Research Article: 2018 Vol: 17 Issue: 5

The Relationship between Information Technology and Strategic Knowledge Management and their Impact on the Financial Performance of Iraqi Companies

Batool Abd Ali Ghali, University of Al Qadisiyah

Liqaa Miri Habeeb, University of Al Qadisiyah

Abstract

The research aims to determine the relationship between management information technology and strategic knowledge management in Iraqi industrial companies, as well as to identify the impact of that relationship on the financial performance of these companies. In order to achieve this objective, the research was conducted on a sample of the Iraqi industrial companies represented by (Al-Hilal Industrial Company, Baghdad Soft Drinks Company, and Iraqi Company for Carpets and Furniture) for the fiscal years (2014-2015). An analytical study was conducted to identify the Information Technology (IT) used in the administrative process and how companies manage knowledge and its impact on financial performance. A survey was conducted through distributing (100) forms to the staff of the company, and through their responses, the research objectives were achieved. As far as the model of analysis is concerned, the researchers utilized the statistical program SPSS and Likart for analyzing the responses of the study sample to the questionnaires distributed. The main findings of the research are the relationship between IT and strategic knowledge management, which is reflected in the efficiency of the financial performance of the research sample companies. IT helps to develop the administrative structure of the company in a way that increases its financial performance. The most important thing recommended by the research is the need for industrial companies to exploit the expertise and knowledge that they possess in providing administrative and strategic plans that help them achieve their future goals and avoid falling into crises and administrative problems.

Keywords

Knowledge-Based Strategy, Information-Based Strategy, Awareness of Strategic Management.

Introduction

Due to the recent rapid developments in the external business environment ,the increase competition between companies in order to obtain the available resources in order to achieve future goals, the increase financial performance in a way that strengthens its position in the markets, and the increasing dependence of many advanced organizations on modern IT in the management of administrative processes and productivity, modern information has become a key element in the continuation of administrative organizations. As a result of the decline of knowledge experiences as a basis for the consultative process in strategic decision-making in the administrative business organizations, and because of the impact of knowledge on the development of the financial performance of the organizations, the strategy of the administrative organizations is based on knowledge experience and IT in achieving strategic success in achieving future goals. The research provides an analytical and exploratory study on the relationship between management IT and strategic knowledge and their impact on the financial performance of a sample of Iraqi industrial companies. In order to achieve the objectives of the study, the researcher is divided into four parts. The first part includes the research methodology, problem, importance and objectives of research. The second part includes the theoretical framework for research, which explains the concept and importance of IT management and strategic knowledge management and their impact on the financial performance of business organizations. In the third part, the research deals with the description of the research sample that was tested, in addition to the analysis of study sample capability of IT, administrative experience and knowledge of its financial performance. Moreover, a survey was conducted through questionnaires distributed to the sample. Finally, the research ends with a number of concussions and recommendations based on the results of the practical part of the study.

Research Methodology

Research Problem

The problem of research is the lack of use of modern IT by the Iraqi industrial companies in the administration, although there is the possibility of the development of management techniques and that these companies do not manage technology knowledge appropriately in the case of possession, as that technology has a role in the development of performance financial institutions of Iraq. The research problem can be summarized as follows.

1. Is there a possibility to use IT in the management of Iraqi industrial companies?

2. Can industrial companies manage strategic knowledge management if they are available?

3. Is there a relationship between management IT and strategic knowledge in the management of future corporate plans?

4. Does the relationship between management IT and strategic knowledge management affect the financial performance of industrial companies?

Research Importance

1. It is hoped that this study helps industrial companies to use modern technology to manage knowledge and strategic information.

2. To identify the role of information technology knowledge in providing appropriate solutions to administrative problems faced by the administration.

3. Employing modern management IT in the provision of strategic plans to help the management of industrial companies in keeping up with modern administrative developments.

4. The research helps companies manage the use of modern management IT as a basis for knowing the financial performance of companies to manage companies.

Research Objectives

The research aims to achieve the following objectives:

1. Providing a theoretical framework on the concept and importance of modern IT in management.

2. Determining the importance of strategic knowledge management and its integration with modern technology in the efficient management of companies.

3. Identifying the relationship between modern information systems and strategic management in the efficiency of financial performance of Iraqi industrial companies.

Research Hypothesis

H1: Modern information technology and strategic management have an important impact on the financial performance of Iraqi industrial companies.

Population of the Study

The research population consists of Iraqi companies that possess modern IT in strategic knowledge management and operating in the Iraqi Stock Exchange (ISX).The population of the study are actually a group of various Iraqi industrial companies listed in the ISX (Al-Hilal Industrial Company, Baghdad Soft Drinks Company, and Iraqi Company for Carpets and Furniture).

