Research Article: 2019 Vol: 20 Issue: 2

Market Discipline and Implicit Deposit Protection Empirical Study on the Regional Development Banks in Indonesia

Lina Risnaeni Ahmad, Universitas Padjadjaran

Erie Febrian, Universitas Padjadjaran

Mokhammad Anwar, Universitas Padjadjaran

Aldrin Herwany, Universitas Padjadjaran

Abstract

Keywords

Market Discipline, Developing Economy, Deposit Insurance, Regional Development Banks, Probit Equation, Reduced Form Equation

Introduction

Market discipline has been proven effective in financial service sectors (Eling, 2012), and particularly for preventing depositor runs. The instrument works using the power of depositors, bond-holders, and shareholders, who will withdraw their deposit, sell their shares related to the bank or will ask for higher return from risky banks (Hosono et al., 2005). Some studies have proved that this approach becomes more and more significant in some countries, since it can help prevent excessive risk taking in banks, e.g., Beyhaghi et al. (2014); Arnold et al. (2016); Aysan et al. (2017), among others.

However, there are several factors determining the effectiveness of the instrument. Deposit insurance has been proven to not only improve risk sharing and prevent bank runs (Niinimäki, 2003), but also discourage banks to take prudential business decisions and make depositors less sensitive to bank risk (Febrian & Herwany, 2011).

In different study, Calomiris & Jaremski (2019) find that when government guarantees deposits, depositors would pay less attention to the bank’s fundamentals and any risk associated to their deposits. Some early works (Demirgüç-Kunt & Huizinga, 2013) have proved that such insensitivity induces banks to be more risk taker, and consequently increases probability of default.

Nevertheless, it is still interesting to investigate whether depositors are sensitive to risk of RDBs, particularly in emerging economy. Despite the insurance from government, depositors should be aware of the capability of financial service authority in the developing economy for ensuring liquidity of the respective bank. In this paper, we conduct empirical investigation on whether depositors in Indonesia are sensitive to the risk of RDBs, while their deposits have been insured for some degree. We limit our study to data on regional development banks in Indonesia which were reported by the Indonesian Financial Services Authority in the 2011-2018 period.

Literature Review

Market Discipline

The concept of market discipline was developed by Berger in 1991. In January 2001, the Bank for International Settlements (BIS) through the Basel Committee for Bank Supervision completed a weakness in the 1988 credit risk regulation, by introducing Basel-based market discipline regulations. Many studies have been carried out to asses the concept and mechanisms of market discipline and their impact on risk-taking behavior in banks before the crisis, during the crisis, and after the crisis. These studies are specifically carried out in developing countries. The results of these studies vary depending on the observation period of economic progress and certain conditions.

Some studies show that market discipline is not effective in preventing banks from taking excessive risks, such as Hasan et al. (2013), among others. VanHoose (2007), which examines the key elements of the Basel II pillar and its relation to previous studies, concludes that the pillars of market discipline do not apply as recommended by academics. The pillar of supervision is also misguided. This finding is in line with the results of Hall et al. (2004) research who find that the realization of market discipline as an instrument of bank supervision is more difficult than expected. Furthermore, based on the results of studies of depositors in Indonesia, Valensi (2003) concludes that the effectiveness of market discipline (Pillar III of Basel II) is still low in developing countries, so she recommends that regulators pay more attention to pillars I and II. Grira et al. (2016) support this conclusion in Islamic banking industry.

However, many studies have also resulted in significant support for the effectiveness of market discipline in preventing excessive risk taking, such as Gup (2004); Murata & Hori (2006); Iyer et al. (2016), among others. Murata & Hori (2006) even show that riskier institutions are only able to attract fewer depositors and are forced to offer higher interest compensation. This indicates the validity of market discipline. Similarly, Caprio & Honohan (2004) state that increasing the role of market discipline will be more beneficial in most developing countries than the pillars of Basel II.

