Research Article: 2018 Vol: 17 Issue: 6

An Empirical Study of Key Factors to Effectively Operate Strategic Performance Management System

Michaela Striteska, University of Pardubice

David Zapletal, University of Pardubice

Lucie Jelinkova, University of Zilina

Abstract

Measuring performance is a fundamental aspect of successful management systems, which are focused on implementing strategy and maintaining competitive advantage. Effective performance measurement must be founded on systematic and comprehensive research on company activities and results in order to constantly develop key competencies. This paper is comprised of a number of sections that tie into each other thematically. First, an effective strategic performance management system and factors that influence its implementation are defined from a theoretical perspective. Then, the methodology and research methods used in the paper are described. The next step for the companies being investigated was to identify their strategic performance management system’s development level according to whether it encompasses characteristics indicated in the literature and whether a number of key factors are demonstrably managed. Only then does the paper proceed to investigate the relationship between the strategic performance management system’s level of development and both the length of time it has been implemented as well as key factors that are currently managed.

Keywords

Performance Measurement, Performance Management, System, Strategy, Effectiveness.

JEL Classification: M14, M21, M29.

Introduction

Recently, performance management systems (hereinafter PMS) have been increasingly becoming a significant part of organizations, enterprises, and academia, which spend large sums on developing comprehensive methods of performance measurement (Taticchi, 2008; Franco- Santos & Bourne, 2005; Kennerley & Neely, 2002). Certain authors even speak about the revolution that performance measurement has undergone in recent years (Kennerley & Neely, 2002; Neely et al. 1995). This has occurred because the entrepreneurial environment has been undergoing changes (mainly, market globalization, new sources of competitive advantage, the need to quickly transfer information, and fast decision making) that call for revising current PMSs (Seethamraju & Marjanovic, 2009). These changes have led to criticism of traditional control and accounting systems, which ignore strategically important performance drivers (knowledge, reputation, branding, and relationships) and focus too intently on internal organization, the bottom line, lagging indicators, and yesterday’s performance (Pedersen & Sudzina, 2012; Bourne & Neely, 2002).

Therefore, the objective of the new type of PMS is to achieve greater balance between performance measures that are financial and non-financial, short- and long-term, backward- and forward-looking, leading and lagging, focused on stockholders and stakeholders, and internal and external (Kennerley & Neely, 2002; Kaplan & Norton, 1992; Brignall et al., 1991; Keegan et al., 1989). Using a PMS that is designed in this way improves a company’s orientation in the new business environment, speeds up and improves the quality of decision making processes, and makes it easier to implement strategy. Moreover, performance measurements align employees’ incentives and motivate them to enhance performance and achieve the strategic goals (Simons et al., 2000).

Therefore, over the last two decades, a number of scientific studies have been conducted that deal with various aspects of performance measurement: the extent performance measures’ use (Gomes et al., 2011; Robinson et al., 2005; Frigo & Krumwiede, 1999; Stivers et al., 1998), defining performance measurement systems (Franco-Santos et al., 2007; Bourne & Bourne, 2002; Forza & Salvador, 2000), the creation and implementation of PMS (Atkinson, 2012; Robinson et al., 2005; Bourne et al., 2000), and new trends (Yadav & Sagar, 2013; Marr & Schiuma, 2003). However, there is no unified theory or clear agreement concerning the factors and contexts that influence the implementation and continual improvement of strategic performance management system (hereinafter SPMS) (Henri, 2006). There is very little discussion about the quality of information and the linking of performance and strategic management.

Despite this, a number of internal factors influencing the implementation of PMS have been identified. These include size, strategy, organizational culture, organizational structure, management style, the process of reviewing measures, and systems for collecting and analyzing data. External factors that influence companies-and, thereby, also a performance measurement system’s requirements-include new technologies, increasing global competition, increasing customer bargaining power, and cultural differences (Aguinis et al., 2012; Claus & Hand, 2009). Another internal factor cited is the maturity of the PMS. The question is whether it is valid to assume that a company’s experience acquired during the development and implementation of a SPMS influences the system’s level of development. Just as interesting is the research question of whether companies that spend sufficient energy managing key factors (company culture, competent people, review process, and information system) have a more developed SPMS. Key factors are considered to be those that are most frequently cited in the literature as relating to effectively implementing performance measurement and management systems.