Statistical Methods Used

The research relies on the measure of central tendency frequencies,, arithmetic mean ,and percentages) along with measure of dispersion, such as standard deviation in data and information analysis, in addition to using statistical program (SPSS) in order to find relationships between the research variables.

Research Limits

1. Spatial limits: Spatial limits are the sample of research represented by Iraqi industrial companies which are Al-Hilal Industrial Company, Baghdad Soft Drinks Company, and Iraqi Company for Carpets and Furniture.

2. Period limits: The research period limits are the fiscal years (2014-2015) for the above sample companies.

Theoretical Framework

Information Technology

Defining information technology

Technology is generally defined as the process of transforming the practical idea from theoretical to practical, i.e., transforming it into a productive commodity or a tool used by man in his daily life. IT means the skills possessed by man and the modern and sophisticated tools, whether audio or visual, used on daily basis (Bakshi, 2013). IT can also be defined as a useful and optimized investment for the various areas of knowledge owned by the company, i.e., it is the cognitive means that enable us to access the information quickly enough and can be used in a particular field (Nonaka et al., 2000). IT can also be defined as the revolution of information associated with the industry and the acquisition of information, marketing, storage and retrieval through modern and sophisticated equipment.

Characteristics of the information Society

As a result of the development of the administrative environment in the present day, information has become one of the familiar things of the administrative organizations. This means that the organizations which have better information than their competitors are considered to be the most capable of competitive advantage in the financial markets. Information has become an element of success and excellence, especially modern and advanced information which is useful in making appropriate decisions by the administration. Based on that, the characteristics of the information society can be defined as follows (Song, 2007):

1. Explosion of information: Contemporary societies and administrative organizations have become the source of many types of information as a result of developments and the openness of societies to IT.

2. Increasing the importance of information as a strategic resource: Information is one of the basic pillars on which management plans in organizations are based, as it is the raw material of the operations carried out by organizations of various kinds.

3. Multiple categories of beneficiaries of modern information: As a result of developments in the business environment, the need for information users to make up a large part of the requirements of individuals and administrative organizations and quickly and timely.

4. The emergence of modern IT and advanced systems: Information technology has become a leading element in many fields. Successful organizations have modern knowledge technologies that are used in successful strategic plans to achieve competitive advantage.

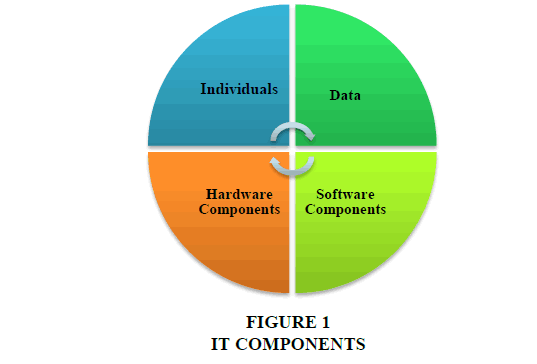

IT components

Due to the great importance of modern information based on IT that reflects the development of society, Serafica & Magno (2001) categorizes IT into the following components:

1. Hardware components: It includes all tangible components that are utilized in the use of modern technological knowledge, which can be represented in computer and it accessories such as the storage memory.

2. Software components: The intangible components that can be employed by the human to benefit from the process of generating modern knowledge and it include software and the communication between people.

3. Individuals: This component refers to the employees of administrative organizations with sufficient experience and knowledge in the generation and processing of information, as well as their ease of interaction with the latest developments in the business environment.

4. Data: This component refers to all the activities and exchanges that are stored, which are considered as a raw material to be processed in order to transfer them to valuable information.

Figure 1 below best summarizes IT components:

Figure 1: IT Components

Knowledge Management

Knowledge is one of the most recent factors of production that have been recognized as the basis for wealth creation in the economy. It is also a key source of competitive advantage. Knowledge is one of the factors of the modern economy. It expresses capital based on experience and knowledge and can be accessed through information (Maroofi et al., 2013). Innovative information is called knowledge, which offers a new addition or expansion of our previous knowledge. Through that, knowledge can be categorized into an implicit knowledge and explicit knowledge. Implicit knowledge is invented by its owners who have minds and are not expressed in other forms. This sort of knowledge is not applicable to all users. Whereas, explicit knowledge is visible and common among people and accessible to those who search for it and the means of obtaining it is multiple.

Knowledge management definition

Knowledge management is defined as planning, organizing, monitoring, coordinating and generating related knowledge and intellectual knowledge, as well as personal and organizational processes and capabilities that can be utilized to achieve competitive advantage (Wiig, 1993). According to Nonaka et al. (2000) the methodological process for the creative use and creation of knowledge. Through these definitions, the importance of knowledge management can be illustrated according to Senge et al. (2008) as follow:

1. A source of productivity: Knowledge management helps to improve the level of productivity and performance due to the distribution of skills within the institution and improve them in addition to keeping abreast of recent developments.