The presence of market discipline is also evident in the era of financial crisis. Santos (2014) finds that depositors request a higher risk premium from riskier banks than safer banks, during the financial crisis. In Russia, Karas et al. (2006) prove that both institutional and individual depositors apply quantitative sanctions to weak banks, especially after the 1998 financial crisis. In addition, Hosono (2005) examines the experiences of 4 Asian countries (Indonesia, Malaysia, Thailand and South Korea) exposed to the crisis, finds empirical evidence that deposit rates are negatively related to bank equity. This illustrates that depositors understand the risks of the bank and are able to identify problem banks.

Similarly, studies of the impact of the banking crisis on market discipline in Argentina, Chile and Mexico in the 1980s and 1990s show that depositors disciplin banks by withdrawing their deposits and asking for higher interest rates (Martinez Peria & Schmukler, 2001). The researchers also find that depositors are more sensitive to the risks of banks in times of crisis. Furthermore, Romera & Tabak (2007) claim that depositors are able to distinguish between well-managed and badly managed banks. The results of this research also prove that depositors discipline banks by withdrawing their deposits or demanding an increase in interest rates during the crisis period.

In the mechanism of market discipline, depositors usually study bank fundamentals. Barajas et al. (2000), who analyze panel data estimates from 1985-1999 in Columbia, prove that depositors preferred banks that have strong fundamental conditions. This kind of bank can profit from the reduced cost of funds and high lending rates. As a result, banks tend to improve their fundamental conditions after being punished by depositors. Rose et al. (2004) examine the relationship between bank risk premiums and risk indicators on financial statements in New Zealand. They conclude that disclosure of the bank's financial statements makes depositors get valuable information and that information is reflected in the interest rates offered by the bank. This finding is consistent with the results of Martinez Peria & Schmukler (2001) research.

However, the success of market discipline in reducing bank risk taking is not automatic. Every economy needs to fulfill certain conditions to successfully enforce market discipline. Llewellyn (2005) finds that much needed to be fulfilled by regulators to be able to increase the effectiveness of market discipline and to ensure that market discipline was not hampered. Yeyati et al. (2004) recognize that certain institutional characteristics in developing countries (such as weak capital markets, aggressive government ownership of banks, greater deposit insurance, less transparency) can weaken the public response against bank risk. They further explain that if systemic risk increases, the substance of information from the bank's fundamental indicators decreases. They also explain that systemic shocks can trigger bank runs, regardless of the fundamentals of the bank. Furthermore, Ioannidou & Dreu (2006) emphasize the importance of risk restrictions per depositors, companion insurance, and deposit insurance systems that are able to maintain incentives for large groups of depositors who are willing and able to run market discipline. De Ceuster & Masschlein (2003) argue that disclosure of more external risk management is a sine qua non (absolute) requirement so that market discipline can function as a regulatory mechanism.

Benink & Wihlborg (2002) suggest regulators to strengthen market discipline through establishing an obligation for banks to issue subordinated debt as part of capital liabilities. Lane (1993) argues that market discipline can function effectively if the following conditions are met: i) the capital market is easily accessible, ii) information about the debtor's available debt position, iii) there is no anticipation of bailout and iv) the debtor effectively responds to signals market. Similarly, Hosono et al (2005) states that effective market discipline requires various institutional structures, including disclosure of data (financial institution performance) and transparency, credible and adequate security network schemes, capital market development, bank activity liberalization, bank privatization, and stable macroeconomic policies. He adds that the government needs to dare to liquidate banks and improve the quality of the legal system and the credibility of the security network scheme.

Another specific issue is the ability of market discipline in resolving moral hazard problems that arise when depositors are less informed about whether bankers monitor projects they fund. Nier & Baumann (2006) conduct a study with panel data across 32 countries and involve observations in 729 banks during the 1993-2000 period. They test the hypothesis that moral hazard exist and market discipline is effective. They find the fact of the existence of moral hazard and that market discipline plays a role in dealing with moral hazard problems.

Deposit Insurance

After the introduction of the connection between Market Discipline with Deposit Insurance by Demirgüç-Kunt & Huizinga (2004), the following literatures prove that deposit insurance is effective in reducing the risk of bank management, including Karas et al. (2010); Kiss et al. (2014); Shy et al. (2014); Demirgüç-Kunt et al. (2015); Aysan et al. (2017), Calomiris & Jaremski (2016), Fungáčová et al. (2017), among others. They empirically prove that insurance is generally effective in lowering bank bankruptcy risk.