Thus, the main goal of this paper is to provide an empirical analysis of the relationship between the length of time a SPMS has been implemented and its level of development and, at the same time, the relationship between the strategic performance management system’s level of development and key organizational factors.

Literature Review

A performance measurement system is the core of the overall PMS; it supports its philosophy and is fundamentally important for its effective operation (Lebas, 1995). Melnyk et al. (2014) also confirms this; he believes that measuring and managing performance is composed of two elements: a system of performance measurement and a system of performance management. On one hand, the performance measurement system incorporates the process of setting objectives; creating measures; and collecting, analysing, and interpreting performance data. On the other hand, the PMS encompasses the process for assessing the differences between actual and desired outcomes; identifying and flagging those differences that are critical, i.e., warranting management intervention; understanding if and why the deficiencies have taken place; and, when necessary, introducing (and monitoring) corrective actions aimed at closing the significant performance gaps. Thus, the PMS allows companies to plan, measure, and monitor their performance so that decisions, resources, and activities can be better coordinated with the strategies for achieving the required results (Bento & Bento, 2006). On the basis of accepting these basic tenets, only one concept of the SPMS will be used hereafter in the paper, because this concept also encompasses the system of measurement.

In order to speak about an effective SPMS, it must show specific characteristics. Different scholars have put emphasis on various characteristics that should be shown by an effective SPMS. For example, Maskell (1989) claims that traditional financial measures are inadequate and sometimes misleading; he identifies seven common characteristics of a PMS as part of world class manufacturing (WCM). A balanced picture and comprehensive mapping are among the six key characteristics identified by Kennerley & Neely (2002). Bititci et al. (2006) provide a long list of detailed characteristics of modern PMSs that differentiates between supervisory and improvement measures. Gomes et al. (2011) created a summary of relevant characteristics using the available literature on performance measurement from the last two decades.

Taking into account the considerations of the authors mentioned above and a broader review of academic literature, it is possible to integrate these opinions, remove duplication, and define a basic set of characteristics of an effective SPMS. A SPMS must:

1. Have strategic objectives and measures derived from the mission statement or vision,

2. Be established as a tool for implementing strategy and continuous improvement,

3. Set performance measure targets for what should be achieved during the projected period,

4. Support an understanding of the causal relationships between measures,

5. Have performance measures integrated across the entire hierarchy and all functions,

6. Be linked to the reward system, and

7. Change dynamically with the strategy and with changes in the internal and external environments.

The PMS does not operate in an organizational, strategic, or environmental vacuum. This means that changes in organizational structure, corporate culture, strategy, or the environment should have direct consequences for the PMS (Melnyk et al., 2014). Recently, many authors have focused on examining factors that can facilitate or hinder the effective functioning of a SPMS. On the basis of interviews with managers, Kennerley & Neely (2003) identified four key factors: the presence of a corporate culture focused on performance management, people with the required knowledge and skills, the existence of a review process for performance measures, and the availability of flexible systems. Atkinson (2012) defined the same key factors for the successful development and implementation of a PMS. According to him, the key components are visible senior management leadership and commitment, a culture of improvement and learning, and regularly reviewing and updating the PMS so that it remains dynamic and flexible. Sole (2009) distinguishes between internal and external factors influencing PMSs in public organizations. Internal ones include leadership and management’s commitment, internal resources, a performance-oriented culture, employee engagement, and the maturity of the PMS. The latter is crucial for this study because it assumes that experience in performance management and measurement will affect the system’s implementation as well as its end results. The external factors defined for public organizations are not relevant for the business environment.