2. Stability factor: Working in a competitive environment is one of the most important difficulties faced by organizations. The key element that helps them in the process of excellence is knowledge management that makes them well positioned in the market.

3. Persistent competitive advantage: Knowledge is characterized by a constant competitive advantage as a rare and important resource for all organizations.

Knowledge management steps

Maroofi (2015) points out that knowledge management steps are:

1. Knowledge diagnosis: This is an important process in any knowledge management program .It simply refers to the knowledge acquisition and expertise that organizations need, especially the implicit ones.

2. Knowledge generation: innovation and the generation of new ideas. Knowledge and innovation are a dual process. Knowledge is a source of innovation, and innovation provides an addition to knowledge.

3. Knowledge storage and retention: It refers to the processes that include access to and retrieval of knowledge that is maintained. Many organizations that are exposed to crises are the result of their loss of organizational knowledge in which IT plays a prominent role in the preservation and retrieval of knowledge.

4. Knowledge sharing: It refers to sharing, dissemination and transferring of previously held knowledge including the process of connecting or transferring knowledge from the right place to the right person at the right cost.

5. Application of knowledge: It is the process of mixing knowledge in the plans and the performance of the staff of the organization through the actual use and the application in a timely manner which can be developed in a timely manner.

Strategic knowledge

Strategic knowledge is one of the most important types of organizational knowledge, which includes wisdom in the first place. It is related to planning, description, supervision, evaluation and generation of strategies. Strategic knowledge includes two types. The first type is strategic and non-strategic information, whereas the second type implies expertise, skills, the owners of the organizations, and the decision makers. Thus, strategic knowledge is perceived as something implicit or apparent that is adopted by the management of the organization so that it can accomplish the tasks of strategic planning effectively (Al Adwani et al., 2009). According to Zack (1999), the organization‘s awareness about its competitive position is not easy. Each organization develops according to its organizational structure. The organization's awareness cannot be unique or distinct, and thus can be classified as follows:

1. Fundamental knowledge: It represents the basic level of knowledge required by all organizations within a particular industry. Possessing this knowledge does not give the organization a long-term competitive advantage but enables it to enter into a particular industry.

2. Advanced Knowledge: I enable the organization to have a long-term competitive advantage. The knowledge of the organization is often different for its competitors as the organization pursues a knowledge policy in a particular way that differs from that of its competitor.

3. Innovative or pioneering knowledge: This is the knowledge that enables the organization to lead the market and lead it towards competitive excellence. Through it, the organization can change the rules of competition as it wishes.

Characteristics of knowledge as strategic resource

Al-Taei & Al-Adili (2014) assume that strategic knowledge is characterized by multiple characteristics, most importantly are:

1. Strategic knowledge is unique: Every person in the company relies on a knowledge base in interpreting the information, as the interpretation and comprehension of collective knowledge depends on the growing efforts of each person within the company's employees.

2. Scarcity: Organizational knowledge represents the knowledge that exists in the competence of employees in the current and former organization. Each organization has its own knowledge that distinguishes it from other organizations, which enables it to solve things and dilemmas.

3. Strategic knowledge is valuable: The organization’s new organizational knowledge is characterized by continuous improvement in products, processes, and services. New knowledge helps the organization to obtain new information to help it create value.

4. Strategic knowledge is non-replaceable: Collective knowledge possessed by individuals in the organization is characterized by efficient and difficult to replace, and the most important knowledge lies in capital, expertise and hard work.

Strategic management of knowledge and the awareness of strategic management

The strategic management of knowledge is represented by concentrating on the competitive reality of the organization. Whereas, the knowledge of strategic management relates to the cognitive and academic aspect of the decision maker in the organization, and can be considered in the manner in which the organization is managed. Table 1 below best illustrates the differences between the strategic management of knowledge and the awareness of strategic management.

| Table 1 Strategic Management Of Knowledge And The Awareness Of Strategic Management |

||

| Points of Difference | Strategic Management of Knowledge | Awareness of Strategic Management |

| Knowledge Type | Strategic knowledge. | Any organizational Knowledge. |

| Concentration | Knowledge included in strategy preparation and strategic decision. | Organizational knowledge of interest to any decision maker in the organization. |

| Processes | Strategic planning processes for strategic decision-making processes | Any process in the organization. |

| Relevant Parties | Strategists and strategic decision makers. | General managing managers. |

| Regulatory factors | Cognitive side, technological context, organizational culture, management style. | Leadership, culture. Technology and knowledge measurement tools. |

Knowledge-based strategy

Each organization has its own unique information, both in terms of culture and strategy. So many, researchers, including (Abosh, 2016), have presented a view on the difference between a knowledge-based strategy and information-based strategy and as shown in Table 2 below.

