Research Article: 2019 Vol: 18 Issue: 3

TQM Potential Moderating Role to the Relationship between HRM Practices, KM Strategies and Organizational Performance: The Case of Jordanian Banks

Zeyad Alkhazali, Al-Ahliyya Amman University

Issam Aldabbagh, Al-Ahliyya Amman University

Ayman Abu-Rumman, Al-Ahliyya Amman University

Abstract

With the ever-increasing attrition rate of organizational performance in national banks, the Jordanian banks continue to face a number of economic difficulties and imbalances in the economic structure, their results witnessed a decline in many case. This study aims to investigate the effects of Total Quality Management (TQM) on the relationship between Human Resource Management (HRM) practices and Knowledge Management (KM) strategies towards organizational performance of Jordanian banks. Result of Partial Least Squares (PLS) path analysis supports all variables in the hypothesized direct relationship with organizational performance. Relationship between HRM practices (training and development, performance appraisal and compensation) and KM strategies (knowledge acquisition, knowledge conversion, knowledge protection, knowledge application and knowledge sharing) towards organizational performance proved to be significant. Results of the analysis also suggest that TQM moderates the relationship between HRM practices and KM strategies and organizational performance; while the moderation effects of TQM on compensation, knowledge acquisition and organizational performance are not been supported. Findings of this study lend empirical, support to the view that joins value creation chains between variables, can confer competitive advantage. Thus, Jordanian national banks particularly should focus on creating a synergic combination between TQM, HRM practices and KM strategies implementation to enhance their manager’s practices towards creating sustainable effectiveness of organizational performance.

Keywords

HRM Practices, KM Strategies, TQM, Organizational Performance, Jordanian Banks.

Introduction

The part of an organization’s activities that is concerned with selecting and recruiting, training, developing and managing employees activities towards achieving organization’s objectives; is regarded as human resource management (HRM) practices (Wall & Wood, 2005; Wright & Boswell, 2002; Wood & Wall, 2002; Armstrong, 2009). Thus, HRM is concerned with employee dimensions towards realizing the objectives of an organization in a workplace (Arshad et al., 2014).

Effective HRM practices and systems focus on the organizational performance level of the business and prevent it from being lethargic (Khilji, 2001). They also emphasize that an organization’s effectiveness is proven by a strong bundle of activities and practices targeted at capitalizing on its strengths (Arshad et al., 2014). In this regard, HRM gives a better sign of support to the top management before the time of selecting and hiring suitable personnel, managing, and training them to meet up with the requirements needed to improve organizational performance.

Effective HRM practices are considered as the assurance of continuous survival and performance of the organization (Guest, 2011; Björkman & Budhwar, 2007). The varying nature of humans makes HRM practices a complex task (Bamberger & Meshoulam, 2000). Therefore, it is highly important for organizations to focus on strengthen their HRM practices and systems (Schuler & Jackson, 2005). Thus, Achieving better organizational performance requires successful, effective and efficient exploit of organization competencies and resources to create competitive advantage locally and globally.

HRM practices on selection, training and development, compensation, performance appraisal, incentives, promotion, participation, work design, communication, involvement, employment security, and so on must be formulated and implemented by HRM practices experts with the help of line managers to achieve efficiency, cooperation among employees, cooperation with management, commitment, motivation, retention, satisfaction, presence, and other organizational performance success attributes. Organizational performance is an important result that the management and shareholders will use to evaluate the business processes and organization’s activities. It is important because a perfect performance would give the shareholders and the investors’ confidence in management and thus secure a sustained and profitable organization future.

Organizations that are responsive to changes in the business environment are more able in gaining competitive advantage. Organizations usually look at knowledge management strategies as an empowering means to improving organizational performance, however the processes of knowledge creation, storage/retrieval, and transfer by itself, do not necessarily lead to that preferred enhanced organizational performance; however, effective knowledge application does (Lam et al., 2011; Brewer & Brewer, 2010; Andolšek, 2014).

Organizational performance often depends on the organization’s ability to empathize on transforming knowledge into effective use on work, and less on knowledge itself. Adopting best practices and sharing knowledge. Therefore, KM has to infuse into the way people interact in the organizations. In this regard, KM strategies and HRM practices are to be integrated as a vital theme in management and business research for the past decades due to its potential to ability and gain to sustain organizational performance (Lam et al., 2011; Brewer & Brewer, 2010; Andolšek, 2014).

In business firm, KM strategies and HRM practices integration formulates a strong and powerful tools to quantify ways business firm functions. Several examples in the literature have highlighted how the integration between KM strategies and HRM practices has enabled many organizations to achieve sustainable organizational performance (Arunprasad, 2016) and to sustain development (Gloet, 2006).

The triple dimensional attempt of testing variables in this research, aims to investigate the potential moderating role of total quality management (TQM) on the relationship between human resource management (HRM) practices and knowledge management (KM) strategies towards organizational performance of Jordanian banks. Results of such investigation could help seeking ways to create a synergic combination between TQM, HRM practices and KM strategies implementation to enhance their manager’s practices towards increasing productivity and effectiveness for sustainable organizational performance.

Scope Of The Study

This study attempts to investigate within the following scopes:

1. This study is quantitative in nature and the data were collected at one time (cross-sectional), specifically from heads of department in Jordanian banks.

2. This study makes use of the self-completion questionnaire in the collection process. Data for this study was collected from heads of department in Jordanian banks.

3. The research framework in this study is limited to identify variables: HRM practices, KM strategies, TQM and organizational performance.

Literature Review

HRM Practices and Organizational Performance

Human resource management practices are effective management of people at work. Because human resource is a potentially important source for sustainable competitive advantage, its management well helps to create unique competencies that differentiate products and services and consequently drive competitiveness. This link, in essence, facilitates a successful corporate performance. The growing body of work contains arguments that have a positive relationship between so-called “high performance work practices” and different company performance measures. “High-performance work practices” include comprehensive recruitment and selection procedures, incentive compensation and performance management systems, and extensive employee engagement and training (Racelis, 2015).