Nevertheless, many literatures on banking discusses theory and factual reports about the moral hazard effects of applying deposit insurance. Several studies found that deposit insurance provided incentives for bank management to carry out more risky operations because customer funds were guaranteed by government-owned deposit insurance institutions. Banks choose a portfolio of assets that are low risk if the deposits are not insured. When deposit insurance applies at no cost to the banking industry, banks with risk-neutral characters will invest their entire portfolio into risk assets. But if there is no deposit insurance, the bank will diversify its portfolio to risky assets and less risky assets. On the market side, Febrian & Herwany (2011) found that as the Indonesian government has implemented an implicit deposit insurance since late 1990s, bank customers have been less sensitive to the level of risk in bank operations.

Several other studies prove that the effectiveness of deposit insurance depends on the condition of an economy. Hall et al. (2004) test the sensitivity of deposit interest and excess risk before and after the enactment of the Law on the 1991 Deposit Guarantee Institution (FDICIA). They find that increasing the insured deposit limit will not cause moral hazard, at least in financial institutions and certain economic conditions. The Demirgüç-Kunt & Huizinga (1999) study find that explicit deposit insurance can reveal trade-offs between the benefits of increasing the security of depositors and losses due to a decrease in the disciplinary potential of creditors.

On the other hand, Demirgüç-Kunt & Kane (2001) find many problems in countries that impose explicit deposit insurance without adequate testing and improvements to weaknesses in their supervision systems. Likewise Demirgüç-Kunt & Detragiache (1999) reveal that countries that impose explicit deposit insurance when their banks are not ready will actually experience a banking crisis. This finding is in line with the results of a study by Laeven (2000) which proves that government deposit insurance schemes create moral hazard and other negative motives in insured banks. This applies in countries with weak institutional systems, which are reflected in concentrated private shareholdings. Cull et al. (2002) state that to prevent instability and to support financial sector development, the application of explicit deposit insurance schemes must be supported by an adequate regulatory framework. Kane (2000) argues that the peculiar factors of a country must be considered in the preparation of a country's financial security network scheme, such as the quality of access to information, rules on the realization of contracts with non-governmental institutions, and so on. Demirgüç-Kunt & Kane (2001) recommend that countries with weak institutional quality may not apply explicit deposit insurance.

Deposit Insurance and Market Discipline in Indonesia

In 1998, the monetary and banking crisis hit Indonesia, which was marked by the liquidation of 16 banks and resulted in a decrease in the level of public confidence in the banking system. To overcome the crisis, the government issued several policies including providing guarantees for all bank payment obligations, including public deposits (blanket guarantee). In January 1998, after Presidential Decree No.26/1998, the government established the National Bank Restructuring Agency (IBRA) to manage the Blanket Guarantee scheme. This policy is very important to prevent bank runs from recurring in the following years, because the previous guarantee system did not work effectively.

In its implementation, the blanket guarantee can indeed revive public confidence in the banking industry, but the scope of the guarantee is too broad so that moral hazard arises from both bank managers and the community. The government then replaced the guarantee program with a limited guarantee system to overcome moral hazard problems and to continue to create a sense of security for deposit customers. In 2004, the Indonesian government enacted Law 24/2004 concerning the Deposit Insurance Corporation (DII). With this law, DII officially operated in Indonesia in 2005. DII has guaranteed all types of deposits and savings, including savings accounts, checking accounts, deposit certificates, time deposits and others that are equivalent to those accounts. The coverage ceiling has been reduced to Rp100 million at the end of April 2007.

Problem RDB

In the literature related to the issue of bank conditions that trigger market discipline, academics and researchers disagree over the results of the study. Some studies define bank status as a trigger for market discipline as problem banks, such as Grossman (1992); Wheelock & Kumbhakar (1994); Barr et al. (1995); Khorassani (2000); Ahumada & Budnevich (2001), Canbas et al. (2005) and Febrian & Herwany (2011). Studies conducted in various countries tend to prefer the definition of troubled banks compared to banks failing for the dependent variable considering that it is not easy to find the number of bankrupt banks in an economy.