| Table 2 Knowledge-Based Strategy And Information-Based Strategy Comparison |

|

| Knowledge-Based Strategy | Information-Based Strategy |

| High level of personality. | Poor level of personality. |

| Increase profits by increasing efficiency. | Increasing profits by increasing efficiency. |

| Disadvantage of the feature through economies of scale. | Its advantages are through economies of scale in production. |

| Small sizes and limited customers. | Important sizes and crowded markets. |

| Investing in individuals. | Investing in technology and electronic media. |

| Consider the individual as a resource. | Consider the individual as a cost |

The Concept of Financial Performance

Financial performance is regarded as one of the most commonly used indicators of which organizations are superior to others through simple financial use and application. This may lead to a concept of performance, which is a series of financial processes and methods that can be used to determine the strength or weakness of a company. This analysis is to compare past, current and expected performance and to find out the differences between them (Al-Mutiry, 2012).

Financial performance significance

Corporate evaluation is a feedback to the effectiveness of strategic plans developed by senior management. Assessing the performance of organizations helps them in the process of future planning and monitoring the implementation of goals. Therefore, Al-Taib (2011) assumes that the financial performance significance is represented in the following points:

1. The financial performance evaluation process is one of the main pillars upon which planning, auditing and control are based.

2. Performance assessment directly helps diagnose weaknesses and strengths to solve the company's problems.

3. The financial performance provides the management of the company with the necessary information needed in the decision-making process in the areas of development and investment.

4. The financial considered as one of the most important pillars of the company in the formulation of public policy at the internal or external level.

Factors affecting financial performance assessment

The factors affecting the evaluation of the performance of the company are embodied through the following points (Shireen, 2002):

1. The different size of the company affects the process of evaluating its particular performance which deals with a larger workload.

2. The presence of late works affect production.

3. Organizational improvements that lead to production interruption.

4. Performance in similar operations varies by geographical location from unit to unit depending on local conditions.

5. The quality of the whole work unit may lead to different performance rates.

The Relationship between Information Technology and Strategic Knowledge Management

IT has been an important element in recent times, as it is the engine for the development of companies and organizations. The ownership of technology by organizations is not an evolution unless they are employed in the right direction. The process of managing IT towards achieving strategic objectives is one of the most important processes of employing modern IT. Hence, the organizations use of the skills, knowledge and advanced electronic devices they possess in the process of planning and strategic building of future plans and objectives will lead to efficiency in the implementation of these plans or goals effectively and in achieving the goals of those organizations.

Strategic Knowledge and IT Management and Its Effect on Corporate Performance

The efficiency of companies in managing the resources available to them and knowing how they outperform their competitors is based on performance in general. The performance of companies is divided into two main types: financial performance and administrative performance. The financial performance refers to the effectiveness of the company's management of the funds it owns and the extent of its employment in the best way that enables it to benefit from it for more than one area. The administrative management refers to the effectiveness of the company in implementing the administrative and strategic plans set by the senior management and how to compare them with the goals already planned in addition to the extent management ability to shape future policies. The role of knowledge and IT in influencing the financial performance of companies and organizations is evident. Organizations that have IT and effective management in their recruitment and management are the leading companies in their field that can overcome their competitors. It is also assumed that the strength of the relationship between IT and strategic knowledge management effects on the efficiency and effectiveness of financial performance of companies, which will be tested in practical part of the research.

Empirical Analysis

Description of the Research Sample

This section will describe the research sample represented by the Iraqi Company for Carpets and Furniture, Al-Hilal Industrial Company, and Baghdad Company for the manufacture of soft drinks. The reports and disclosures of the information technology used by each sample company will be prepared for the financial year 2014-2015. In addition to designing a questionnaire form consisting of (3) axes according to the search variables and will be linked using the statistical program (SPSS). Below is a brief description to the sample of the study:

Iraqi company for carpets and furniture

It is a private Iraqi joint stock company operating in the industrial sector. It was established in 1989 with a base capital of 5 million Iraqi Dinars (IQD). It was listed in the Iraqi Stock Exchange in 2004 and its capital amounted to 500 million IQD. The share of the public sector is 7.3%, the cooperative sector is 1.8%, the mixed sector is 0.2% and the private sector is 90.7% .The Company prepares and publishes lists and reports in the ISX at the end of each fiscal year.

Al-Hilal industrial company

It is a joint-stock Iraqi company operating within the industrial sector. It was established in 1962 with a capital capacity of 80 thousand IQD. It was listed in the ISX in the year (2004) with capital capacity of 150 million IQD. The company's public sector is 25% and the private sector is 74%. The company prepares and publishes lists and reports in the Iraqi Stock Exchange at the end of each financial year.

Baghdad company for the manufacture of soft drinks

It is a private joint stock company operating in the industrial sector established in 1989 with a capital capacity of 70 million IQD. It was listed in the ISX in (2004) and its capital was 10 billion IQD in 2004. The share of the public sector is 13.8%, the mixed sector is 0.78% and the private sector is 85.3%. The company prepares and publishes lists and reports in the ISX at the end of each fiscal year.