Some studies have found positive relationships between HRM practices and policies, and various company performance measures. For example, significant positive correlations have been found between the use of staff organizations in human resources and both annual profits and profit growth among cross-cutting industries. Likewise, links have been shown between high performance work practice systems and short-term measures of corporate finance performance (Racelis, 2015).

Nigam et al. (2011) examined the relationship between HRM practices and performance taking India Service Sectors as a case, they explored the three approaches in HRM practices including universalistic, contingency, and configurations remain in the Indian setting, using analytical approach. The findings show that positive relationships exist between HRM practices and its effectiveness.

Business strategies also have an influence on the relationship between HRM and its effectiveness but, HRM practices universal theory is ineffective in the case of the Indian services sector. It proposes to increase the transport and industry that allows IT to more strategic HR capabilities required. Nigam et al. concluded that HRM practices should be dynamic and contingent in the business strategy to achieve maximum impact on effectiveness performance (Nigam et al., 2011).

KM Strategies and Organizational Performance

Nawaz et al. (2014) investigated the impact of knowledge management strategies on firm performance. Data was collected from 407 manufacturing organizations and analyzed using SPSS. The research aimed to find the impact of three knowledge management strategies that are knowledge acquisition, dissemination of knowledge, and response to knowledge of innovation and firm performance. The results showed that there is a positive relationship between the variables studied and innovation partially mediates the relationship between knowledge management strategies and firm performance. The limitation of this study was that it did not consider the impact of size, and therefore there is need of a comparative study on the basis of size (Ha et al., 2016).

Knowledge Sharing cannot be limited just in sharing information. The main purpose of knowledge sharing in about its effective using that can be the core of its essential expected help to the whole organization while achieving its business goals. In this regard, Nawab’s research identifies a number of barriers causing incomplete sharing process. These barriers includes: disadvantaged knowledge of knowledge, culture and language, lack of time and place of meeting, narrow idea of productive work, status and rewards go to knowledge owners, lack of recipient absorptive capacity, knowledge-related beliefs to certain groups, and an intolerant attitude toward mistakes and shortcomings (Nawab et al., 2015).

KM procedures identified with the conversion and protection of knowledge is those that bring about to make existing learning helpful. Procedures related to knowledge conversion and protection incorporate organizational capabilities to strengthen, assimilate, join, structure, coordinate, and convey learning. Information obtained from various assets within and outside the association is ineffective if it is not converted into a gainful practicable structure. It will upgrade yield and business forms (Cho, 2011).

For Kongpichayanond, knowledge application procedures are those expected for actual utilization of learning. Not much information is in hand about consequences of learning application in the literature. It is a presumption about information application and no unequivocal confirmation. It is expected that if an association can make learning it will be connected viably (Kongpichayanond, 2013).

Learning application qualities are capacity, recovery, application, commitment, and sharing. This is the main part of information administration. The value of individual information and KM controlled by an association exists on the variable as successful as it is connected. The use of learning encourages the association to continuously change their credentials into material outcomes (Ahmad et al., 2012). Thus, the implementation of knowledge and the use of existing knowledge will forms means to make decisions (Gholami et al., 2013; Ha et al., 2016).

Total Quality Management TQM and Organizational Performance

TQM is a set of techniques and procedures for reducing or eliminating variations of production processes or service delivery systems to improve efficiency, reliability and quality to achieve organizational performance (Liu & Liu 2014). In addition, it is a management philosophy that is often adopted when working to improve quality across different cultures and industries, the key strategies used to maintain organizational performance, and how to handle an organization that will improve overall effectiveness and productivity performance towards achieving excellent status (Chao et al., 2015; Chaichi & Chaichi, 2015; Usrof & Elmorsey, 2016).

Furthermore, TQM is an effective systematic approach that helps for designing and implementing an organization’s continuous improvement process. As an approach, TQM focus on identifying problems, building commitment, and promoting open decision making among workers. In a similar vein, TQM is considered as a philosophy that aims improving the business as a whole. Some benefits lies in continuous processes and product enhancements that increases the efficiency of people and machines, that in her turn, leads to quality improvement. The main thrust of TQM is to achieve productivity and process effectiveness by identifying and eliminating problems in work processes and systems (Chao et al., 2015; Chaichi & Chaichi, 2015; Usrof & Elmorsey, 2016).

TQM has always been a priority in the agenda of some organizations due to the demand for superior quality and the enhancement of reliable products and services (Honarpour et al., 2012; Psomas & Jaca, 2016; Talib et al., 2013).

HRM practices and TQM have been recognized as a potential combination that attracts many scholars and the interests of practitioners. The integration between HRM and TQM within management philosophy supports the organization's efforts to acquire satisfied customers. Thus, this paper looks at HRM practices, KM strategies as to be subject of the investigating, while the implementation of TQM. Due that such practices, includes; recruitment and selection processes, teamwork and empowerment of employees, training and development, performance and compensation assessments have the potential to explore and generate new knowledge for the organization and responds to TQM’s requirements.

Recognizing benefits of practice during the implementation of TQM was empiracly, as Usrof & Elmorsey, proved, they believe that this approach can give a larger opportunity to achieve organization’s goals (Usrof & Elmorsey, 2016).

Other research was conducted to conceptualize the relationship between TQM and KM strategies in a new way, while some researchers consider KM strategies as the other TQM facilitator, TQM is considered as the former for KM, and the propose a reciprocal causation between TQM and KM strategies. The results of the empirical studies linked TQM to KM strategies, and the approach aims to divide the smallest correlation of the smallest and shows what part is clear about the predictor variables and what part is because of common variance among predictors. The results indicated that nearly half of all explained variances in empirical studies that considered the relationship between TQM and KM strategies is disregarding the criteria are accounted for the joint variance of TQM and KM strategies. Therefore, a reciprocal causation between TQM and KM strategies can be formulated. The research is one of the first studies that explored the diverse results of the relationship between TQM and KM strategies from a methodological perspective (Honarpour et al., 2017 & Miartana & Hadiwijoyo, 2014).