This study uses the definition set by the Indonesian Deposit Insurance Corporation (regulation number 5/2006). According to Indonesia Financial Service Authority, RDBs are banks with core capital less than IDR 1 trillion. Banks are categorized as problem if NPF of the bank is greater than 5% of all loans. The use of this problematic bank definition is in line with the pattern of research conducted by Valensi (2003) and Febrian & Herwany (2011). Valensi (2003) chose to use the terminology of troubled banks rather than failed banks because generally the banks that were worst in Indonesia almost always got solutions from external parties, the central bank and the Deposit Insurance Corporation, so that depositors did not lose their funds.

Bank Risk and Its Measure

Brewer & Mondschean (1994) define bank risk as the root of variance in yields of related bank shares. Some recent studies define bank risk as the probability of bank bankruptcy based on contributions from several variables, such as in studies conducted by Wheelock (1992); Grossman (1992); Wheelock & Kumbhakar (1994); Park (1995); Khorassani (2000); Febrian & Herwany (2011). These studies use a weighted average of several variables that contribute to bank failure. The variables included include bank fundamental variables (for example, capital / total-asset ratio, financing/total asset ratio, etc.).

Thus, based on recent developments in the study of bank risk, this study uses the definition of bank risk as an empirical weighted average of a number of variables that contribute to the probability of bank bankruptcy, which in turn contributes to the probability of depositors losing part or all of their deposit funds. The equation used is known as Reduced Form Equation. This equation consists of 2 levels of equality. Equation 1 is used to determine the bank risk variable calculation model. Equation 2 is used to measure the sensitivity of the amount of deposits to bank risk.

The Observed Variables

This study examines the effectiveness of market discipline using reduced-form equations that are developed from the previous works conducted by Grossman (1992); Wheelock & Kumbhakar (1994); Park (1995); Honohan (1997); Khorassani (2000); Ahumada & Budnevich (2001) and Febrian & Herwany (2011), among others. In particular, in the second equation, this study will run a regression of some factors considered by the depositors in their deposit decision on the respective bank’s total deposit.

The independent variables on Equation 1 seek to assess the contribution of internal and external factors of a bank to its risk. In this case, most of similar studies assesses risk using ratio of capital-to-asset. If the ratio is low, then the bank is in higher leverage situation, which may lead to an increased bank risk. We then measure the asset quality using ratio of different types of loan, including loans of agricultural, trade, manufacturing, and construction, to total assets. Riskiness of the respective type of loan is expected to vary over time, in spite of the fact that such assets may generally bear higher default risk than may other current assets. Meanwhile, ratio of total security investment to total asset is an ex-ante measure of asset quality.

Another measure of asset quality is the ratio of loan revenue to total revenue. The impact of this ratio to risk is still unclear. Higher loan revenue is positive to a bank standing, but it comes from higher loan. While, the higher is loan, the higher ratio of risky assets to safe assets, which may induce higher probability of bank failure. Furthermore, this may imply that high loan may have a positive impact on the bank risk.

The bank profitability is measured using the ratio of net income to total assets, while the bank's ability to cover short-term liabilities to its depositors is measured using the ratio of liquid assets to total assets. These ratios are expected to have negative impact on bank risk. The influence of the deposit-asset ratio towards the bank risk is unclear. Khorassani (2000) states that when depositors are indifferent to bank risk, the larger is the total deposit, the riskier is the chosen portfolio of assets, thus the higher is the bank risk. Nevertheless, this does not necessarily mean that a lower deposit level results in lower bank risk. Deposits are the cheapest source of funds for banks. When such a source of funds cannot sufficiently meet the banks’ fund need, the banks have to seek other sources of funds that charge higher cost of capital. This lowers profitability of the bank and increases its risk.

This study measures size of a bank and the associated management’s capacity to diversify the bank’s portfolio of asset using the natural log of assets and the number of service office, respectively. Some studies, like Avery & Hanweck (1984); Barth et al. (1985), and Demsetz & Strahan (1995) argue that large banks may not be failed. They interpret size as an indicator of greater liquidity. They believe that the larger the institutions, the greater the ability to alleviate unexpected liquidity problems.