In order to identify more on the research sample, it is necessary to know more about its characteristics. Table 3 below best summarizes the characteristics of the sample of the research.

| Table 3 Distribution Of The Research Sample By Gender |

||||||

| Gender | Iraqi Company for Carpets and Furniture | Al-Hilal Industrial Company | Baghdad Company for the Manufacture of Soft Drinks | |||

| Number | Percentage | Number | Percentage | Number | Percentage | |

| Male | 40 | 40% | 53 | 53% | 55 | 55% |

| Female | 60 | 60% | 47 | 47% | 45 | 45% |

| Total | 100 | 100% | 100 | 100% | 100 | 100% |

Table 4 below illustrates the distribution of the research sample by the age.

| Table 4 Distribution Of The Research Sample By The Age |

||||||

| Baghdad Company for the Manufacture of Soft Drinks | Al-Hilal Industrial Company | Iraqi Company for Carpets and Furniture | ||||

| Categories | Number | Percentage | Number | Percentage | Number | Percentage |

| 25-30 | 25 | 25 % | 16 | 16 % | 30 | 30 % |

| 35-40 | 60 | 60 % | 50 | 50 % | 60 | 60 % |

| 40-55 | 7 | 7 % | 20 | 20 % | 5 | 5 % |

| 55-60 | 8 | 8 % | 14 | 14 % | 5 | 5 % |

| Total | 100 | 100% | 100 | 100 % | 100 | 100 % |

Table 5 below illustrates the distribution of the research sample by the scientific level.

| Table 5 Distribution Of The Research Sample By The Scientific Level |

||||||

| Iraqi Company for Carpets and Furniture | Al-Hilal Industrial Company | Baghdad Company for the Manufacture of Soft Drinks | ||||

| Scientific Level | Number | Percentage | Number | Percentage | Number | Percentage |

| Less than High School | 10 | 10% | 10 | 10% | 7 | 7% |

| High School | 15 | 15% | 25 | 25% | 3 | 3% |

| Diploma | 65 | 65% | 45 | 45% | 63 | 63% |

| Bachelors | 10 | 10% | 20 | 20% | 27 | 27% |

| Total | 100 | 100% | 100 | 100% | 100 | 100% |

Table 6 below shows the distribution of the research sample by the administrative position.

| Table 6 Distribution Of The Research Sample By The Administrative Position |

||||||

| Iraqi Company for Carpets and Furniture | Al-Hilal Industrial Company | Baghdad Company for the Manufacture of Soft Drinks | ||||

| Admin | Number | Percentage | Number | Percentage | Number | Percentage |

| Auditor | 7 | 7% | 13 | 13% | 16 | 16% |

| Chartered Auditor | 8 | 8% | 12 | 12% | 14 | 14% |

| Accountant | 9 | 9% | 8 | 8% | 7 | 7% |

| Technician | 10 | 10% | 10 | 10% | 3 | 3% |

| Laborer | 16 | 16% | 7 | 7% | 13 | 13% |

| Total | 100 | 100 % | 100 | 100 % | 100 | 100 % |

Analyzing the Research Variables

For the purpose of clarifying and analyzing the research variables, it requires analysis of each variable. IT is the first variable in the research shown in the Table 7 below.

| Table 7 Analyzing The Variables Of The Study |

||||||

| Iraqi Company for Carpets and Furniture | Al-Hilal Industrial Company | Baghdad Company for the Manufacture of Soft Drinks | ||||

| Knowledge Form | Type | Level | Type | Level | Type | Level |

| Administrative Experience | Experience | Good | Cognitive experience | Good | Accumulated Cognitive experience | Good |

| Strategic Plans | Modern plans | Good | Modern plans | Good | Modern plans | Good |

| Cognitive technology | old Plans | Not good | Modern | Good | Modern | Good |

Table 7 shows the forms of intellectual and cognitive knowledge and the strategy and IT of the research sample. Apparently, the Iraqi Company for carpets and furnishings possess better knowledge experience and strategic plans compared with Al-Hilal and Baghdad companies. The following table shows how knowledge and strategic plans are represented.

