Research Article: 2019 Vol: 18 Issue: 2

Effect of Forward Integration Strategy on Organizational Growth: Evidence from Selected Insurance and Banking Organizations in Nigeria

Bamidele S. Adeleke, Ladoke Akintola University of Technology

Vincent A. Onodugo, University of Nigeria

Olamide O. Akintimehin, Landmark University

Ruby I. Ike, University of Nigeria

Abstract

This study investigates the effect of forward integration strategy on the organizational growth of selected banking and insurance firms in Nigeria. The specific aim of the study is to examine the nature of the relationship between direct marketing and the firm’s profitability. The study utilized a descriptive survey design, and data were collected through a self-administered questionnaire from a sample of 753 respondents who were the staff of twelve selected banking and insurance organizations in south-western Nigeria. The hypothesis was tested with productmoment correlation coefficient at 0.05 level of significance. The finding revealed that there was a significant positive relationship between direct marketing activities and profit growth in the selected organizations. Informed by this finding, the study concluded that there were a limited number of strategic integration moves, especially vertical integration among most of the Nigerian financial organizations. The Nigerian banking and insurance organizations are therefore advised to enhance the personalization of their service to ensure that the existing customers remain locked in and new customers continue to be attracted.

Keywords

Integration Strategy, Direct Marketing, Profitability, Corporate Growth.

Introduction

In the contemporary business environment, business rivalry and keen competition has encouraged many firms to pursue different strategic moves. Bower & Lewis (2002) explain that firms globally continued to strive for enhanced competencies and improved strategic capabilities so as to remain competitive and grow profitably. Intense competition and more demand from customer expectations have facilitated suppliers, businesses and middlemen to increasingly focus on deliveries, operational sustainability, reliability, and flexibility in order to generate the needed organizational growth (Flynn & Flynn, 2004). The dynamism of the intense competition and the fragmentation of firm’s have encouraged many organizations to seek for measures that will guarantee continuous business operations. Surviving in a turbulent and highly volatile industry requires organizations to incorporate sales and profit growth as one of their major objectives. Lack of growth strategies drains the company of potential opportunities which often leads to loss of its entrepreneurial managers (Kotler & Keller, 2014). Different types of growth strategies are available to a firm, it is important that firm develops its own growth strategy according to its own characteristics and environment. Ansoff (1965), gives the three main growth strategies, among them is the integration strategy.

Integration comes in either vertical or horizontal dimensions. Perrault & McCarthy (2005) explain that vertical integration may be backward or forward. Integration strategy is backward when a firm moves toward the input of the present product and also aimed at moving lower on the production processes so that such a firm is able to supply its raw materials or components. Thomas (2010) explains that backward integration involves company’s actions in diversifying closer to the sources of raw materials, in the stages of production allowing a firm to control the dimension and quality of the supplies being purchased. Contrarily, forward integration refers to the firm entering into the business of distributing or selling the present product and moving upwards in the production/distribution process towards the consumer (Hunger & Wheelen, 2009). Forward integration happens when a organization moves closer to the end users in the of production stages, by allowing such firms more control over how the products and service are distributed and sold to the markets. Sometimes, the firm established its own distribution outlets for the sale of its own product. The other integration (i.e. horizontal integration) involves firms adding parallel new products or service to the existing product line or entering a new product market in addition to the working product line. Mugo et al. (2015) explain that it also occurs when a firm combines with rival organizations and firms.

Albeit, there is extensive literature investigation and documentation of importance of integration in achieving competitive advantage, there is however, very limited understanding of how vertical integration leads to cost efficiency in operational milieu of a developing society like Nigeria. Corporate strategic researchers have studied factors that influence inter-firm relationships from the perspective of power and relationship commitment. Some scholars were found referring to an upstream issue (supply chain) perspective, while others concentrated on a downstream (marketing channel) perspective (Fan & Goyal, 2006; Robert et al., 2012; Akben- Selcuk & Kiymaz, 2013). Generally, the trend towards organizations’ strategic integration have been explained and widely discussed by scholars and industry insiders alike and has led to repeated debates about the advantages and disadvantages of such developments. Proponents argued that the new technologies and expansion of financial firms encouraged the economies of scale and scope that gives the firm the ability to compete in the global marketplace (Shearer, 2000), whereas opponents have called the acceleration of consolidation a threat because of the effect of the homogenization of many of these institutions resulting in the loss of job, industrial standards and business liquidation (Parker, 2000; Wellstone, 2000).

Many organizations are often affected by the risks associated with growth, and this results to declining in profits leading to liquidation and folding-up of business activities, therefore compelling some of these organizations to adopt other growth strategies. However, practical experiences have shown that integrating around firms’ value networks impact the structure and operations, cost leadership, and market position of these firms. In spite of these, financial institutions in Nigeria are still very skeptical to initiate these strategic moves. The service distribution of banks and insurance firms in Nigeria are often direct, with no involvement of intermediaries. The absence of intermediaries in these firms has continued to generate complaints from the customers ranging from poor service delivery, lack of good customers relations and longer customer response-time. A cursory analysis of some of these problems prompted the crucial need for embarking on this proposed study. Thus, the need to measure the growth performance of firms’ forward integration strategy is unavoidable. So far, the existing empirical research on whether forward integration improves corporate growth remains inconclusive, because there are few studies conducted in Nigeria on the forward integration strategy (direct marketing) as it affects the financial firms’ profitability growth.

H1: There is a significant positive relationship between direct marketing and a financial firm’s profitability.