The model includes the charter of a bank to measure impact of the banking regulation on bank risk. Meanwhile, this study assesses the quality of management and the reliability of a bank from its age. Managers of old banks may have gained more lessons learned from their longtime daily operation than may their counterparts in new banks. Thus, it is expected that the longer is age of a bank, the less risky the bank.

This study includes the growth rate of provincial real personal income and the change in provincial unemployment rate in the model to measure the impact of economic atmosphere of the province in which certain bank is located on the associated bank risk. A less favorable economy may put more pressure to the operation of a bank. Therefore, negative growth rate of provincial real personal income and positive change in provincial unemployment rate may increase risk of a bank.

Finally, this study also includes the ratio of the number of banks to the provincial population to reveal the impact of competition on bank risk. The higher is this ratio, the riskier is a bank. In this study, a bank is defined as highly risky bank when it requires fund injection in any form from the central bank or the associated local government or at least it experiences downgraded good-corporate-governance (GCG) index. It is assumed that the impact of the bank’s internal and external factors included in Equation 1 on the bank risk can be seen in t+30. This implies that the depositors, who are considering to deposit their money in a bank, could use the estimated coefficients obtained from Equation 1 to predict the probability of bank experiencing at least one of the risk criteria for periods t+30. This probability is obtained by multiplying the regression coefficients of Equation 1 by the values from t+30. In the next stage, a cross-sectional data set on variable Risk is constructed in every month during the obervation periods. Variable Risk in Equation 2 reflects the sensitivity of depositors to bank risk. It is expected that the more sensitive is the depositor, the higher is quantity of deposits.

To assess the impact of the risk competition effect on deposit, the average bank risk in the particular area is included in Equation 2. According to economic theory, an increase in the average risk of other banks in the particular area will escalate the supply of deposits to bank i, assuming risk of bank i is constant.

To test the impact of personal income on the deposit level, this study includes natural log of area personal income per bank in Equation 2. This variable is expected to be positive. This study also includes the natural log of the number of bank service office and the natural log of the age of each bank in Equation 2 to examine how the size of a bank and its reachability to depositors influence the quantity of deposits. Banks with more service offices and long experience are believed to be able to stimulate more deposits. This study measures the impact of the predetermined interest in the banks on the supply of deposits by including the rate of return on bank deposits {Rdp} in Equation 2. Finally, to see how other banks’ deposit return rate in particular area influence supply of deposit in bank i, the average rate of return across banks in the area (Meanrdp) is included in Equation 2.

Data and Methodology of the Study

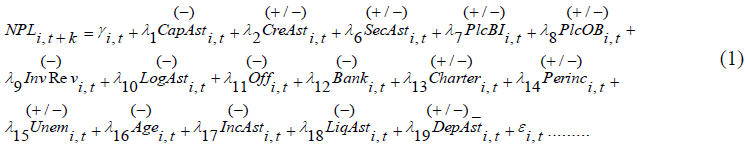

This study employs monthly financial data of 28 RDBs in Indonesia. The data is obtained from Indonesia Financial Service Authority. We conduct analysis using Reduced Form Equation. In this approach, the first model is to calculate risk of each bank using Probit equation and 59-month data in the period of 2011.2 to 2015.12, ending up with 30 estimated risks. Equation 1 was tested to determine the bank risk model, as follows:

Where

- Ratio of total bank capital per aset

- Ratio of total bank capital per aset

- Ratio of total bank credit per asset

- Ratio of total bank credit per asset

- Ratio of total bank securities per aset.

- Ratio of total bank securities per aset.

- Ratio of total bank placement in central Bank per asset.

- Ratio of total bank placement in central Bank per asset.

- Ratio of total bank placement in other Bank per asset.

- Ratio of total bank placement in other Bank per asset.

- Ratio of total credit revenue per total revenue.

- Ratio of total credit revenue per total revenue.

- Log total assets of each bank

- Log total assets of each bank

- Ratio of number of bank office each bank per total bank office.

- Ratio of number of bank office each bank per total bank office.

- Ratio of number of bank per total population in an area, Multiplied by 1,000 (area of metropolitan city, or province).