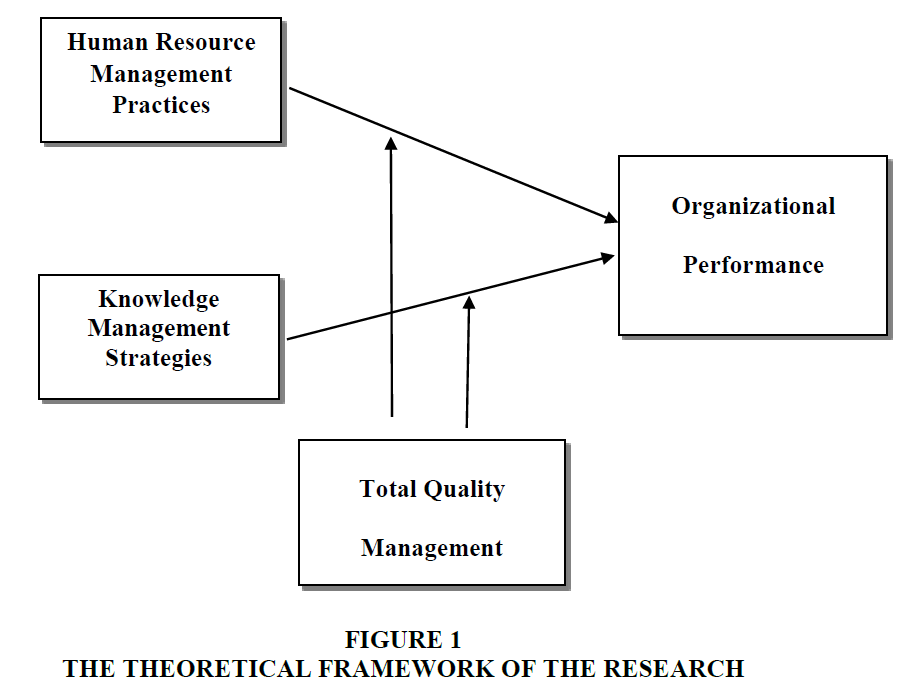

The Theoretical Model of the Study

Based on the extensive literature reviewed, the researcher identified two independent variables that are the HRM practices and KM strategies. The dependent variable of the study is organizational performance.

Further, a moderating variable has been proposed to have an effect on the relationship between independent variables and the dependent variable. Basically, the moderating variable used in this study is TQM. The relationships of these variables will all be tested according to the hypotheses of the study. Figure 1 below illustrates the schematic framework and proposed relationships that exist among the variables.

Figure 1: The Theoretical Framework Of The Research

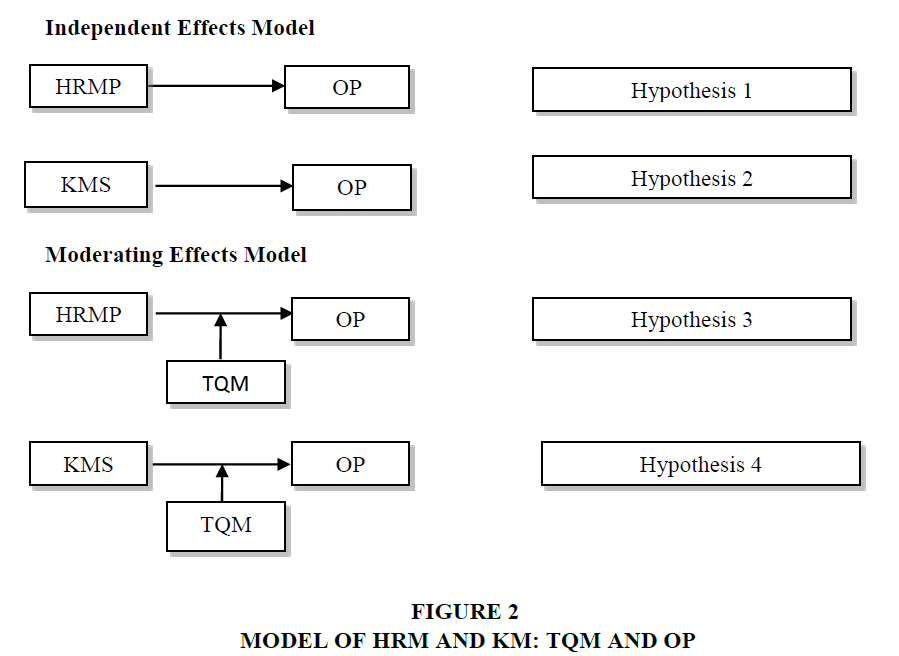

Research Hypotheses

Based on the theoretical framework of the research, four main hypotheses are formulated to reflect the relationships depicted in the framework that can be further enriched by testing alternate models. The alternative models presented here serve as examples of possible relationships and provide an explanation of the framework presented while introducing various hypotheses to be tested. These alternative models are frequently mentioned in the literature as “relationships” between HRM practices or KM strategies and organizational performance, as shown in Figure 2.

Figure 2: Model Of Hrm And Km: Tqm And Op

A few sets of hypotheses are developed based on the proposed framework. These hypotheses will establish the relationship between HRM practices and organizational performance, KM strategies towards organizational performance and at the same time, test the proposed roles of TQM on that relationship.

H1: There is a positive relationship between HRM practices and organizational performance.

H2: There is a positive relationship between KM strategies and organizational performance.

H3: TQM moderates the relationship between HRM practices and organizational performance.

H4: TQM moderates the relationship between KM strategies and organizational performance.