We see through Table 8 that knowledge is represented by the ideas and experiences of individuals, which promote the drawing of good strategic plans in the research sample. Information technology is represented by computers, the Internet and other modern means of communication. The definition of the form and types of knowledge in the research sample requires knowing the impact on the financial performance of the sample, as illustrate in Table 9 below.

| Table 8 Representing Technological And Strategic Knowledge In The Research Sample |

||||||

| Iraqi Company for Carpets and Furniture | Al-Hilal Industrial Company | Baghdad Company for the Manufacture of Soft Drinks | ||||

| Cognitive Form | Representation | Level | Representation | Level | Representation | Level |

| Knowledge | Individuals' ideas | Good | Individuals' ideas | Good | Experience of individuals | Very good |

| Strategy | Stability | Good | Stability | Good | the growth | Good |

| Technology | Computer hardware and communication | Not Good | Computer hardware and communication | Good | Computer hardware, communication and Internet | Good |

We note from Table 9 that the companies that have the knowledge and intellectual technology and the advanced strategy is the owner of the highest financial performance according to the analysis shown in Tables 5 & 6, as Al-Hilal Industrial Company characterized by low and weak financial performance due to the weak strategic plans followed in addition to the absence of clear vision for managing the experiences they have. In contrast to the Baghdad Company for soft drinks and the Iraqi Company for Carpets and Furniture, an increase can be remarkably seen as the return of the share per dividend distributed to the shareholders as a result of the effectiveness of the company's management in the implementation of strategic plans and the use of knowledge in the appropriate manner that serves the policy of the company.

| Table 9 Financial Performance In The Research Sample |

||||||

| Iraqi Company for Carpets and Furniture | Al-Hilal Industrial Company | Baghdad Company for the Manufacture of Soft Drinks | ||||

| Financial performance ratios | 2014 | 2015 | 2014 | 2015 | 2014 | 2015 |

| Share turnover ratio | 1.4 | 1.91 | 6.33 | 9.19 | 7.71 | 11.94 |

| Circulation Rate | 1.39 | 0.65 | 12.86 | 11.53 | 2.77 | 3.38 |

| The market value of the stock (Million) | 8291 | 4950 | 300580 | 391020 | 2125 | 2140 |

| Earnings per share | ----- | ----- | 0.148 | 0.201 | 0.325 | 0.327 |

Test the Research Hypothesis

For the purpose of testing the hypothesis of the research, a survey was conducted for the sample of the research referred to at the beginning of the subject. The questionnaire was designed by (3) axes according to the research variables, which were distributed to 100 employees whose data were analyzed by the program SPSS. Moreover, Likart scale was used for the purpose of analyzing the samples’ responses to the questionnaire and as follows:

| Table 10 Likart Scale For Analyzing The Research Samples’ Responses |

|||||

| Response Level | Strongly Agree | Agree | Neutral | Disagree | Strongly Disagree |

| Coding | 5 | 4 | 3 | 2 | 1 |

Analysis the Responses of the Research Sample

For the purpose of identifying the relationship between IT and strategic knowledge management, the questionnaire was divided into three axes, the first (IT) of which is illustrated in the following table.

Table 11 illustrates the followings:

| Table 11 Analyzing Inortmation Technology |

||||||||

| Statement | Strongly Disagree | Disagree | Neutral | Agree | Strongly Agree | Mean | SD | General Trend |

| No. | No. | No. | No. | No. | ||||

| Percentage | Percentage | Percentage | Percentage | Percentage | ||||

| IT is one of the most important developments in the Iraqi business environment | 30 | 50 | 13 | 2 | 5 | 3.1210 | 0. 62020 | Agree |

| 30% | 50% | 13% | 2% | 5% | ||||

| Modern technology provides all means for the development of organizations | 33 | 57 | 2 | 5 | 3 | 0.32 1 0 | 0. 73100 | Agree |

| 33 % | 57 % | 2 % | 5 % | 3 % | ||||

| IT is based on recent and rapid developments in the external environment | 27 | 43 | 4 | 10 | 16 | 0. 6 2 30 | 0. 6 6264 | Agree |

| 27 % | 43 % | 4 % | 10 % | 16 % | ||||

| It is not possible to take advantage of modern information unless it is employed in a good administrative manner | 35 | 35 | 12 | 9 | 9 | 0. 320 0 | 0. 698 00 | Agree |

| 35 % | 35 % | 12 % | 9 % | 9 % | ||||

| Average relative weight of the first axis | 1.09625 | Agree | ||||||

1. The research sample is consistent with the first statement, which is that “IT is one of the most important developments in the modern Iraqi business environment” through their answers (50+30%=80%) and the average arithmetic mean is (1.09625).

2. The research sample is consistent with the second statement: “Availability of modern technology means all the necessary means for the development of organizations” by answering them (33%+57%=80%) and the average arithmetic mean is (1.09625).

3. The research sample is consistent with the third statement: “IT is based on the recent developments in the external environment” by answering (27%+43%=70%) and the average arithmetic mean is (1.09625).

4. The research sample is in line with the fourth statement, which states that “It is not possible to take advantage of modern information unless it is employed in a good administrative manner...” by answering (35%+35%=70%) as a ‘agree’ in the general trend and with average arithmetic mean (1.09625).