- Ratio of number of bank per total population in an area, Multiplied by 1,000 (area of metropolitan city, or province).

- Binary variable; 0 for bank operating in more than 1 province and 1 for bank operating in 1 province.

- Binary variable; 0 for bank operating in more than 1 province and 1 for bank operating in 1 province.

- Change in local income per capita.

- Change in local income per capita.

- Change in unemployment rate

- Change in unemployment rate

- Bank age per 1000.

- Bank age per 1000.

- Ratio of bank net income per asset.

- Ratio of bank net income per asset.

- Ratio of bank liquid asset per total asset

- Ratio of bank liquid asset per total asset

- Ratio of bank deposit per asset

- Ratio of bank deposit per asset

The results of this model are then used as exogenus variable in the second model, Multiple Regression Equations. The second model utilizes data from 2016.1 to 2018.12 to reveal the sensitivity of depositors to risk of the observed banks through 36 equations.

In the second model, multiple regression equation is occupied. Equation 2 was tested to examine the impact of several variables on the change in amount of bank deposit, as follows:

where:

- The risk predicted in a bank in the period t+12; calculated from Equation 1

- The risk predicted in a bank in the period t+12; calculated from Equation 1

- Average risk estimated at all banks in a metropolitan or provincial region at the beginning of the period t

- Average risk estimated at all banks in a metropolitan or provincial region at the beginning of the period t

- Rate of return on deposit

- Rate of return on deposit

- Average rate of return on deposit

- Average rate of return on deposit

- The natural log value of the ratio between the value of personal income to the number of commercial banks in a small metropolitan or provincial region

- The natural log value of the ratio between the value of personal income to the number of commercial banks in a small metropolitan or provincial region

- The natural log value of the number of offices in period t.

- The natural log value of the number of offices in period t.

- Natural log value of bank age in period t. Deposit natural log value.

- Natural log value of bank age in period t. Deposit natural log value.

In the first stage of the statistical measurement, i.e., empirical measurement of the sensitivity of depositors to bank risk, the risk needs to be defined, before the regression is run. Khorassani (2000) states that most of studies assessing bank failure use official definition and/or economic definition of a failed bank. For the purpose of this study, the official definition of a failed bank in Indonesia may not be appropriate, since it is bias in reflecting the probability of depositors loosing their money. Indonesian banking regulator has been proven inconsistent in determining whether a bank should be bailed out or closed. For instance, in November 2008, the authorities lowered minimum capital adequacy ratio (CAR) requirement from 8% to 0%, only to help a RDB survive, while a year earlier a slightly bigger bank was closed under the minimum CAR requirement of 8%. In this study we define a bank is at risk if the bank i) receives one of the three central bank’s financial assistance schemes, i.e., Intraday Liquidity Fund (locally known as FPI), Short-term Fund (FPJP), and Emergency Fund (FPD); ii) receives additional capital from the local government to satisfy the minimum CAR; and iii) experiences decline in GCG index.

In the first equation, we conduct a regression of some variables on the binary figure (0 or 1) that reflects that the observed bank is at risk based on the abovementioned criteria. The variables include ratio of capital to total asset (Capast), ratios of loan to total asset (Creast), ratio of security to total asset (Secast), placement in Bank Indonesia (Plcbi), placement in other domestic banks (Plcob), the ratio of total loanof each bank to its total revenue (Invrev), natural log of total asset (Logast), age of bank (Age), number of bank office (Off), income per capita (Perinc), unemployment rate (Unem), the ratio of the number of banks to total population in an area (Bank), charter of a bank (Char), ratio of deposit to total asset (Depast), ratio of net income to total asset (Incast), and ratio of liquid asset to total asset (Liqast).

From the first equation regression, we obtain values of Risk (ertimated risk) that are then included in the second equation regression. In the second stage, we regress the predicted risk, natural log of the ratio of national income per capita to the number of banks nationwide (Lincprbk), return rate on bank deposits (Rdp), natural log of number of bank offices (Lnum), natural log of age of the bank (Lage), on the natural log of total bank deposit (Ldp), to assess the depositor sensitivity.