Research Methodology

This study uses a survey research as its quantitative approach to study. A questionnaire is a suitable data gathering instrument. Notably, each of the variables to be investigated in this study is continuous variables. These are HRM practices, KM implementation, and its subvariables, TQM as the moderating variable, and OP as the dependent variable (Zikmund et al., 2010). Also, due to the appropriateness of quantitative research data to be numeric, administering questionnaire serves as the best approach to data collection that will align with these features. This is further justified because this study is interested in capturing the opinions of employees of the Jordanian banks. It implies that the information expected to be deduced from the respondents can best be derived from the individuals’ reflection of the work place reality and its variation.

The population of this study is all the heads of department among Jordanian banks. This study is interested in capturing the opinions of all the heads of department irrespective of their role. The total number of employees from the Jordanian banks is 22886. There are 190 department heads, which is the population size for this study. Sampling is the technique used in the selection of the sample size and the subsequent administration of the survey instrument (Zikmund et al., 2010). In this study, a proportionate random sampling method is used as a method of sampling (Pallant, 2011) so as to effectively cover all the 16 banks in Jordan. This sampling method also improves the representativeness of the sample by reducing sampling error (Chang et al., 2010). Additional analyses provide an opportunity for data screening and cleaning and control for non-response data, and some other data collection errors (Krejcie & Morgan, 1970). According to Krejcie & Morgan (1970), a total of 190 questionnaires will be distributed from heads of department among Jordanian banks.

Moreover, the results that are derived from a large sample could be generalized to the whole population (Hair Jr, 2006). Sweidan mentioned that determining the appropriate sample size is an important element for a successful study because small samples may lead to inaccurate results and large samples may waste time, money, and resources (Sweidan et al., 2012). Based on this evidence, this study uses 127 as the amount of the sample size. Then, 190 questionnaires were distributed to heads of department in Jordanian banks, so that at least 127 sets can be returned in a usable form.

For this study, items addressing questions HRM practices sub-variables (training and development, performance appraisal and compensation), KM strategies sub-variables (knowledge sharing, knowledge acquisition, knowledge conversion, knowledge application and protection), TQM, and organizational performance are into parts of the questionnaire. The development of the survey instruments is guided by relevant literature, and adaptation of related past items, when suitable.

Moreover, for the purpose of this study, a uniform 5-point Likert response rating scale will be adopted to measure dependent, independent, and moderating variables. Extant authors have argued in favor of 5-point Likert scale to be consistent with the original design of Liken (1932) and measure more accurately than the 7-point scale popularly used in social science research (Dawes, 2008). Also, this method will avoid ambiguity associated with the 7-point scale, which is usually collapsed in some studies before accuracy is achieved. The scale rating is as follows: 1=Strongly Disagree, 2=Disagree, 3=Neutral, 4=Agree, 5=Strongly Agree.

Measurement of Variables

This study focuses on the relationship between HRM practices, KM strategies, and organizational performance with the inclusion of TQM as a moderating variable. Table 1 below present the summary of questionnaire.

| Table 1: Summary Of Questionnaire | |||

| Section | Variables | No. of Items | Source |

| 1 | Organizational Performance | 14 | Al-Bahussin & El-Garaihy, (2013); Argyropoulou (2013); Zerbst, (2011); Benedict, (2012); Gold et al., (2001); Kuruppu, (2009) |

| 2 | HRM practises | 22 | Vlachos (2009) & Shitsama, (2011) |

| 3 | KM strategies | 52 | Kongpichayanond, (2013) & Mohammed, (2011) & Cho, (2011) |

| 4 | TQM | 13 | Kongpichayanond, (2013); Bin Ahmad, (2014) |

Discriminant Validity

Concisely defined, discriminant validity is the extent to which a particular latent construct is different from other latent constructs (Duarte & Raposo, 2010). The current study assessed discriminant validity using AVE as suggested by Fornell & Larcker (1981). This was done by comparing the correlations among the latent constructs with square roots of AVE (Fornell & Larcker, 1981). Furthermore, discriminant validity was determined using Chin’s (1998) benchmark by comparing the indicator loadings with other reflective indicators in the cross loadings. Discriminant validity can be assessed using AVE with score more than 0.50. In addition, to show that the discriminant of validity is adequate, the square root of the AVE should be higher than the correlations of latent constructs (Fornell & Larcker, 1981).

Table 2 above shows that the square root of AVE is higher among the inter-constructs correlations in the particular columns which indicate the discriminant validity of data. All constructs have AVE above 0.5 and the square root of AVE is above the correlation for each of the construct in a particular column, which means it satisfies every condition suggested by Fornell & Lacker (1981).

| Table 2: Discriminant Validity (Fornell-Lacker Criterion) | |||||||||

| OP | TD | PA | COM | KAc | KC | KA | KP | KS | |

| OP | 0.819 | ||||||||

| TD | 0.624 | 0.754 | |||||||

| PA | 0.589 | 0.482 | 0.782 | ||||||

| COM | 0.645 | 0.505 | 0.507 | 0.761 | |||||

| KAc | 0.526 | 0.445 | 0.353 | 0.433 | 0.754 | ||||

| KC | 0.668 | 0.533 | 0.585 | 0.593 | 0.419 | 0.740 | |||

| KA | 0.632 | 0.510 | 0.489 | 0.504 | 0.617 | 0.488 | 0.770 | ||

| KP | 0.664 | 0.475 | 0.486 | 0.563 | 0.644 | 0.453 | 0.557 | 0.718 | |

| KS | 0.647 | 0.524 | 0.566 | 0.558 | 0.508 | 0.671 | 0.646 | 0.512 | 0.824 |

Coefficient of Determination (R2)

Apart from the assessment of the significance and relevance, another most commonly used measure of the evaluation of the relationships in the PLS-SEM model is the coefficient of determination or assessment of the level of R-square (Hair et al., 2010: 2012; Henseler et al., 2009). The R2 is the measure of the predictive accuracy of a model, which is calculated as the squared correlation between the endogenous construct’s actual and predicted value (Hair et al., 2014). The R2 value represents the combined effects of the exogenous latent variables on the latent endogenous variable (Hair et al., 2010: 2006: 2014). The R2 value of the endogenous variable of the direct relationships model is presented in Table 3.

| Table 3: Coefficient Of Determination (R-Square) | |

| Endogenous Variable | Coefficient of Determination (R-Square) |

| Organizational Performance | 0.702 |

Although it is difficult to provide a threshold for an acceptable level of R2 value as it largely depends on the complexity of a model and the research discipline, some researchers have stated values as a rough rule of thumb (Hair et al., 2014). Chin (1998) proposed the R2 values of 0.67, 0.33, and 0.19, to be considered as substantial, moderate, and weak respectively or rejected in the PLS-SEM modeling.