Table 12 below best illustrates the samples responses to the second axis of the study (knowledge management strategy).

| Table 12 Analyzing The Knowledge Management Strategy |

||||||||

| Statement | Strongly Disagree | Disagree | Neutral | Agree | Strongly Agree | Mean | SD | General Trend |

| No. | No. | No. | No. | No. | ||||

| Percentage | Percentage | Percentage | Percentage | Percentage | ||||

| Strategic knowledge is one of the most important factors that the organization possesses and is a tool for growth. | 24 | 46 | 17 | 4 | 9 | 0 . 7300 | 0. 56020 | Agree |

| 24% | 46% | 17% | 4% | 9% | ||||

| Strategic knowledge provides success in organizations through advice. | 28 | 42 | 15 | 9 | 6 | 0 . 4 2 0 0 | 0. 62100 | Agree |

| 28 % | 42 % | 15 % | 9 % | 6 % | ||||

| Knowledge is the expertise of individuals and IT owned by the organization. | 31 | 49 | 8 | 7 | 5 | 0 . 6 2 00 | 0. 57 264 | Agree |

| 31 % | 49 % | 8 % | 7 % | 5 % | ||||

| The process of employing strategic knowledge is one of the most important policies of the organization towards achieving the goals. | 30 | 37 | 3 | 17 | 13 | 0 . 330 0 | 0. 4931 0 | Agree |

| 30 % | 37 % | 3 % | 17 % | 13 % | ||||

| Average relative weight of the first axis | 0.525 | Agree | ||||||

Table 12 illustrates the followings:

1. The research sample is consistent with the first statement “Strategic knowledge is one of the most important factors owned by the organization and it is a tool for growth” through their answers (24+46%=70%) and an average arithmetic mean is (0.525).

2. The research sample is consistent with the second statement “Strategic knowledge provides success in organizations through advice” by answering (28%+42%=70%) and an average arithmetic mean is (0.525).

3. The research sample is consistent with the third statement “Knowledge is the expertise of individuals and IT owned by the organization” by answering them (31%+49%=80%) and the arithmetic mean is (0.525).

4. The research sample is consistent with the fourth statement “The process of employing strategic knowledge is one of the most important policies of the organization towards achieving the goals” by answering (30%+37%=67%). And the average arithmetic mean is (0.525).

Table 13 illustrates the third axis of the study which represents the financial performance of the Iraqi companies.

| Table 13 Analyzing The Financial Performance In Iraqi Companies |

||||||||

| Statement | Strongly Disagree | Disagree | Neutral | Agree | Strongly Agree | Mean | SD | General Trend |

| No. | No. | No. | No. | No. | ||||

| Percentage | Percentage | Percentage | Percentage | Percentage | ||||

| Financial performance is one of the most important indicators for measuring the performance of a company as a whole. | 34 | 36 | 7 | 13 | 10 | 4 0 . 5500 | 0. 66020 | Agree |

| 34 % | 36 % | 7 % | 13 % | 10 % | ||||

| Trading ratios, earnings per share and market capitalization represent the most important financial performance ratios. | 32 | 48 | 8 | 8 | 4 | 4 0 0 . 530 0 |

0. 68900 |

Agree |

| 32 % | 48 % | 8 % | 8 % | 4 % | ||||

| There is a close relationship between the company's knowledge experiences and the development of its financial performance. | 33 | 46 | 11 | 7 | 3 | 4 0 . 4100 | 0. 87 264 | Agree |

| 33 % | 46 % | 11 % | 7 % | 3 % | ||||

| The process of strengthening the relationship between IT and knowledge management is an important factor in increasing financial performance. | 36 | 38 | 8 | 15 | 5 | 40 . 110 0 | .0. 99310 | Agree |

| 36 % | 38 % | 8 % | 15 % | 5 % | ||||

| The process of strengthening the relationship between IT and knowledge management is an important factor in increasing financial performance | 0.4 | Agree | ||||||

Table 13 illustrates the followings:

1. The research sample is consistent with the first statement that “Financial performance is one of the most important indicators for measuring the performance of a company as a whole” through their response (34+36%=70%) and with average athematic mean (0.4).

2. The research sample is consistent with the second statement that “Trading ratios, earnings per share and market capitalization represent the most important financial performance ratios” by their responses (32%+48%=80%) and with average athematic mean (0.4).

3. The research sample is consistent with the third statement that “There is a close relationship between the company's knowledge experiences and the development of its financial performance” by their responses (32%+48%=80%) and with average athematic mean (0.4).

4. The research sample is in line with the fourth statement that “The process of strengthening the relationship between IT and knowledge management is an important factor in increasing financial performance” by answering (36%+38%=72%) and with average athematic mean (0.4).