Majority of the earlier studies on vertical forward integration were conducted in Western and Asian countries, with few done in Nigeria, and these little researches were concentrated on the manufacturing firms. Those given greater emphasis in Nigerian financial sector were researches on mergers and acquisitions, which are only a part of the whole spectrum of integration strategies. The study, therefore fill up the identified gap. The economic relevance of the study to the Nigerian financial firms, coupled with the theoretical contribution to the body of strategic management knowledge makes this study a pressing research issue. Hence, the study aimed to assess the nature of the relationship between direct marketing and financial firms’ profitability.

Review Of Literature

The Concept of Forward Integration Strategy

A strategy is an action taken by an organization to attain superior performance (Hill, 2011). Strategic management involves the process by which managers choose a set of strategies for their organizations (Brassington & Pettitt, 2003; Kotler & Keller, 2014). Andrews (2000) explains that strategy is the pattern of decisions in an organization that determine and reveals the firm’s objectives, purpose and goals, produces the principal policies and plans for achieving those goals and defines the range of products and services the organization is to pursue, the kind of organization it is or intends to be and the nature of the contribution it intends to make to its constituencies. For Bats & Eldredge (2004) strategy is seen as the guiding philosophy of the organization, in the commitment of its resources to attain or fulfill its goals.

There are different definitions of strategy, both within its generic and business contexts. Although, business strategy is new, most of its principles and theories originated in military strategy, which dated back to principles propounded by Julius Caesar and Alexander the Great and further still on Sun Tzu’s classic treaties written in about 360 B.C. The scopes of strategy are usually in three and they are corporate, business and functional levels of strategy (Ezigbo, 2011). Olayinka & Aminu (2006) see corporate strategy as the process of designing, implementing and controlling the cross-functional decision-making, which ensures that the firm achieves the stated objectives. David (2001) divided strategy into four main categories which are integration strategies, intensive strategies, diversification strategies, and other strategies.

Company corporate strategies always contain growth strategies (Kotler & Amstrong, 2009). There are various growth strategic options that firm utilized according to Mugo et al. (2015). The firms have the ability to design its growth strategy according to its characteristics and environment. Ansoff (1965) gives the growth strategy options that a firm can pursue and explains that they often include the integration (horizontal and vertical-forward or backward), diversification (related and unrelated); new product development, modernization/new technology, and internationalization.

Particular Strategic Issues and Illusions in Forward Integration

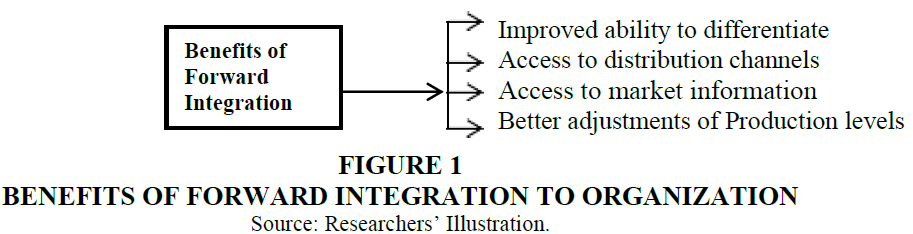

Firms can acquire or take full or partial control of its middlemen or marketing channels. This is known as forward integration (Jobber, 2006). Porter (2008) explains that there are some particular issues raised by forward integration which firms must take into consideration. First, it helps to improve the ability to differentiate the product and enables firms to access the distribution channels, thereby removing any bargaining power the channels may have. Second, it provides better access to market information by allowing the firm to determine the quantity of demand for its products sooner, than if it had to infer it indirectly from customers’ orders. Finally, it allows higher price realization to the organization.

However, Foster & Kaplan (2001) and Porter (2008) give some common misperceptions about the benefits of forward integration strategy that must be guarded against. First, a strong market position in one stage can automatically be extended to the other. This is because it is often said that the firm with a strong position in its base business can integrate into a more competitive adjacent business and extend its position to that market. Only if the integration per se produced some tangible benefits, would the integration allow the extension of market power. Second, it is always cheaper to do things internally, because so many costs and risks in integration may be avoided by dealing with outside firms rather than doing it internally. Third, it often makes sense to integrate into a competitive business, however this may not be true because there are many firms to choose from when buying or selling. Integration can produce negative incentives and blunt initiatives. Finally, integration can save a strategically sick business. Forward integration can bolster the strategic position of a business under certain conditions but it is rarely a sufficient cure for a strategically sick business. A strong position in the market cannot be extended vertically except under some extreme circumstances.

The Concept of Direct Marketing

Direct marketing has generated much attention from marketing experts, scholars and professionals, academics, and researchers in the past two decades. However, experts express three different views towards this subject. The first perspective looks upon direct marketing regarding the promotional medium (Smith, 2003; Burnertt, 2003). The second perspective looks upon it as a channel of distribution which is one of the elements of the marketing mix (Rosenbloom, 2007; Lewison & Delozier, 2002). The third view considers direct marketing as a subset of marketing (Hoke, 2002; Stone, 2004). Apart from the different perspectives employed by researchers and academics, there are also different opinions on the definition of direct marketing. For instance, there are vague attitudes toward direct selling. Some researchers (Ogilvy, 2002) treat direct selling synonymously with direct mail or telemarketing, as part of direct marketing, however others (Roman, 2007) exclude it.

Moschis et al. (2000) also argued that, according to DMA’s definition, “direct marketing does not include other forms of non-store retailing, such as door-to-door sales and vending machines.” (Moschis et al., 2000) Ogilvy, who is one of the few people to define what direct marketing is, defines direct marketing as any advertising activity which creates and exploits a direct relationship between the firm and its prospect or customer, as an individual (Ogilvy, 2002).