Unequivocally, the most frequently mentioned factor is having a company culture focused on performance, which is mentioned by both the authors above as well as Bititci et al., 2006; Garengo & Bititci, 2007; and Franco-Santos & Bourne, 2005. Certain authors have defined the specific aspects that create it (Kennerley & Neely, 2003), while other authors separate them out. Examples of this approach are the factors of top management’s commitment and support (Johanson et al., 2006; Chan, 2004; Bourne et al., 2000; Kaplan, 2001), employee training (Chan 2004), and integration with a rewards policy (Burney et al., 2009; Johanson et al., 2006). Other factors that have been identified are organizational learning (Mohamed et al., 2009), organizational strategy and structure (Chenhall, 2003), and governance (Garengon & Bititci, 2007). Further, there are the important factors of people-primarily their engagement and participation (Cox et al., 2007), skills, and also the power to change the performance measurement system (Kennerley & Neely, 2003). The existence of a process for reviewing performance measures and the availability of a flexible IT system that allows for the collection, analysis, and reporting of data (Kennerley & Neely, 2002: 2003; Bandara, 2007) are other factors that should not be left out.

External factors influencing the effective development of a PMS are broadly identified here as factors that influence business activities and, thereby, company performance. These include new technologies, legislative changes, increasing global competition, market volatility, outsourcing, the strength of the unions, increasing customer bargaining power, and changes in accounting standards (Pedersen & Sudzina, 2012; Medori & Steeple, 2000). This paper only deals with internal factors, because it is possible for a company to manage and influence them directly.

Methodology And Research Methods

In order to fulfil the primary goal, it is first necessary to achieve the following secondary goals:

1. To determine the current SPMS’s development level for the surveyed companies,

2. To identify the key factors influencing how well this system operates and to specify the degree to which the surveyed companies manage them.

First, it was necessary to establish research questions in order to achieve the primary and secondary goals. The research questions were related to the following basic areas:

1. For what length of time has the performance measurement system been implemented in the surveyed companies?

2. What is the current strategic performance management systems’ development level-according to how well they display the characteristics of effective performance measurement and management as defined by the literature?

3. In what way are the key factors that influence how well the strategic performance management system operates managed in the surveyed companies?

4. Do companies with more experience developing a strategic performance management system have a more developed system?

5. Does a managing key factor influence the development of the strategic performance management system?

Thus defined, the research questions were developed into the form of a questionnaire. The method of an electronic questionnaire was selected for acquiring data (Somr, 2007). The basic sample was comprised of enterprises from the five most competitive sectors in the Czech Republic; these were identified on the basis of the Czech TOP 100 list of companies for 2014. The following is the breakdown of the companies contacted by individual sector in percentages: electricity, gas, steam, and air conditioning (7%); the manufacture of motor vehicles (except motorcycles), trailers, and semi-trailers (19%); the chemical, pharmaceutical, rubber, and plastic industries (37%); banking and insurance (11%); and electronics, optical products, and electrical equipment (26%).

For achieving the survey goals, two more criteria were set for selecting companies from the sectors listed above: 1. all companies actively conducting business in the Czech Republic with a turnover of CZK 30 million or more and 2. Companies having over 50 employees. Namely, medium-sized and large companies were selected, because it can be assumed that they have a developed PMS. Having been defined in this way, the population was identified using the Magnus Web database. In the end, the population included a total of 1295 enterprises.

However, 51 questionnaires were not delivered to the respondents. The overall rate of return for questionnaires was 10.1 %, i.e., 126 companies. Formulas listed in ?ermák (1980) were used to calculate sample size from the population and the subsequent rate of return.

It is possible to describe the sample of companies that participated in the questionnaire using number of employees and type of ownership. The companies were divided into the following groups by number of employees: medium-sized enterprises with 50-250 employees (50%), medium-sized to large companies with 251-500 employees (15%) and those with 501 or more employees (35%). According to type of ownership, the sample of businesses is comprised of companies with domestic ownership (53%), companies partially or completely owned by international entities (46%) and state-owned enterprises (1%). Regarding the fact that the questionnaire was filled in anonymously, it is not possible to describe the respondents by sector.

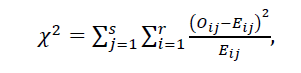

Statistical software STATISTICA was used to calculate the statistics listed below. Pearson's test of independence was used to test the hypotheses concerning the random variable’s independence. The testing criterion takes the form (Pacáková et al., 2009):

test of independence was used to test the hypotheses concerning the random variable’s independence. The testing criterion takes the form (Pacáková et al., 2009):

(1)

(1)

Where,

r and s are the number of categories of the investigated random variables, Oij are the observed frequencies and Eij denotes the theoretical frequencies.

