation of the improvement;

T2is engineering hours for the year after the implementation of the improvement;

DRsnisstandard deductions rate for social needs;

Wis199 rubles/hour based on the above calculation.

The average number of analyses of the capability of manufacturing new products per year at NLMK is on average 15.

The average analysis time was about 160 hours, but this analysis was carried out on average for 35-40 days, since the analysis is a chain of sequential actions of different performers.

The average analysis time after automation is 3 hours. In its pure form, the analysis process takes significantly less time, but the need for coordination with a chief technologist or a chief metallurgist increases the required time.

The average repair time after the implementation of the 1C system is 24 hours. The average number of repairs per year is 70.

Based on the data provided, the values T1 and T2 were calculated using the following formula:

Where Q' is number of tests performed per year;

T' is time spent on one analysis.

Thus, according to formula 6:

T1=15.160= 2 400hours,

T2= 15.24 = 360hours,

Labor savings are calculated using formula 5.

However, saving on labor costs is not the main benefit of optimizing this process. The practice of the Sales Department shows that due to the long wait for a response, NLMK loses at least 3 contracts a year, each of which could bring a minimum profit of 2 million rubles. Using the minimum number of lost contracts and the minimum amount of profit that they can bring, it turns out that the plant can earn an additional 6 million rubles annually. Adding these 6 million to the savings on labor costs, the plant could get 6,418,138.8 rubles of additional funds received annually.

Such indicators as return on investment and payback period were further calculated. In this situation, the return on investment (ROI) can be calculated using the following formula:

Where ROI is economic effect of the proposed event; Ieis investments (one-off costs) for the implementation of the event. The return on investment (ROI) according to formula 7 is:

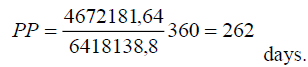

Payback period of investment (PP) is a time period for which funds invested in events (one-off investments) will be returned in the form of additional profit, calculated using the following formula:

According to formula 8, payback period (PP) of investment is:

The calculations allow concluding that reengineering of the business process “the analysis of the capability of manufacturing new products” is an effective measure.

Conclusion

As a method of improving business processes, the method of reengineering through a process approach to management was chosen in the current study. The economic model of the process of analyzing the capability of manufacturing new products was developed and the characteristics of the process of analyzing the capability of manufacturing new products were also presented. The process costs were classified and a process map was constructed.

As part of the study, it was proposed to supplement the definition of a business process with the imperative of making a profit. Thus, we understand a business process as “a stable, purposeful set of interrelated activities that, using a certain technology, transforms inputs into outputs that are of value to the consumer”, ensuring profit for a manufacturer.

As a result, the economic efficiency of the reengineering project was proved. Practical application of an economic model of the process of analyzing the capability of manufacturing new products will increase the efficiency of the production cycle and simplify the decision to start production. At the same time, the introduction of an improved business process into the practice of the enterprise must ensure significant economic effect. The main economic effect was achieved by reducing the time spent by specialists on the process of analyzing the capability of manufacturing new products and reducing customer losses due to a long wait for a response about the capability of manufacturing.

References

Altarawneh, M., Shafie, R., & Ishak, R. (2020). CEO Characteristics: A Literature Review and Future Directions. Academy of Strategic Management Journal, 19(1), 1-10.

Anderson, B. (2003). Business processes. Improvement toolbox. Transl. from English by S.V. Arinicheva, sci. ed. Yu.P. Adler. Moscow: RIA “Standards and Quality”, pp.272.

Ericsson Quality Institute (1993). Business Process Management. Gothenburg, Sweden: Ericsson.

Kostyukhin, Y., & Savon, D. (2020). Improving steel market performance indicators in the fact of increased competition. Chernyemetally, 4, 68-72.

Kostyukhin, Y.Y. (2016). Enhancement of labor efficiency in coal mining industry.GornyiZhurnal, 10, 41-44.

Kruzhkova, G. V., Kostyukhin, Y. Y. &Rozhkov, I. M. (2018). Choice procedure for expedient composition of electronic waste.Mining Informational and Analytical Bulletin, 9, 47-57.

Porter, M. E. & Millar, V. E. (1985). How Information Gives You Competitive Advantage. Harvard Business Review, 63(4), 149-160.

Porter, M. E. (1980). Competitive strategy: techniques for analyzing industries and competitors. New York: Free Press (republished with a new introduction, 1998).

Porter, M. E. (1985). Competitive advantage. Creating and sustaining superior performance. New York: Free Press.

Repin, V. V. (2013). Biznes-processy. Modelirovanie, vnedrenie, upravlenie [Business processes. Modeling, implementation, management]. Moscow: Mann, Ivanov and Ferber (in Russian).

Rosstandart. (2015). GOST R ISO 9001-2015. National standard of the Russian Federation. Quality management system. Requirements (approved by the order of Federal Agency on Technical Regulating and Metrology of September 28, 2015 No. 1391-st) (with “Explanation of the new structure, terminology and concepts”, “Other international standards in the field of quality management and on quality management systems developed by ISO/TC 176”).