Although there is no general agreement on the definition, by contrasting the different definitions, the general opinions point to four features:

1. A combination of advertising and selling into a single function.

2. A service concept that will affect repeat buying.

3. A strong trend toward specificity.

4. An existence of built-in feedback mechanisms (Katzensten & Sachs, 2006).

Direct marketing helps marketers reach their target market/audiences effectively. The most desirable achievement in direct marketing is to create a significant impact on the target group and to receive a high response rate. Concerning direct marketing strategy, it is necessary to outline a direct marketing flow. Direct marketing may be applied either on its own or in conjunction with other marketing activities to satisfy customers and achieve a company's objectives. As the direct marketing response is measurable, it also eliminates some problems in marketing control and evaluation which allows marketers to monitor the marketing impacts on a target group. Thus, the strategic role of direct marketing in the marketing context relies on what it can achieve. It can expand the number of customers, maintain the existing number of customers, upgrade the existing customers, cross-sell the customer base with other firms that will have no or very little competition with the business, increase the second or future purchase (Fifield, 2002). Direct marketing is also used to achieve marketing objectives. It also emphasizes the importance of marketing research amongst the components. Direct response advertising is concerned with targeting, media choice, and the advertisement creation. Based on the response rate, companies can evaluate how successful the direct marketing campaign is and fulfill the transaction. Most importantly, it is a continuous process and involves a long-term commitment.

Does Forward Integration Strategy Facilitate Organizational Growth?

Firms can acquire or take a full or partial control of its middlemen or marketing channels. This is known as forward integration (Jobber, 2006). Empirical literature has been devoted to the examination of the causes of forward integration, in order to validate or reject the various theoretical integration strategy frameworks (Whinston, 2001). Studies have examined whether firms that must make asset-specific investments are more likely to integrate (Joskow, 2005; Baker & Hubbard, 2003). There is, however, empirical research on the actual microeconomic effects of forward integration, i.e. on how integration affects firm performance. The complexity of integration strategy, its competitive advantages and disadvantages, and its internal benefits and costs make forecasting its economic outcomes very difficult (Foster & Kaplan, 2001). Harrigan (2001) explains that vertically integrated firms outperformed their non-integrated counterparts. The superior performance of related diversifiers was due to the impact of industry structure on profit rates. In earlier studies, Hoskisson (1987) found a negative correlation between firm’s integration and performance, which was confirmed by D’Aveni & Ravenscraft’s (2004) study, where the decision to vertically integrate did not result in predictable economic performance improvements. Reed & Fronmueller (1990), however, concluded on performance neutrality in their study.

Porter (2008) explains that there are some particular issues raised by forward integration which must be adequately taken into consideration. First, forward integration improved ability to differentiate the product. Forward integration can often allow the firm to differentiate its product more successfully because the firm can control more elements of the production process or the way the product is sold. Secondly, forward integration gives access to distribution channels. Forward integration solves the problem of access to distribution channels and removes any bargaining power the channels have. Third is better access to market information. In a vertical chain, the underlying demand for the product (and the decision maker who actually makes the choices among competing brands) often are located in a forward stage. This stage determines both the size and the composition of demand of the upstream stages of production. Forward integration towards the demand leading stage can provide the firm with critical market information that allows the entire vertical chain to function more effectively (Figure 1). On the simplest level, it allows the firm to determine the quantity of demand for its products sooner than if it had to infer it indirectly from orders by its customers. The interpretation of customers' orders is complicated by the presence of inventories held by each intervening stage. The earlier market information allows better adjustment of production levels and reductions in the costs of overages and underage.

Source: Researchers’ Illustration.

Figure 1: Benefits Of Forward Integration To Organization

Theoretical Underpinnings

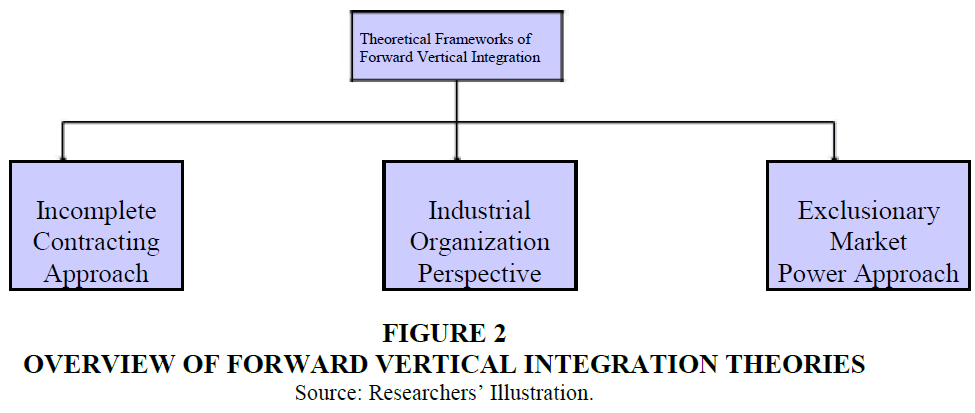

Theories of vertical integration generally analyze the ways that companies deal with different forms of market imperfections. In the vertical (forward) integration literature (Figure 2), three main approaches are generally distinguished: the incomplete contracting approach, the industrial organization theorists' perspective as put forward by Porter (1980:2008) with its resource-based view of the firm (Foster & Kaplan, 2001), and the exclusionary market power approach.

Overview Of Forward Vertical Integration Theories

Figure 2: Overview Of Forward Vertical Integration Theories

The orthodox neo-classic paradigm according to Arndt (2003), explains that the microeconomic perspective focuses on the functional role of the interacting subject with the aims of minimizing production and distribution costs. Generally, a perfect market transparency and economic rationality drives firm’s behavior, and makes it possible the maximization of long-term result, within the limits given by the level of competition in the sector. On the basis of such hypotheses, forward vertical relationships can be studied with reference to the various models of competition (perfect competition, oligopoly, monopoly, oligopsony, monopsony, etc.).