As shown in Table 3 the exogenous latent constructs of this study (i.e., HRM practices and KM strategies) explain 70% variance in organizational performance. Following Chin’s (1998) recommendation, the R2 value explained by the exogenous constructs on the endogenous construct in their direct relationships is very close to substantial effect. It indicates that organizational performance is 70% dependent on the eight predictors considered in this study. The remaining 30% may be explained by other factors.

Hypotheses Testing for Direct Relationships

In order to test hypotheses for direct relationship, the first step that was to run PLS algorithm. This step enabled the researcher to generate path coefficients to determine the relationships between exogenous and endogenous constructs of this study. The second step was bootstrapping to generate the t-value to test the significance of the relationship. There are various suggestions about how bootstrapping can be run. For instance, Hair et al. (2013) suggested that bootstrapping can be run with 500 subsample while Hair et al. (2014) recommended 5000. This study adhered to the recommendation of Hair et al. (2014) by using 5000 as mentioned above.

The results of the structural model based on the direct relationships between the predictors and criterion variables of this study are presented in Table 4 below. These results were interpreted using the coefficients (Beta) of the path relationship, the standard error (SE), t-value (T Statistics) and P-value.

| Table 4: Structural Model Output For Hypotheses Testing | ||||||

| Hypotheses | Hypothesized Relationships | Path Coefficient | Standard error | T statistics | P Value | Comments |

| H1 | - | - | - | - | - | - |

| H1a | TD à OP | 0.186 | 0.051 | 3.558 | 0.000 | Accepted |

| H1b | PA à OP | 0.194 | 0.049 | 3.583 | 0.000 | Accepted |

| H1c | COM à OP | 0.185 | 0.052 | 3.539 | 0.000 | Accepted |

| H2 | - | - | - | - | - | - |

| H2a | KAc à OP | 0.135 | 0.061 | 2.191 | 0.001 | Accepted |

| H2b | KC à OP | 0.176 | 0.074 | 2.429 | 0.000 | Accepted |

| H2c | KA à OP | 0.334 | 0.063 | 5.303 | 0.000 | Accepted |

| H2d | KP à OP | 0.255 | 0.065 | 3.887 | 0.000 | Accepted |

| H2e | KS à OP | 0.128 | 0.075 | 2.149 | 0.001 | Accepted |

Hypotheses Testing for Moderating Effect

In this study, moderating effect of TQM was tested in the relationship between HRM practices, KM strategies and organizational performance. The following Table 5 shows the findings of moderating effect test.

| Table 5: Results Of Moderating Effect Test | ||||||

| Hypotheses | Relationship | Coefficients | T-Value | P-Value | Level of Sig. | Comments |

| H3 | - | - | - | - | - | - |

| H3a | TQM* TD ->OP | 0.111 | 3.448 | 0.001 | *** | Accepted |

| H3b | TQM* PA ->OP | 0.067 | 2.227 | 0.026 | ** | Accepted |

| H3c | TQM* COM ->OP | 0.280 | 0.869 | 0.385 | - | Rejected |

| H4 | - | - | - | - | - | … |

| H4a | TQM* KAc ->OP | 0.035 | 1.301 | 0.193 | - | Rejected |

| H4b | TQM* KC ->OP | 0.133 | 4.879 | 0.000 | *** | Accepted |

| H4c | TQM* KA ->OP | 0.078 | 2.875 | 0.004 | *** | Accepted |

| H4d | TQM* KP ->OP | 0.097 | 3.591 | 0.000 | *** | Accepted |

| H4e | TQM* KS ->OP | 0.079 | 3.218 | 0.001 | *** | Accepted |

Note: ***p=0.01; **p=0.05; *p=0.1

The above Table 5 shows the hypotheses testing results of moderating effects of TQM in the relationship between HRM practices, KM strategies and organizational performance. In PLSSEM analysis, moderating effect exists if the interaction path is significant which means that the t-statistics of interaction effect must be 1.64 or 1.96 and above to be significant using one tail or two tails respectively (Hair et al., 2010).

Results And Discussion

Findings of the present study are discussed in the context of research questions, research objectives, hypothesized relationships, theoretical framework and underpinning theories. The subheadings in this section are structured according to the research objectives.

The Relationship between HRM Practices and Organizational Performance

HRM practices as relationship management success factors positively influence organizational performance among heads of departments in Jordanian banks, as proposed in hypothesis H1 (H1a, H1b, and H1c). The result of this relationship as reported in Table 4, is at the 0.001 level of significance, with oath coefficient (training and development is 0.184, performance appraisal is 0.034 and compensation is 0.185), T-statistics and P-value (training and development is t=3.558 (P<0.000), performance appraisal is t=3.583 (P<0.000) and compensation is t=3.539 (P<0.000)). This result indicates that HRM practices are considered as the most important determinant of organizational performance. These results are in line with previous studies (Dyer & Reeves, 1995; Harel et al., 2003; Chand & Katou, 2007; Katou & Budhwar, 2015; Vlachos, 2009; Gurbuz & Mert, 2011; Nigam et al., 2011; Maruf & Raheem, 2014; Almazari, 2014).