Results Analysis and Hypothesis Validation

Through the responses to the questionnaire statements of the first and the second axes and, it is noted that IT constitutes the basic essence in supporting strategic management in organizations, especially knowledge management. Technology and knowledge are two sides of a single coin, and with the increase of modern information based on developments in the business environment, the experience of strategic management in the management of such knowledge is increasing, It is also noticed from the responses of the research sample in the third axis that the relationship between information technology and straConclusionstegic knowledge management helps to increase the financial performance and efficiency of the organizations as indicated in Table 9. Hence, the company that possesses information technology and strategic management is competent to manage its knowledge resources is characterized by increasing financial performance through the indicators discussed in Table 13. According to what has been stated so far, the main research hypothesis “Modern information technology and strategic management have an important impact on the financial performance of Iraqi industrial companies” is approved and validated.

Conclusions And Recommendations

Conclusions

1. IT at the present time is an important component of organizations' success in achieving their strategic goals by providing timely and quick information for decision-making.

2. Iraqi industrial companies suffer from the lack of modern developments in the outside world regarding the use of information in the administrative and manufacturing process.

3. The strategic knowledge management process is the key to the development of the administrative and organizational structure of organizations in general and of Iraqi industrial companies in particular through the development of the company's infrastructure and the development of its strategic plans.

4. The relationship between IT and strategic knowledge management plays a prominent role in achieving future management objectives, resolving crises and problems as well as increasing the credibility of future prospects.

5. Financial analysis is an important indicator of the company's development in the market and its ability to achieve future success.

6. There is a great role for the relationship between IT and knowledge management in developing the financial performance of Iraqi industrial companies by providing strategic plans and solutions that enable them to achieve future success.

Recommendations

1. The need for Iraqi industrial companies to activate their IT in order to keep up with the rapid administrative developments and achieve their strategic objectives.

2. Iraqi industrial companies should employ modern information systems in the management of current and future plans for industrial development in a manner that achieves future profits.

3. Iraqi industrial companies should adopt good strategic plans that serve the interest of senior management and development of the administrative and organizational structure of the company.

4. The need for industrial companies to increase interest in the knowledge and experience which they possess in a way that helps them to predict future problems and avoid falling into them before they occur.

5. Industrial companies should take care of administrative and productive processes and develop an appropriate strategy to help them develop the financial performance.

6. The necessity of developing Iraqi industrial companies for the management expertise they possess, training and developing their skills as well as attracting more expertise for the purpose of creating a knowledge structure based on the company to increase its financial performance.

Acknowledgement

I would like to show my warm thank to Mr. Abdullah Najim Abd Al Khanaifsawy who supported me at every bit and without whom it was impossible to accomplish the end task. His translation, guidelines, and the substantial endeavors in providing the necessary sources and references have empowered me to positively finish this article.

References

- Abos h, R. (2016). The role of strategic knowledge management in enhancing the competitive response of the economic institution: A study on a sample of electronic industry institutions. Al-Gharee for Economics and Administration Sciences, 5(3), 111-140.

- Al-Adwani, A., Alaa, A., & Nujaifi, Z. (2009). The role of strategic knowledge in determining competitive development options: A study of the views of managers in Iraqi mobile organizations. Al-Qadisiyah Journal for Administrative, Economic, and Financial Studies, 257 (4), 143-170.

- Al-Taei, F. A., & Al-Adili, O. H. (2014). Knowledge management strategy and the optimal strategy for knowledge management in Iraqi University libraries: Case study of Karbala University libraries. Karbala Journal of Economic Sciences, 9(36), 154-167.

- Al-Taib, D. (2011). Information and communication technology as an introduction to knowledge management: A case study of Annaba port corporation. Faculty of Economic and Commercial Sciences Journal.

- Bakshi, S. M. H. (2013). Information technology managers role and responsibility: A study at select hospitals. Global Journal of Computer Science and Technology.

- Magno, F. A., & Serafica, R. B. (2001). Information technology for good governance. Manila: Yuchengco Center for East Asia, De La Salle University.

- Maroofi, F., Kahrarian, F., & Dehghani, M. (2013). An investigation of initial trust in mobile banking. International Journal of Academic Research in Business and Social Sciences, 3(9), 394.

- Nonaka, I., Toyama, R., & Konno, N. (2000). SECI, Ba and leadership: A unified model of dynamic knowledge creation. Long Range Planning, 33(1), 5-34.

- Senge, P. M., Smith, B., Kruschwitz, N., Laur, J., & Schley, S. (2008). The necessary revolution: How individuals and organizations are working together to create a sustainable world. Crown Business.

- Shireen, M. (2002). The development of accounting measurement of performance in the light of proxy relations. Dar Mars for publishing: Cairo.

- Song, H. (2007). The role of information and communication technologies in knowledge management: From enabler to facilitator.

- Wiig, K.M. (1993). Knowledge Management Foundations: Thinking about how people and organizations create, represent, and use knowledge.

- Zack, M. H. (1999). Developing a knowledge strategy. California management review, 41(3), 125-145.