The incomplete contracting approach to vertical integration takes the view that different units of the firm are run by separate managers who are self-interested and cannot be made to act in the best interest of the firm because of the incompleteness of contracts (Klein et al., 1978; Grossman & Hart, 1996; Hart & Moore, 2000; Bolton & Whinston, 2003). The managers foresee that the part of the surplus they generate with their investment will be expropriated by the buyer in the bargaining process while they still pay the full cost of investment. Contractual incompleteness and its interaction with transactional attributes like asset specificity, complexity, and uncertainty, therefore, influences firms' decisions about governance through market-based bilateral contracts versus governance through vertical integration.

The first dimension, the incomplete contracting approach can be subdivided into two interrelated kinds of literature viz. Transaction Cost Economics (TCE) theory that is generally identified with Williamson (1985:2005). Secondly, the property rights theory that has been put forward by Oliver Hart and his co-authors (Grossman & Hart, 1996; Hart & Moore, 2000). The second approach, the industrial organization or strategic management perspective, as advocated by Porter (1980:2008), argues that vertical (forward/backward) integration can create competitive advantages in imperfect markets (Porter, 2008). In discussing different strategic motives for vertical integration, Porter (2008) argues that the strategic purpose of forward integration is to utilize different forms of economies, i.e. cost savings, like economies of combined operations, the economics of internal control and coordination, economics of information, and economies of stable relationships. Porter (2008) argues, in the same way as Pfeffer & Salancik (1978) that forward vertical integration is an important instrument for reducing uncertainty and securing controlling the channels members effectively.

The resource-based view theory of the firm has received much attention for its explanation of the existence of sustained competitive advantage (Barney, 2001; Peteraf & Barney, 2003). The resource-based view of the firm confirms the view that the decision to vertically integrate is based on creating or sustaining competitive advantage and achieving stellar growth (Miller & Shamsie, 2006; Ramanujam & Varadarajan, 2009). This study is anchored on resource-based view theory. The resource-based view of the firm provides an analysis of integration strategy that differs from the market imperfections and oligopoly assumptions of the transactions cost economics approaches and that of property rights theory explained by early scholars (Joskow, 2005). In general, the resource-and capability-based view of the firm originated from Penrose (1959) and more recently from Barney (2001). The theory emphasizes the firm’s resources as the fundamental determinant of competitive advantage and performance. The effectiveness of any change in strategy is dependent on both the environmental and organizational changes that accompany it (Rajagopalan & Spreitzer, 2007). Managerial capabilities such as an evaluation of potential costs and benefits of an integration strategy also constitute an integral determinant of forward-vertical integration success. From this perspective, the performance outcome of forward integration is a function of both firm-specific competencies and environmental constraints (Peyrefitte et al., 2002).

Conclusively, the resource-based view of a firm predicts that firms will vertically integrate into situations where integration allows the firm to either leverage its unique capabilities into another market segment or where new unique capabilities can be secured through the acquisition of a firm in another market segment. According to this theory, forward integration will also occur when it is more efficient to access or leverage knowledge or property based capabilities through integration than through market contracts (Grant, 2006).

Methodology

The study adopted a descriptive survey design. The study area was south-west Nigeria. The south-west region was selected because it has a large concentration of branches of Nigerian banking and insurance firms. 12 money deposit banks and insurance organizations were randomly selected. The population of the staff of the selected banks and insurance firms in all selected organizations was 2553, and a sample size of 753 was drawn from the study population with the method of Trek (2004) formula. The sample size defined above was selected from their respective population group with convenience sampling technique. Convenience sampling technique was used because the population groups were always tightly busy during the day or time for the survey, thereby affecting the study. Data for the study was collected from the primary source through questionnaires that were self-administered to the management staff of the selected firms. Information collected through the questionnaire was analyzed with a frequency distribution and a percentage table. The 5-point likert scale with: SA-Strongly Agree, A-Agree, U-Uncertain, D-Disagree, SD-Strongly Disagree was used to develop the answer options for the questionnaire. The test instrument was validated with face and content methods, and a Cronbach’s method of reliability was carried out on the instrument to determine the reliability. The results show a score of 0.83, which indicated that the test instrument is above the recommended reliability of 0.70, thereby indicating high reliability and validity. Seven hundred and fifty-three (753) questionnaires were administered out of which 699 (92.8%) questionnaires were returned for the data analysis. The hypothesis on the nature of the relationship between direct marketing and financial firm’s profitability was tested using the product-moment correlation coefficient analysis, and the results are as presented in table.

Results

The response from the questionnaires shows that seven hundred and fifty-three copies of questionnaires were administered to the management staff of twelve selected financial institutions. These institutions were Fidelity Bank, GT Bank, Access Bank, Diamond Bank, First Bank, Zenith Bank, United Bank, AIICO Insurance, Lead way Assurance, Royal Exchange General Assurance, Cornerstone Insurance and Niger Insurance. Six hundred and ninety-nine copies of the questionnaire were retrieved, which amounted to a 92.8% response rate. All the 699 copies of the questionnaire retrieved were found to be useable, and a total of 44 copies of the questionnaires were not retrievable, which amounted to 7.2%.

The age distribution revealed that 201 (28.8%) were respondents between ages of 18 to 24 years, 227 (32.5%) were respondents between ages of 25 to 34 years, 134 (19.2%) were respondents between ages of 35 to 44 years, 77 (11.0%) were respondents between ages of 45 to 54 years, 49 (7.0%) were respondents between ages of 55-64 years and 11 (1.5%) were respondents above 65 years. The result indicates that most of the respondents were between the ages of 25-34years representing 32.5% of the total number of respondents. However, respondents within the age bracket “above 65 years” were the minorities. This implies that most respondents in the Nigerian financial institutions are mostly between the ages of 25 to 34 years. This also shows that most of the respondents are young adults who can independently give informed responses. The distribution of gender reveals that male respondents were 336 (48.1%) and female respondents were 363 (51.9%). Despite the 3.8% difference between the two genders, data obtained represents a rich and balanced opinion of both genders.