The null hypothesis concerning independence of random variables is rejected if, for the given level of significance α, it is true that:

(2)

(2)

Where,

denotes

denotes  -quantile of probability distribution with

-quantile of probability distribution with degrees of freedom. In that case, the p-value which is provided by most of statistical software (including STATISTICA), is less than the level of significance α.

degrees of freedom. In that case, the p-value which is provided by most of statistical software (including STATISTICA), is less than the level of significance α.

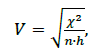

For the assessment of the level of demonstrated dependence (association), Cramer’s coefficient V was used, which is given by the term

(3)

(3)

Where,

n is the overall number of units included in the sample and h is the minimum of the numbers (r-1) and (s-1).

In cases when it made sense to judge whether the intensity of dependence for the investigated value was comparable for both directions, we used Somers’d, which is an asymmetrical measure evaluating the directional dependence of the investigated values.

Analysis And Discussion

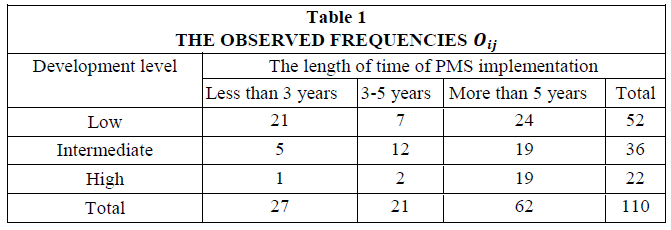

In order to verify the first hypothesis, it was necessary to first determine the length that the performance measurement system had been implemented in the companies under investigation by using a questionnaire. There were 126 returned questionnaires, of which 16 were rejected, because they did not include all the data necessary for the subsequent analysis. It was determined that 56% of the companies have a performance measurement system that has been implemented for longer than five years, 19% have had one for between three and five years, and 25% have had one for less than three years.

Next, the companies were divided according to the basic group of characteristics of an effective SPMS that were defined in the literature review section. The companies were divided into three groups that specified their SPMS’s development level. The companies whose system of performance measurement and management had 1 to 2 of the characteristics were labelled companies with “low development,” companies with 3 to 5 characteristics were designated companies with “intermediate development”, and companies that were identified with 6 to 7 characteristics were called companies with “high development”. On the basis of this division, it can be stated that 47% of the companies indicate low development, 33% of the companies show intermediate development, and a mere 20% have a highly developed SPMS.

In this context, it is possible to conduct a more detailed analysis of how the individual characteristics were distributed. The companies most frequently showed the characteristic of setting up the management system as a tool for implementing strategy (60%). On the other hand, the least shown characteristic (23%) understood of the causal relationships between the performances measures included in the SPMS. For the time being, this area has not been given enough attention in practice.

After determining how long the SPMS has been implemented and its development level, it was possible to proceed with verifying the null (H0) and alternative (HA) hypothesis that was formulated for the companies, as follows:

H0: An effective strategic performance management system’s development level is not dependent on the length of time it has been implemented.

HA: An effective strategic performance management system’s development level is dependent on the length of time it has been implemented.

For testing the null hypothesis, the companies were divided according to two criteria: the development level of an effective SPMS (low, intermediate, and high) and the length of time it has been implemented (less than three years, between three and five years, more than five years), see Table 1.

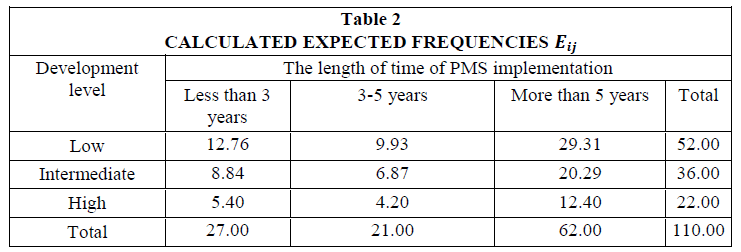

As mentioned previously, Pearson's test of independence was used to test the null hypothesis of independence. This is why expected frequencies were calculated, see Table 2.