The Relationship between KM Strategies and Organizational Performance

The relationship between KM strategies and organizational performance, this variable positively influences organizational performance among heads of department in Jordanian banks as proposed in hypothesis H2 (H2a, H2b, H2c, H2d and H2e). As expected, the result supports the relationship as reported in Table 4, at the 0.001 level of significance, path coefficient is: (knowledge acquisition is 0.135, knowledge conversion is 0.176, knowledge protection is 0.255, knowledge application is 0.334 and knowledge sharing is 0.128), T-statistics and P-value are: (knowledge acquisition is t=2.191 (P<0.001), knowledge conversion is t=2.429 (P<0.000), knowledge protection is t=3.887 (P<0.000), knowledge application is t=5.303 (P<0.000) and knowledge sharing is t=2.149 (P<0.001)). This result indicates that KM strategies among Jordanian banks need to be considered to improve the level organizational performance among heads of department.

In summary, the tests performed show a statistically positive and significant relationship between KM strategies and organizational performance. This finding agrees with prior researches that have shown a positive relationship between KM strategies and organizational performance (Rasula et al., 2012; Maseki, 2012; Imran, 2014; Supriyanto, 2015).

The effects of HRM Practices on Organizational Performance are Influenced by the TQM of Jordanian Banks

The effects with regards to the moderating effect of TQM on the relationship between HRM practices and organizational performance, are as stated in hypothesis H3 (H3a, H3b and H3c). The results support this hypothesis (H3a and H3b) as shown in Table 5, at the 0.001 level of significance (training and development is Coef=0.111, t=3.448 (p>0.001), performance appraisal is Coef=0.067, t=2.227 (p>0.026) and compensation is Coef=0.280, t=0.869 (p>0.385)).

These findings indicate that moderating effects of TQM on the relationship between HRM practices and organizational performance are significant and in line with previous studies (Abu- Doleh 2012; Keeble & Armitage, 2010). But according to Hair et al. (2010), H3c both the tstatistics and p-value were insignificant. Therefore hypothesis H3c which posits that TQM moderates the relationship between compensation and organizational performance is not accepted.

The effects of KM Strategies on Organizational Performance are Influenced by the TQM of Jordanian Banks

The moderating effects of TQM on the relationship between KM strategies and organizational performance are as stated in hypothesis H4 (H4a, H4b, H4c, H4d and H4e). The result of this hypothesis supports (H4b, H4c, H4d and H4e) the moderation effect as reported in Table 5, at the 0.001 level of significance (knowledge acquisition is Coef=0.035, t=1.301, (p<0.193), knowledge conversion is Coef=0.133, t=4.879, (p<0.000), knowledge application is Coef=0.078, t=2.875, (p<0.004), knowledge protection is Coef=3.591, t=3.591, (p<0.000) and knowledge sharing is Coef=3.218, t=3.218, (p<0.001)). These findings indicate that the moderating effects of TQM on the relationship between KM strategies (knowledge conversion, knowledge application, knowledge protection and knowledge sharing) and organizational performance is proved (Loke et al., 2011; Aboyassin et al., 2011; Dabestani et al., 2014). But hypothesis H4a is rejected because it is insignificant. On the basis of this finding, it can be said that TQM doesn’t moderate the relationship between knowledge acquisition and organizational performance. Therefore hypothesis H4a is rejected (Hair et al., 2010).

The present study demonstrates that it would be in the best interest of national sampled banks in particular, to apply relationship management approach in the delivery of their banks’ services in view of the employee performance challenges facing the sector. By using specific HRM practices (training and development, performance appraisal and compensation). KM strategies (knowledge acquisition, knowledge application, knowledge conviction, knowledge protection and knowledge sharing) and TQM, employees’ participation at all levels of the banking sector can be increased. This will promote a sense of belonging or recognition, which ultimately will lead to improve performance.

Taken the comprehensive results of the present study succeeded in answering all the research questions and fulfilled the objectives, regarding some limitations. While several studies abound on the link between the relationship of HRM practices, KM strategies and organizational performance, the present study, addresses theoretical gaps by testing the relative impact of personal reasons which hitherto have been rarely investigated. It also incorporates the significance of the moderating role of TQM and expanding the theoretical horizons of the RBV theory and the knowledge based theory within the context of the banking sector. The study has succeeded in evaluating the moderating role of TQM in the relationship between HRM practices (training and development, performance appraisal, and compensation), KM strategies (knowledge acquisition, knowledge application, knowledge conviction, knowledge protection and knowledge sharing) and organizational performance among Jordanian banks.

Apart from theoretical contributions, the findings of this study provide important managerial implications, particularly for the banking sector. In response to the limitations of this study, several suggestions for future research are made with a view to filling the gaps in the present research. In conclusion, the present study provides valuable theoretical and practical contribution to expand the body of knowledge in the domain of organizational performance, in particular. Though the focus of the study is on banks’ performance, implementation of the findings of this study can help the national banks in Jordan to increase the employee’s performance.

Conclusion

The study highlights the complexity of management task and recommends that Jordan assumes a TQM perspective. Resources can be provided by lecturers, employees and banks which require an interactive approach through which the parties integrate these resources. Jordan stands to gain if the recommendations are implemented to become capable of attaining its vision in the future.

For future studies may be based on the following ideas: further enlarging the study population involving the whole banking sector. Alternatively, by taking evidence from other industries and increasing the number of observations by using a larger sample size and longer period for data. The relationship between HRM practices, KM strategies and organizational performance can also be further explained, if future researchers conduct studies by including additional variables in order to cover other dimensions of TQM in terms of banking perception and operations. Changing TQM from moderating to independent variable or even to a mediating variable may also change the results and relationships. Since national banks are still growing in Jordan, performance evaluation must be conducted from time to time, in order to take any corrective actions, when needed.