Information provided by respondents on educational qualification programme of respondents shows that 3 (0.4%) were Ph.D. holders, 231 (33.1%) were MBA/MSc holders, 305 (43.6%) were BSc/HND holders, and 160 (22.9%) were ND/NCE holders. The degree programme results revealed that more of the respondents were BSc/HND holders (305) followed by MBA/MSc holders 231 and the least were Ph.D. holders with three respondents. However, the distribution of qualifications of respondents cuts across different disciplines, which implies that the opinions of respondents from different disciplines were considered. The distribution of marital status reveals that married respondents were 221 (31.6%) and single respondents were 374 (53.5%). 81 (11.6%) number of the respondents were separated while 23 (3.3%) were divorced. The implication of this is that most of the respondents were still unmarried.

As presented in Table 1, 255 (36.5%) respondents and 242 (34.6%) respondents strongly agreed and agreed respectively that firm’s ownership and control of its channels of distribution have impacted on its activities such as sales, customer relations, customer retaining, while 59 (8.4%) respondents and 102 (14.6%) respondents disagreed and strongly disagreed. 41 (5.9%) were undecided. Having a mean and standard deviation response score of 3.31 ± 0.77, the majority of the sampled respondents agreed that firm’s ownership and control of its channels of distribution have impacted on its activities such as sales, customer relations, and customer retaining.188 (26.8%) respondents strongly agreed that financial institutions lower their costs by directly selling to its target markets rather than through marketing channels. 199 (28.5%) respondents agreed, 72 (10.3%) respondents did not have any opinion, 85 (12.2%) respondents disagreed and 155 (22.2%) respondents strongly disagreed. With a mean and standard deviation response score of 3.04 ± 0.68, the respondents finalized that financial institutions lower their costs by directly selling to its target markets rather than through marketing channels.

| Table 1: The Nature Of The Relationship Between Direct Marketing And Firm’s Profitability | |||||||

| Items | SA (5) No. (%) |

A (4) No. (%) |

U (3) No. (%) |

D (2) No. (%) |

SD (1) No. (%) |

Mean | S.D |

| Firm’s ownership and control of its channels of distribution have impacted on its activities such as sales, customer’s relation, customer retaining. |

255 (36.5%) |

242 (34.6%) |

41 (5.9%) |

59 (8.4%) |

102 (14.6%) |

3.31 | 0.77 |

| Financial institutions lower their costs by directly selling to its target markets rather than through marketing channels. |

188 (26.8%) |

199 (28.5%) |

72 (10.3%) |

85 (12.2%) |

155 (22.2%) |

3.04 | 0.68 |

| Financial organizations ownership and control of its channels of distribution has improved its financial fortune. |

240 (34.3%) |

212 (30.3%) |

51 (7.3%) |

66 (9.5%) |

130 (18.6%) |

3.29 | 0.76 |

| Selling directly to final consumers has improved financial organizations revenue generation and profit as well. | 191 (27.3%) |

199 (28.5%) |

81 (11.6%) |

77 (11.0%) |

151 (21.6%) |

3.07 | 0.69 |

| Financial firms enjoy a decrease in total costs of servicing customers’ by cutting out the middlemen. |

199 (28.5%) |

208 (29.8%) |

108 (15.5%) |

45 (6.4%) |

139 (19.9%) |

3.18 | 0.71 |

| Marketing intermediaries are not contributing to achieving service excellence in the financial sector. | 190 (27.2%) |

191 (27.3%) |

103 (14.7%) |

95 (13.6%) |

120 (17.2%) |

3.09 | 0.70 |

| Customers? value in the financial industry is best achieve by delivering the product service without channels of distributors. | 133 (19.0%) |

233 (33.3%) |

99 (14.2%) |

99 (14.2%) |

135 (19.3%) |

3.02 | 0.66 |

| Using internet marketing to sell product-services to buyers produces time and place utilities needed by customers. |

199 (28.5%) |

235 (33.6%) |

31 (4.4%) |

79 (11.3%) |

155 (22.2%) |

3.42 | 0.79 |

Source: Researchers Computation of Field Data.

From the mean and standard deviation response score of 3.29 ± 0.76 and the responses of 240 (34.3%) respondents, 212 (30.3%) respondents, 51 (7.3%) respondents, 66 (9.5%) respondents and 130 (18.6%) respondents who strongly agreed, agreed, did not have any opinion, disagreed and strongly disagreed respectively. This shows that the respondents agreed that financial organizations’ ownership and control of its channels of distribution improved its financial fortune.

With 191 (27.3%) respondents strongly agreeing, 199 (28.5%) respondents agreeing, 81 (11.6%) respondents had no opinion, 77 (11.0%) respondents disagreeing and 151 (21.6%) respondents strongly disagreeing, as well as a mean and standard deviation response score of 3.07 ± 0.69, the respondents agreed that selling directly to final consumers has improved financial organizations’ revenue generation and profit as well.

In response to whether financial firms enjoy a decrease in total costs of servicing customers by cutting out the middlemen, 199 (28.5%) respondents strongly agreed, 208 (29.8%) respondents agreed, 108 (15.5%) respondents had no opinion, 45 (6.4%) respondents disagreed and 139 (19.9%) respondents strongly disagreed. With a mean and standard deviation response of 3.18 ± 0.71, the respondents agreed that financial firms enjoy a decrease in total costs of servicing customers by cutting out the middlemen.