In this case, the value of Pearson’s testing criteria, the test of independence, is X2=20,963 and the corresponding -value is nearly zero, which attests to the rejection of the null hypothesis in favor of the alternative hypothesis. We can thus state that an effective strategic performance management system’s development level is dependent on the length of time it has been implemented. Cramer’s coefficient is V=0,309, which indicates weak to medium-strong correlation.

Thus, the assumption is valid: the more experience a company has with using a SPMS, the more highly developed this system becomes, i.e., it shows more basic characteristics of an effective SPMS as defined in the professional literature.

As was mentioned in previous sections, an effective SPMS is closely dependent on factors that influence its development and continual improvement. Therefore, the level of management of these key factors was further determined for the surveyed companies. The factors that were most frequently listed in professional literature are those considered to be key, i.e., a company culture focused on performance, competent workers with the power to change the performance management system, a good process for reviewing and modifying performance measures, and a flexible information system used for collecting, analysing, and reporting data.

As has already been indicated as a part of research in the literature, a company culture focused on performance encompasses a number of aspects that shape it. In order to investigate the degree to which this factor is being managed, it was first necessary to define these aspects. The aspects were defined according to a study by Atkinson (2012) and Kennerley & Neely (2003), which agree on key points and provide a comprehensive perspective on this problem. These points are visible commitment and support by top management; the ability to learn from mistakes and adapt to a changing environment; using information attained from performance measurement for reacting quickly and revising strategy and processes; consistent communication and demonstrating the performance management system’s benefits. Companies that showed at least two of these aspects were defined as companies that manage this factor. All four aspects of company culture were managed by only 13% of the companies, three aspects were managed by 14%, two aspects were managed by 31%, and 42% of the companies managed only one of the aspects. This is thus a factor that is of considerable interest to the companies under investigation. This was the same for the factor of securing competent workers with the power to change the performance management system, which very closely relates to company culture. It was identified that 69% of the companies manage this factor. However, the most frequently managed factor is the development of a flexible information system used to collect, analyse, and report data. Of the companies, 87% were convinced that they have this type of information system.

Conversely, only 20% of the companies were able to define the process of reviewing, modifying, and implementing performance measures. While 60% of the companies did not even try to answer this question, this process cannot be considered of high quality for the remaining 20 % of the companies, because they were not able to describe its individual steps.

If we evaluate managing key factors collectively, it can be stated that all four factors are managed by only 12% of the companies, and three factors were managed by 25% of the companies. Totally only a little more than one third of the companies managed three or four factors. Most respondents manage two factors (33%) or only one factor (30%).

On the basis of determining the level of management of the key factors that influence how well the SPMS operates, it is possible to proceed with verifying the null (H0) and alternative (HA) hypothesis defined below:

H0: An effective strategic performance management system’s development level is not dependent on the number of key factors it manages.

HA: An effective strategic performance management system’s development level is dependent on the number of key factors it manages.

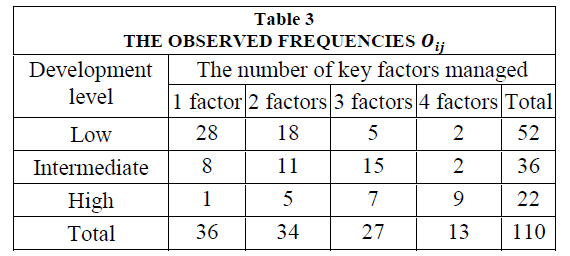

For testing the null hypothesis, the companies were divided according to two criteria: the development level of an effective SPMS (low, intermediate, and high) and the number of key factors managed (one factor, two factors, three factors, four factors), see Table 3.

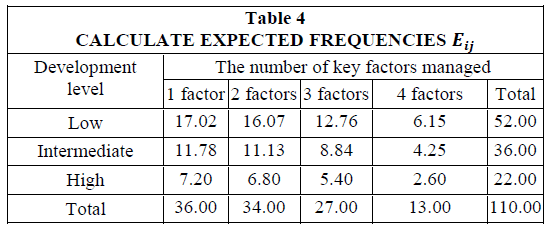

As mentioned previously, Pearson's test of independence was used to test for independence. This is why expected frequencies were calculated (Table 4).