References

- Aboyassin, N.A., Alnsour, M., & Alkloub, M. (2011). Achieving total quality management using knowledge management practices: A field study at the Jordanian insurance sector. International Journal of Commerce & Management, 21, 394-409.

- Abu-Doleh, J.D. (2012). Human resource management and total quality management linkage-rhetoric and reality: Evidence from an empirical study. International Journal of Commerce and Management, 22(3), 219-234.

- Ahmad, S., Fiaz, M., & Shoaib, M. (2012). Impact of Knowledge Management Practices on Organizational Performance: An Evidence from Pakistan. International Journal of Scientific and Engineering Research , 3(8), 10-15.

- Almazari, A.A. (2014). The impact of affective human resources management practices on the financial performance of the Saudi Banks. Integrative Business & Economics, 3(1), 327-336.

- Andolšek, D.M. (2014). Knowledge management and human resource management: A strategic perspective. Journal of Process Management, 2(4), 93-101.

- Armstrong, M. (2009). The practice of human resource management. St. Petersburg: Peter.

- Arshad, A., Azhar, S.M., & Khawaja, K.J. (2014). Dynamics of HRM practices and organizational performance?: Quest for strategic effectiveness in Pakistani organizations. International Journal of Business and Social Science, 5(9), 93-101.

- Arunprasad, P. (2016). Guiding metaphors for knowledge intensive firms: Strategic HRM practices and knowledge strategies. International Journal of Organizational Analysis, 24(4), 743-772

- Bamberger, P., & Meshoulam, I. (2000). Human resource management strategy. Published Sage, London, 99.

- Björkman, I., & Budhwar, P. (2007). When in Rome…? Human resource management and the performance of foreign firms operating in India. Employee Relations, 29(6), 595-610.

- Brewer, P.D., & Brewer, K.L. (2010). Knowledge management, human resource management, and higher education: a theoretical model. Journal of Education for Business, 85(6), 330-335.

- Chaichi, A., & Chaichi, K. (2015). The impact of human resource deliberating TQM practice and employees job satisfaction in Iran. International Journal of Multicultural and Multireligious Understanding, 2(3), 27-38.

- Chand, M., & Katou, A.A. (2007). The impact of HRM practices on organizational performance in the Indian hotel industry. Employee Relations, 29(6), 576-594.

- Chang, S.J., Van Witteloostuijn, A., & Eden, L. (2010). From the editors: Common method variance in international business research. Journal of International Business Studies, 41(2), 178-184.

- Chao, C.Y., Hsu, H.M., Hung, F.C., Lin, K.H., & Liou, J.W. (2015). Total quality management and human resources selection: A case study of the national teacher selection in Taiwan. Total Quality Management & Business Excellence, 26(1-2), 157-172.

- Chin, W.W. (1998). The partial least squares approach to structural equation modeling. Modern Methods for Business Research, 295(2), 295-336.

- Cho, T. (2011). Knowledge management capabilities and organizational performance: An investigation into the effects of knowledge infrastructure and processes on organizational performance. University of Illinois at Urbana-Champaign.

- Dabestani, R., Taghavi, A., & Saljoughian, M. (2014). The relationship between total quality management critical success factors and knowledge sharing in a service industry. Management and Labor Studies, 39(1), 81-101.

- Dawes, S.S. (2008). The evolution and continuing challenges of e?governance. Public Administration Review, 68(s1), S86-S102.

- Duarte, P.A.O., & Raposo, M.L.B. (2010). A PLS model to study brand preference: An application to the mobile phone market. In handbook of Partial Least Squares (pp. 449-485).

- Dyer, L., & Reeves, T. (1995). Human resource strategies and firm performance: What do we know and where do we need to go? International Journal of Human Resource Management, 6(3), 656-670.

- Fornell, C., & Larcker, D.F. (1981). Evaluating structural equation models with unobservable variables and measurement error. Journal of Marketing Research, 18(1), 39-50.

- Gholami, M.H., Asli, M.N., Nazari-Shirkouhi, S., & Noruzy, A. (2013). Investigating the influence of knowledge management practices on organizational performance: An empirical study. Acta Polytechnica Hungarica, 10(2), 205-216.

- Gloet, M. (2006). Knowledge management and the links to HRM: Developing leadership and management capabilities to support sustainability. Management Research News, 29(7), 402-413.

- Guest, D.E. (2011). Human resource management and performance: Still searching for some answers. Human Resource Management Journal, 21(1), 3-13.

- Gurbuz, S., & Mert, I.S. (2011). Impact of the strategic human resource management on organizational performance: Evidence from Turkey. The International Journal of Human Resource Management, 22(8), 1803-1822.

- Ha, S.T., Lo, M.C., & Wang, Y.C. (2016). Relationship between knowledge management and organizational performance: A test on SMEs in Malaysia. Procedia-Social and Behavioral Sciences, 224, 184-189.

- Hair Jr, J., Sarstedt, M., Hopkins, L., & Kuppelwieser, V. (2014). Partial least squares structural equation modeling (PLS-SEM) An emerging tool in business research. European Business Review, 26(2), 106-121.

- Hair, J.F., Anderson, R.E., Black, W.B., Babin, B., & Tatham, R.L. (2006). Multivariate Data Analysis. Auflage, Upper saddle river.

- Hair, J.F., Black, W.C., Babin, B.J., & Anderson, R.E. (2010). Multivariate data analysis: A global perspective: Pearson Prentice Hall.

- Hair, J.F., Ringle, C.M., & Sarstedt, M. (2013). Partial least squares structural equation modeling: Rigorous applications, better results and higher acceptance. Long Range Planning, 46(1-2), 1-12.

- Harel, G., Tzafrir, S., & Baruch, Y. (2003). Achieving organizational effectiveness through promotion of women into managerial positions: HRM practice focus. International Journal of Human Resource Management, 14(2), 247-263.