In response to whether marketing intermediaries are not contributing to achieving service excellence in the financial sector, 190 (27.2%) respondents strongly agreed, 191 (27.3%) respondents agreed, 103 (14.7%) respondents had no opinion, 95 (13.6%) respondents disagreed and 120(17.2%) respondents strongly disagreed. With a mean and standard deviation response of 3.09 ± 0.70, the respondents agreed that marketing intermediaries are not contributing to achieving service excellence in the financial sector. With 133 (19.0%) respondents strongly agreeing, 233 (33.3%) respondents agreeing, 99 (14.2%) respondents had no opinion, 99 (14.2%) respondents disagreeing and 135 (19.3%) respondents strongly disagreeing as well as a mean and standard deviation response score of 3.02 ± 0.66, the respondents agreed customers? value in the financial industry is best achieved through delivery on the product service without channels of distributors.199 (28.5%) respondents strongly agreed that using internet marketing to sell product-services to buyers produces time and place utilities needed by customers. 235 (33.6%) respondents agreed, 31 (4.4%) respondents did not have any opinion, 79 (11.3%) respondents disagreed, and 155 (22.2%) respondents strongly disagreed. With a mean and standard deviation response score of 3.42 ± 0.79, the respondents agreed that using internet marketing to sell product-services to buyers produces time and place utilities needed by customers.

Data for the test of the hypothesis was obtained from responses from Table 1 above. Correlation analysis was used to test the validity of the nature of the relationship between direct marketing and financial firm’s profitability.

Table 2 reveals that while the r calculated result shows the existence of significant relationship between the variables (r=0.713 at p<0.05). The significant level is 0.041 with the degree of freedom of 698. The significance levels of the variables are less than 0.05 and the rvalue (71.3%) shows a high and very positive relationship. With a significant value of 0.041 based on the result above, it was justified that the alternative hypothesis should be accepted and the null hypothesis is rejected. Therefore, the alternate one which states that there is a significant positive relationship between direct marketing and financial firm’s profitability was accepted.

| Table 2: Correlation | |||

| Direct Marketing | Profitability | ||

| Direct Marketing | Pearson Correlation | 1 | 0.713 |

| Sig. (2-tailed) | 0.041 | ||

| N | 699 | 699 | |

| Profitability | Pearson Correlation | 0.713 | 1 |

| Sig. (2-tailed) | 0.041 | ||

| N | 699 | 699 | |

Source: Analysis of Field Data 2018.

Discussion

Findings above revealed that there was a significant positive relationship between direct marketing and financial firm’s profitability in Nigeria. The resulting findings from the descriptive statistics shows that most respondents agreed that firms ownership and control of its channels of distribution have impacted on its activities such as sales, customer relations, customer retaining. The findings from the descriptive statistics also revealed that most respondents agreed that financial institutions lower their costs by directly selling to its target markets rather than through marketing channels. The descriptive statistics also revealed that most respondents were of the opinion that financial firms enjoy a decrease in total costs of servicing customers by cutting out the middlemen. Furthermore, using internet marketing to sell productservices to buyers produces time and place utilities needed by customers. Empirical research regarding forward integration has not yet resulted in a clear-cut picture, and most of the empirical studies undertaken so far have concentrated on a comparison of the performance of integrated and non-integrated firms (Mullainathan & Scharfstein, 2001; Berger et al., 2004).

The implication of this is that direct marketing activities has a significant relationship with firms profitability. This finding is in line with the study of Dorsey & Boland (2009) and the study of Gil (2012) which showed that if a firm sells directly to users, it has full control on its costs, handling and sales revenue which are all indicators of profit. The findings also gave the nod to the work of Köhler (2014) who explained the long-run profit achievement of forward and backward integration. Conversely, Misund et al. (2012) query the impact of the direct selling on overall firm performance and explain that it is not a feasible strategy useful for large market serving firms. The result also negates the outcome of the findings of Cosh et al. (1980) who elucidate on the pitfalls of direct marketing on business servicing. Moreover, the link between direct marketing and profitability is usually eluded; hence some of the deviations in the research’s findings may be justified due to this fact.

Rumelt (1974) found that related diversification, which denotes both horizontal and vertical integration, was associated with superior performance as compared to unrelated diversification. This implies that the finding of this study is similar to the outcome of Rumelt (1974). Contrarily, the finding of this study negates the assertions from Copeland et al. (2001) and that of Shaver & Shaver (2013). Though, further researches on other industries suggests that very few companies have so far achieved in capitalizing on the benefits that come from integration and many others discovered that the transaction costs generated from increased integration were more than the financial gains generated through economies of scale and scope (Copeland et al., 2001). Financial market and performance and integration also seem negatively correlated from the study of Shaver & Shaver (2013).

Conclusion And Implications

This study concluded that there were limited numbers of integration moves especially vertical integration among most of the Nigerian financial organizations. Banks and insurance companies in Nigeria have not fully exploited the benefits of integration. This study concluded that only horizontal strategies (i.e., mergers, acquisitions, and strategic alliances) were the major strategic options exploited by these firms. Nigeria’s financial organizations have seldom initiated backward integration. It is because of the risks involved as well as the costliness. Poor awareness of the long-run benefits has also discouraged financial organizations in pursuing this strategic move. The forward integration though has been the tactics obtainable in the industry, it is necessary that the firms in the banking and insurance sector of Nigeria must develop and strengthen their value-chain operations. The validated model in this study provides a useful framework for financial firms and managers considering the possibility of using the integration strategies in achieving corporate growth. Findings from this study assist financial managers in planning and implementing their strategic plans on overall corporate growth. This study contributes to the understanding of corporate strategy and planning towards firms performances in the Nigerian context, which may be applied by industry practitioners such as banking and insurance service providers and other similar firms.