In this case, the value of the Pearson’s testing criteria, the test of independence, is X2 = 42,357 and the corresponding -value essentially equals zero, which unequivocally attests to the rejection of the null hypothesis in favour of the alternative hypothesis. Cramer’s coefficient is V = 0,439, which indicates medium-strong correlation. Therefore, we can state that an effective strategic performance management system’s development level is dependent on the number of key factors that it manages.

In this case, it makes sense to investigate whether the intensity of the correlation for the investigated values is comparable in both directions. For this, we can use values of Somers’ . If we judge how an effective strategic performance management system’s development level is conditional on the number of key factors managed, we arrive at the value d = 0.444 If, conversely, we examine how the number of key managed factors is conditional on an effective strategic performance management system’s development level, we arrive at a higher value d = 0.510 The development level of a management system leads to a greater number of managed key factors, i.e., the more developed the system is, the greater attention the company pays to key factors.

Conclusions

In order for companies to better orient themselves in the current dynamic business environment, they need an effective SPMS based on system dynamics, sustainability, and a simulated perspective on performance (Yadav & Sagar, 2013). The design, creation, and implementation of such a system are essential for a company; naturally, the subsequent improvement of this system is no less important. This means establishing a continual process that takes care of constantly reviewing the SPMS. Unfortunately, the results show that only 20 % of the companies studied here have a highly developed SPMS. The least seen characteristic of an effective SPMS understands of the causal relationships between strategic goals or performance measures. This has been confirmed by Fukushima & Peirce (2011), who consider subjective causal relationships between objectives to be a problem for current PMSs. They consider other problems to be evolving measures, reactive decisions, costly operation, and complicated display.

It is a constant challenge for companies to continually improve SPMS and manage factors and contexts that influence how well it operates. It is necessary to focus attention on how to alter their approach from merely measurement to performance management (Amaratung & Baldry, 2002; Bittitci et al., 2012). Therefore, in this study, we decided to focus not only on specifying the current strategic performance management system’s development level but also on the degree to which these companies manage key factors (company culture, competent people, review process, and information system) that influence how well the systems operate and their constant improvement. The results showed that all four factors are managed by only 12 % of the companies, and the most neglected area is the existence and quality of the process for reviewing, modifying, and implementing performance measures. Only 20 % of the companies were able to describe it comprehensively. At the same time, the authors agree that the design and implementation of performance measures is not a one-shot effort, but it is necessary to establish a process for its constant revision (Bourne et al., 2000; Medori & Steeple, 2000; Kennerley & Neely, 2003). This process should include eliminating or replacing existing performance measures, changing target values, or changing how the measures are formulated.

On the basis of literature review, a research question was formulated as to whether companies with experience developing a SPMS have a more highly developed system. Using the pertinent statistical methods, it is confirmed that companies with a SPMS that has been implemented for a longer period of time have a more highly developed system. This finding points to the fact that experience acquired during a strategic performance management system’s development and implementation influences how effective it is. Subsequently, it is proved that companies with more developed SPMS pay more attention to managing the key factors that influence how well it operates. This result confirms the significance of these key factors for effectively developing a SPMS.

Many companies have spent considerable time and resources implementing SPMSs with different results. The current literature in the field of strategic management largely focuses on the very process of performance management and less on the context in which it takes place. SPMS does not operate in an organizational and environmental vacuum.

Unfortunately, little attention is paid to this issue. Therefore future research should focus not only on the identification of factors that affect the evolution of the SPMS, but on how to effectively manage these factors.

A crucial factor that needs to be addressed is corporate culture. It is necessary to build a corporate culture that would contribute to the continuous improvement of the entire system of strategic performance management. At the same time, it would help employees to better understand the strategic goals and link individual performance to the performance of the company as a whole. This would greatly enhance employee engagement and participation.

First of all, it is necessary to identify the specific aspects that create such a corporate culture. Then define the process of its creation and implementation. It is essential to ensure that the content of the culture is in line with the strategy and the managerial practices used throughout the management system. Only such corporate culture will contribute to the continuous improvement and learning throughout the organization.

References

- Aguinis, H., Joo, H., & Gottfredson, R. K. (2012). Performance management universals: Think globally and act locally. Business Horizons, 55(4), 385-392.