- Henseler, J., Ringle, C.M., & Sinkovics, R.R. (2009). The use of partial least squares path modeling in international marketing. In New challenges to international marketing (pp. 277-319). Emerald Group Publishing Limited.

- Honarpour, A., Jusoh, A., & Long, C.S. (2017). Knowledge management and total quality management: A reciprocal relationship. International Journal of Quality & Reliability Management, 34(1), 91-102.

- Honarpour, A., Jusoh, A., & Nor, K. (2012). Knowledge management, total quality management and innovation?: A new look. Journal of Technology Management & Innovation, 7(3), 22-31.

- Imran, M.K. (2014). Impact of knowledge management infrastructure on organizational performance with moderating role of km performance: An empirical study on banking sector of Pakistan. Information and Knowledge Management, 4(8), 85-98.

- Katou, A.A., & Budhwar, P. (2015). Human resource management and organizational productivity: A systems approach based empirical analysis. Journal of Organizational Effectiveness: People and Performance , 2(3), 244-266.

- Keeble-Ramsay, D., & Armitage, A. (2010). Total quality management meets human resource management: Perceptions of the shift towards high performance working. The TQM Journal, 22(1), 5-25.

- Khilji, S. (2001). Human resources in Pakistan. Human resource management in developing countries. Routledge, London.

- Kongpichayanond, P. (2013). Perceived relationships among knowledge management, total quality management, and organization innovation performance: A Thai study.

- Krejcie, R.V., & Morgan, D.W. (1970). Determining sample size for research activities. Educational and Psychological Measurement, 30(3), 607-610.

- Lam, C.H., Tan, P.S.H., Fong, C.Y., & Ng, Y.K. (2011). The effectiveness of HRM and KM in innovation performance: A literature review and research agenda. International Journal of Innovation and Learning, 9(4), 339-351.

- Liu, N.C., & Liu, W.C. (2014). The effects of quality management practices on employees' well-being. Total Quality Management & Business Excellence, 25(11-12), 1247-1261.

- Loke, Y.K., Cavallazzi, R., & Singh, S. (2011). Risk of fractures with inhaled corticosteroids in COPD: systematic review and meta-analysis of randomized controlled trials and observational studies. Thorax, 66(8), 699-708.

- Maruf, A., & Raheem, O. (2014). Effects of human resource management practices on financial performance of banks. Transnational Journal of Science and Technology , 4(2), 1-16.

- Maseki, C. (2012). Knowledge management and performance of commercial banks in Kenya Charity Maseki. A research project submitted in partial fulfilment of the requirements for the award of the Degree of Master of Business Administration (Mba), School of Business, and University.

- Miartana, I.P., & Hadiwijoyo, D. (2014). Implementation of total quality management based knowledge management and its effect on customer satisfaction and organization performance (Studies on Four and Five Star Hotels in Bali), 6(24), 98-108.

- Nawab, S., Nazir, T., Zahid, M.M., & Fawad, S.M. (2015). Knowledge management, innovation and organizational performance. International Journal of Knowledge Engineering-IACSIT , 1(1), 43-48.

- Nawaz, M.S., Hassan, M., & Shaukat, S. (2014). Impact of knowledge management practices on firm performance: Testing the mediation role of innovation in the manufacturing sector of Pakistan. Pakistan Journal of Commerce and Social Sciences, 8(1), 99-111.

- Nigam, A.K., Nongmaithem, S., Sharma, S., & Tripathi, N. (2011). The impact of strategic human resource management on the performance of firms in India: A study of service sector firms. Journal of Indian Business Research, 3, 148-167.

- Pallant, J. (2011). SPSS survival manual: A step by step guide to data analysis using SPSS Australia.

- Psomas, E.L., & Jaca, C. (2016). The impact of total quality management on service company performance: Evidence from Spain. International Journal of Quality & Reliability Management, 33(3), 380-398.

- Racelis, A.D. (2015). The influence of human resource management practices on firm performance: An exploratory study of Philippine banks.

- Rasula, J., Vuksic, V.B., & Stemberger, M.I. (2012). The impact of knowledge management on organizational performance. Economic and Business Review for Central and South-Eastern Europe, 14(2), 147.

- Schuler, R.S., & Jackson, S.E. (2005). A quarter-century review of human resource management in the US: The growth in importance of the international perspective. Management Revue, 11-35.

- Supriyanto, A.S. (2015). Knowledge management implementation, strategic human resource practices and organizational performance mediated by strategic planning. Business and Management Research, 4(1), 90-98.

- Sweidan, G., Al-Dmour, H., Al-Zu’bi, Z., & Al-Dmour, R. (2012). The effect of relationship marketing on customer loyalty in the Jordanian pharmaceutical industry. European Journal of Economics, Finance and Administrative Sciences , 53, 153-172.

- Talib, F., Rahman, Z., & Qureshi, M.N. (2013). An empirical investigation of relationship between total quality management practices and quality performance in Indian service companies. International Journal of Quality & Reliability Management, 30(3), 280-318.

- Usrof, H.J., & Elmorsey, R.M. (2016). Relationship between HRM and TQM and its Influence on Organizational Sustainability. International Journal of Academic Research in Accounting, Finance and Management Sciences, 6(2), 21-33.

- Vlachos, I.P. (2009). The effects of human resource practices on firm growth. International Journal of Business Science and Applied Management, 4(2), 17-34.

- Wall, T.D., & Wood, S.J. (2005). The romance of human resource management and business performance, and the case for big science. Human Relations, 58(4), 429-462.

- Wood, S., & Wall, T. (2002). Human resource management and business performance.

- Wright, P.M., & Boswell, W.R. (2002). Desegregating HRM: A review and synthesis of micro and macro human resource management research. Journal of Management, 28(3), 247-276.

- Zikmund, W.G., Babin, B.J., Carr, J.C., & Griffin, M. (2010). Business researched methods.