Direct marketing is a contributor to financial firms profit success. Hence, for Nigerian banking and insurance organizations to sustain their current dominant positions, competitive advantages and revenue yield, there should be an increasing personalization of services. These organizations need to customize services to such an extent that their existing customers will remain locked in and new customers continue to be attracted. This can best be achieved by utilizing direct selling, personalized marketing, and telemarketing which are all approaches of direct marketing.

Future Researches

The current study is in context of the issue under discussion in Nigeria therefore the future researchers must investigate certain relevant financial factors that have contributed in bringing increasing profitability changes in Nigeria. Further, this current study explained the effect of forward integration strategy on financial performance (profitability) of the banking and insurance firms in Nigeria. Future researchers need evaluate the impact of horizontal and backward integration strategies on the financial performance of the banking and insurance organizations in Nigeria. Moreover, it would be important if comparative analysis is done between the three integration strategies (backward, forward and horizontal integration) by future researchers in scenario of Nigeria. The current study used direct marketing as the indices of forward integration to measure the profitability expectation of banking and insurance firms in Nigeria while the future researchers could make use of disintermediation and agent bypass indices to measure the profitability performance of the financial institutions’ firms in Nigeria.

References

- Akben-Selcuk, E., & Yilmaz, A.A. (2011). The impact of mergers and acquisitions on acquirer performance: Evidence from Turkey. Business and Economics Journal, 22, 12-23.

- Andrews, K.R. (2000). The concept of corporate strategy, (2nd Edition). USA: Dow-Jones Irwin.

- Ansoff, H.I. (1965). Corporations’ strategy. New York: McGraw-Hill.

- Arndt, J. (2003). The political economy paradigm: Foundation for theory building in marketing. Journal of Marketing, 47(2), 66-84

- Baker, G.P., & Hubbard, T. (2003). Make vs. buy in trucking: Asset ownership, job design, and information. American Economic Review, 93(3), 12-22

- Barney, J. (2001). Gaining and sustaining competitive advantage. Upper Saddle USA: Prentice Hall.

- Bats, T., & Eldredge, M. (2004). Strategic management: Formulation, implementation, and control, (6th Edition). Illinois, USA: Elwin.

- Berger, A.N., Miller, N.H., Peterson, M.P., Rajan, R.G., & Stein, J.C. (2004). Does function follow organizational form? Evidence from the lending practices of large and small banks. Journal of Financial Economics, 23(3), 122-139.

- Bolton, P., & Whinston, M. (2003). Incomplete contracts, vertical integration, and supply assurance. Review of Economic Studies, 60(1), 121-148

- Boyer, K.K., & Lewis, M.W. (2002). Competitive priorities: Investigating the need for supply chain trade-offs in operations strategy. Journal of Operations Management, 11(1), 9-20.

- Brassington F., & Pettit, S. (2003). Principles of marketing, (3rd Edition). India: Prentice Hall Inc.

- Burnett, J.J. (2003), Promotion management. Boston: Houghton Mifflin.

- Carlton, D.W. (1979). Vertical integration in competitive markets under uncertainty. Journal of Industrial Economics, 27, 189-209

- Copeland, D.J., Koller, M., & Murin C.A. (2001). Corporate strategy: Resources and the scope of the firm. Boston: McGraw-Hill.

- Cosh, A., Hughes, A., & Singh, A. (1980). The determinants and effects of mergers: An international comparison. Cambridge, MA: Oelgeschlager, Gun & Hanin.

- D’Aveni, R.A., & Ravenscraft, D.J. (2004). Economies of integration vs. bureaucracy costs: Does vertical integration improve performance? The Academy of Management Journal, 37(5), 1167-1206.

- David, P. (2001). Corporate strategies for Asia pacific region. Long Range Planning Review, 28(1), 13-30.

- Dorsey, S., & Boland, M. (2009). The impact of integration strategies on food business firm value. Journal of Agricultural and Applied Economics, 41(3), 585-598

- Ezigbo, C.A. (2011). Advanced management, theory, and applications. Enugu, Immaculate Publication Limited.

- Fan, J.P.H., & Goyal, V.K. (2006). On the patterns and wealth effects of vertical mergers. Journal of Business, 79, (2), 877-902.

- Fifield, P. (2002). Marketing strategy. Oxford: Butterworth-Heinemann

- Flynn, B.B., & Flynn, E.J. (2004). An exploratory study of the nature of cumulative capabilities. Journal of Operations Management, 22(5), 439-458.

- Foster, R., & Kaplan, S. (2001). Creative destruction. New York, USA: Doubleday.

- Gil, R. (2012). Does vertical integration decrease prices? Evidence from the Paramount Antitrust Case of 1948. A Seminar and Conference Paper, Stanford Law School, Columbia Law School, University of Delaware.

- Grant, R.M. (2006). Toward a knowledge-based theory of the firm. Strategic Management Journal, 17(S2), 109-122.

- Grossman, S.J., & Hart, O.D. (1986). The costs and benefits of ownership: A theory of vertical and lateral integration. Journal of Political Economy, 94(4), 691-719.

- Harrigan, K.R. (2001). Matching vertical integration strategies to competitive conditions. Strategic Management Journal, 7(6), 535-555.

- Hart, O., & Moore, J. (2000). Property rights and the nature of the firm. Journal of Political Economy, 98(6), 1119- 1158.

- Hill, C.W.L. (2011). Global business today, (8th Edition). USA: McGraw-Hill Incorporation.

- Hoke, P. (2002). Direct marketing. Editorial.

- Hoskisson, R. (1987). Multidivisional structure and performance: The contingency of diversification strategy. Academy of Management Journal, 30(4), 625-644.

- Hunger, D.J., & Wheelen, T.L. (2009). Essentials of strategic management, (4th Edition). USA: Pearson Education.