- Amaratunga, D., & Baldry, D. (2002). Moving from performance measurement to performance management. Facilities, 20(5/6), 217-223.

- Atkinson, M. (2012). Developing and using a performance management framework: a case study. Measuring Business Excellence, 16(3), 47-56.

- Bandara, W. (2007). Process modelling success factors and measures (Doctoral dissertation, Queensland University of Technology).

- Bento, A., & Bento, R. (2006). Factors affecting the outcomes of performance management systems. AMCIS 2006 Proceedings, 7.

- Bititci, U. S., Mendibil, K., Nudurupati, S., Garengo, P., & Turner, T. (2006). Dynamics of performance measurement and organisational culture. International Journal of Operations & Production Management, 26(12), 1325-1350.

- Bittitci, U. S., Garengo, P., Dorfler, V., & Nudurupati, S. (2012). Performance Measurement: Challenges for Tomorrow. International Journal of Management Reviews, 14, 305-327.

- Bourne, M., & Neely, A. (2002). 12 Why measurement initiatives succeed and fail: The impact of parent company initiatives. Business Performance Measurement, 198.

- Bourne, M., Mills, J., Wilcox, M., Neely, A., & Platts, K. (2000). Designing, implementing and updating performance measurement systems. International Journal of Operations & Production Management, 20(7), 754-771.

- Bourne, M.C.S., & Bourne, P.A. (2002). Instant Manager: Balanced Scorecard. Hodder and Stoughton, London.

- Brignall, T. J., Fitzgerald, L., Johnston, R., & Silvestro, R. (1991). Performance measurement in service businesses. Management Accounting, 69(10), 34-36.

- Burney, L. L., Henle, C. A., & Widener, S. K. (2009). A path model examining the relations among strategic performance measurement system characteristics, organizational justice, and extra-and in-role performance. Accounting, Organizations and Society, 34(3-4), 305-321.

- ?ermák, V. (1980). Selective statistical survey. SNTL.

- Chenhall, R. H. (2003). Management control systems design within its organizational context: findings from contingency-based research and directions for the future. Accounting, Organizations and Society, 28(2-3), 127-168.

- Claus, L., & Hand, M. L. (2009). Customization decisions regarding performance management systems of multinational companies: An empirical view of Eastern European firms. International Journal of Cross Cultural Management, 9(2), 237-258.

- Cox, A., Marchington, M., & Suter, J. E. (2007). Embedding the provision of information and consultation in the workplace: a longitudinal analysis of employee outcomes in 1998 and 2004.

- Forza, C., & Salvador, F. (2000). Assessing some distinctive dimensions of performance feedback information in high performing plants. International Journal of Operations & Production Management, 20(3), 359-385.

- Franco-Santos, M., & Bourne, M. (2005). An examination of the literature relating to issues affecting how companies manage through measures. Production Planning & Control, 16(2), 114-124.

- Franco-Santos, M., Kennerley, M., Micheli, P., Martinez, V., Mason, S., Marr, B., ... & Neely, A. (2007). Towards a definition of a business performance measurement system. International Journal of Operations & Production Management, 27(8), 784-801.

- Frigo, M. L., & Krumwiede, K. R. (1999). Balanced scorecards: a rising trend in strategic performance measurement. Journal of Strategic Performance Measurement, 3(1), 42-48.

- Fukushima, A., & Jeffrey Peirce, J. (2011). A hybrid performance measurement framework for optimal decisions. Measuring Business Excellence, 15(2), 32-43.

- Garengo, P., & Bititci, U. (2007). Towards a contingency approach to performance measurement: an empirical study in Scottish SMEs. International Journal of Operations & Production Management, 27(8), 802-825.

- Gomes, C. F., Yasin, M. M., & Lisboa, J. V. (2011). Performance measurement practices in manufacturing firms revisited. International Journal of Operations & Production Management, 31(1), 5-30.

- Henri, J. F. (2006). Organizational culture and performance measurement systems. Accounting, Organizations and Society, 31(1), 77-103.

- Johanson, U., Skoog, M., Backlund, A., & Almqvist, R. (2006). Balancing dilemmas of the balanced scorecard. Accounting, Auditing & Accountability Journal, 19(6), 842-857.

- Kaplan, R. S. (2001). Strategic performance measurement and management in nonprofit organizations. Nonprofit management and Leadership, 11(3), 353-370.

- Kaplan, R. S., & Norton, D. P. (1992). The balanced scorecard: Measures that drive performance. Harvard Business Review, 70(1), 71-79.

- Keegan, D. P., Eiler, R. G., & Jones, C. R. (1989). Are your performance measures obsolete?. Strategic Finance, 70(12), 45.

- Kennerley, M., & Neely, A. (2002). Performance measurement frameworks-a review. Proceedings of the 2nd International Conference on Performance Measurement, Cambridge, 291-8.

- Kennerley, M., & Neely, A. (2002). Performance measurement frameworks: a review. Business performance measurement: Theory and practice, 145-155.

- Kennerley, M., & Neely, A. (2003). Measuring performance in a changing business environment. International Journal of Operations & Production Management, 23(2), 213-229.

- Lebas, M. J. (1995). Performance measurement and performance management. International Journal of Production Economics, 41(1-3), 23-35.

- Lilian Chan, Y. C. (2004). Performance measurement and adoption of balanced scorecards: a survey of municipal governments in the USA and Canada. International Journal of Public Sector Management, 17(3), 204-221.

- Marr, B., & Schiuma, G. (2003). Business performance measurement–past, present and future. Management decision, 41(8), 680-687.

- Maskell, B. (1989). Performance measures for world class manufacturing, Management Accounting (UK), May, 1989, 32-3.

- Medori, D., & Steeple, D. (2000). A framework for auditing and enhancing performance measurement systems. International Journal of Operations & Production Management, 20(5), 520-533.

- Melnyk, S. A., Bititci, U., Platts, K., Tobias, J., & Andersen, B. (2014). Is performance measurement and management fit for the future?. Management Accounting Research, 25(2), 173-186.

- Mohamed, R., Hui, W. S., Rahman, I. K. A., & Aziz, R. A. (2009). Strategic performance measurement system design and organisational capabilities. Asia-Pacific Management Accounting Journal, 4(1), 35-63.

- Neely, A., Gregory, M., & Platts, K. (1995). Performance measurement system design: a literature review and research agenda. International Journal of Operations & Production Management, 15(4), 80-116.

- Neely, A., Kennerley, M., & Adams, C. (2007). Performance measurement frameworks: a review, 143-162. Cambridge University Press, Cambridge.

- Pacáková, V. et al. (2009). Statistical methods for economists .

- Pedersen, E.R.G., & Sudzina, F. (2012). Which firms use measures? Internal and external factors shaping the adoption of performance measurement systems in Danish firms. International Journal of Operations and Production Management, 32(1), 4-27.

- Robinson, H. S., Carrillo, P. M., Anumba, C. J., & A-Ghassani, A. M. (2005). Review and implementation of performance management models in construction engineering organizations. Construction Innovation, 5(4), 203-217.

- Seethamraju, R., & Marjanovic, O. (2009). Role of process knowledge in business process improvement methodology: a case study. Business Process Management Journal, 15(6), 920-936.

- Simons, R., Dávila, A., & Kaplan, R. S. (2000). Performance measurement & control systems for implementing strategy: text & cases. Upper Saddle River, NJ: Prentice Hall.

- Sole, F. (2009). A management model and factors driving performance in public organizations. Measuring Business Excellence, 13(4), 3-11.

- Somr, M. (2007). Basic methods of research. Selected chapters from pedagogical methodology. Available from: http://www.eamos.cz/ amos/kat_ped/externi/.../zakladni_metody_vyzkumu.doc.

- Stivers, B. P., Covin, T. J., Hall, N. G., & Smalt, S. W. (1998). How nonfinancial performance measures are used. Strategic Finance, 79(8), 44.

- Taticchi, P. (2008). Business performance measurement and management: implementation of principles in SMEs and enterprise networks (Doctoral dissertation, PhD Thesis, University of Perugia, Italy).

- Yadav, N., & Sagar, M. (2013). Performance measurement and management frameworks: Research trends of the last two decades. Business Process Management Journal, 19(6), 947-971.