- Jobber, D. (2006). Principles of marketing, (12th Edition). New York: Prentice Hall Inc.

- Jones, C. (1997). A general theory of network governance: Exchange conditions and social mechanisms. Academy of Management Review, 22(4), 911-945.

- Joskow, P.L. (2005). Vertical integration and long-term contracts: The case of coal burning electric generating plants. Journal of Law, Economics & Organization, 3(2), 33-81.

- Katenstein, H., & Sachs, W.S. (2006). Direct marketing. Ohio: Merril Publishing.

- Klein, B., Crawford, R.G., & Alchian, A.A. (1978). Vertical integration, appropriable rents, and the competitive contracting process. Journal of Law and Economics, 21(2), 281-296.

- Köhler, M. (2014). Bargaining in vertical relationships and suppliers’ R&D profitability. Centre for European Economic Research, 14, 087.

- Kotler, P., & Amstrong, G. (2009). Principles of marketing, (12th Edition). India: Pearson Publishers Ltd.

- Kotler, P., & Keller, K. (2014), Marketing management, (14th Edition). India: Pearson Publishers

- Lewison, D.M., & Delozier, M.W. (1982), Retailing: Principles and practice. Ohio: Bell & Howell.

- McCammon, B.C., & Little, R.W. (1965). Marketing channels, analytical systems and approaches. In Science and Marketing ed. Schwartz. New York: Wiley & Sons.

- Miller, D., & Shamsie, J. (2006). The resource-based view of the firm in two environments: The hollywood film studies in 1936 and 1965. Academy of Management Journal, 39(3), 519-543.

- Misund, B., Osmundsen, P., & Sikveland, M. (2012). Vertical integration and valuation of international oil companies. Journal of Business Management, 7(1), 23-33.

- Moschis, G.P., Korgaonkar, P.K., & Mathur, A. (2000). Older adults' responses to direct marketing methods. Journal of Direct Marketing, 4(4), 7-14.

- Mugo, M., Minja, D., & Njanja, L. (2015). The corporate growth strategies adopted by local family businesses in the manufacturing sector in Nairobi County, Kenya. European Journal of Business and Innovation Research, 3(1), 1-10.

- Mullainathan, S., & Scharfstein, D. (2001). Do firm boundaries matter? American Economic Review, 91(2), 195- 199.

- Ogilvy, D. (2002). Commonsense direct marketing. London: Drayton Bird and Kogan.

- Olayinka, K., & Aminu, S.A. (2006). Marketing management: Planning and control. Lagos, Nigeria: Sundoley Press Nigeria Limited.

- Parker, K. (2000). Diversification strategy, profit performance and the entropy measure. Strategic Management Journal, 6(1), 239-255.

- Penrose, E. (1959). The theory of the growth of the firm. Oxford: Blackwell Publishers.

- Perault, E., & McCarthy, E.J. (2005). Basic marketing: A global managerial approach, (15th Ed.). USA: McGraw- Hill Inc.

- Peteraf, M., & Barney, J.B. (2003). Unraveling the resource-based tangle. Managerial & Decision Economics, 24 (4), 309-323.

- Peyrefitte, J., Golden, P.A., & Brice J. (2002). Vertical integration and economic performance: A managerial capability framework. Journal of Management Decision, 40(3), 217-226.

- Pfeffer, J., & Salancik, G.R. (1978). The external control of organizations. New York: Harper & Row.

- Porter, M.E. (2008). Competitive strategy, (13th Edition). New York, USA: Free Press.

- Rajagopalan, N., & Spreitzer, G.M. (2007).Toward a theory of strategic change: A multi-lens perspective and integrative framework. Academy of Management Review, 22(4), 48-79.

- Ramanujam, V., & Varadarajam, P. (2009). Research on corporate diversification: A synthesis. Strategic Management Journal, 10(6), 523-551.

- Reed, R., & Fronmueller, M. (1990). Vertical integration: A comparative analysis of performance and risk. Managerial and Decision Economics, 11(3), 107-115.

- Roberts, A., Wallace, W., & Moles, P. (2012). Mergers and acquisitions. United Kingdom, Edinburg Business School.

- Roman, E. (2007). Integrated direct marketing: Techniques and strategies for success. New York: McGraw-Hill.

- Rosenbloom, B. (2007). Marketing channel: A management view, (3rd Edition). New York: The Dryden Press.

- Rumelt, R.P. (1974). Strategy, structure and economic performance. Cambridge, MA: Harvard University Press.

- Scherer, F.M. (2000). Industrial market structure and economic performance. Chicago: Rand McNally.

- Shaver, D., & Shaver, M.A. (2002). Comparing merger and acquisition activity in the U.S. and the European Union during the 1990s. Paper presented at the 5th World Media Conference, Turku, Finland.

- Smith, P.R. (2003). Marketing communication: An integrated approach. London: Kogan.

- Stone, B. (2004). Successful direct marketing methods. Chicago: Crain Books.

- Thomas, J. (2010). Diversification strategy. Retrieved from http://www.enotes.com/management- encyclopedia/diversification-strategy

- Trek J. (2004). Statistics for beginners. USA: South-Western Cengage Learning.

- Wellstone, D. (2000). A model of vertical integration and economies of scale in information product distribution. Journal of Economics, 6(3), 23-35

- Whinston, M.D. (2001). Assessing the property rights and transaction-cost theories of firm scope. American Economic Review, 91(2), 184-188.

- Williamson, O.E. (1985). The Economic institutions of capitalism: Firms, markets, relational contracting. New York, USA: Free Press

- Williamson, O.E. (2005). Outsourcing: Transaction cost economics and supply chain management. Journal of Supply Chain Management, 44(2), 5-16.