We conduct the above process using rolling regressions to cope with the short period of data, for the first equation. The variable Risk is obtained by multiplying the regression coefficients by the latest available values of the right hand side variables-namely values from t+30. The series of Risk values along with other independent variables in the Equation 2 are then regressed to the dependent variable, i.e., the natural log of total bank deposit (Ldp). The results of Equation 2 end up with series of multiple regression equations.

Empirical Results and Findings

Table 1 shows the estimated coefficients of the probit model for the observed periods. The obtained equations are appropriate across the rolling periods, as indicated by the average Pseudo R-square ranging from 0.31-0.56. Almost all of the independent variables have significant impact on bank risk, and are consistent with the theory.

| Table 1: Description of Probit Model Estimates:Periods of 2011.2-2015.12 | |||||||||

| Independent Variable | Number of Rolling Periods | Number of Rolling Periods With Insignificant Negative Coefficient (Prob >0.05) | Number of Rolling Periods With Significant Negative Coefficient (Prob <0.05) |

Number of Rolling Periods With Insignificant Positive Coefficient (Prob >0.05) |

Number of Rolling Periods With Significant Positive Coefficient (Prob <0.05) |

||||

| No | Prop | No | Prop | No | Prop | No | Prop | ||

| C | 30 | 6 | 0.200 | 0 | 0.000 | 21 | 0.700 | 3 | 0.100 |

| CAPAST* | 30 | 6 | 0.200 | 18 | 0.600* | 4 | 0.133 | 2 | 0.067 |

| CREAST* | 30 | 3 | 0.100 | 2 | 0.067 | 10 | 0.333 | 15 | 0.500* |

| SECAST | 30 | 7 | 0.233 | 3 | 0.100 | 16 | 0.533 | 4 | 0.133 |

| PLCBI | 30 | 11 | 0.367 | 1 | 0.033 | 14 | 0.467 | 4 | 0.133 |

| PLCOB | 30 | 10 | 0.333 | 2 | 0.067 | 16 | 0.533 | 2 | 0.067 |

| INVREV | 30 | 9 | 0.300 | 0 | 0.000 | 17 | 0.567 | 4 | 0.133 |

| LOGAST* | 30 | 1 | 0.033 | 17 | 0.567* | 6 | 0.200 | 6 | 0.200 |

| OFF* | 30 | 3 | 0.100 | 16 | 0.533* | 10 | 0.333 | 1 | 0.033 |

| BANK | 30 | 13 | 0.433 | 4 | 0.133 | 11 | 0.367 | 2 | 0.067 |

| CHAR* | 30 | 7 | 0.233 | 18 | 0.600* | 5 | 0.167 | 0 | 0.000 |

| PERINC | 30 | 20 | 0.667 | 6 | 0.200 | 4 | 0.133 | 0 | 0.000 |

| UNEM* | 30 | 12 | 0.400 | 1 | 0.033 | 2 | 0.067 | 15 | 0.500* |

| AGE | 30 | 5 | 0.167 | 6 | 0.200 | 15 | 0.500 | 4 | 0.133 |

| INCAST* | 30 | 7 | 0.233 | 17 | 0.567* | 6 | 0.200 | 0 | 0.000 |

| LIQAST* | 30 | 9 | 0.300 | 19 | 0.633* | 2 | 0.067 | 0 | 0.000 |

| DEPAST* | 30 | 11 | 0.367 | 16 | 0.533* | 3 | 0.100 | 0 | 0.000 |

| Pseudo R-square (Average) | 0.39 | ||||||||

| Pseudo R-square (Range) | 0.31 - 0.56 | ||||||||

The Table 2 shows that capast, creast, logast, off, char, liqast, unem, incast, liqast, and depast are risk factors that are significant in more than 50% of the total observed months. This suggests that capital adequacy, bank loan, size, service network coverage, bank charter, unemployment, bank income, sufficiency of liquid asset, and deposit significantly determine risk of the RDBs.

| Table 2: Equation 2 Model: Periods of 2016.1-2018.12 | |||||

| Independent Variable | Number of Periods With Insignificant Negative Coefficient (Prob >0.05) |

Number of Periods With Significant Negative Coefficient (Prob <0.05) | Number of Periods With Insignificant Positive Coefficient (Prob >0.05) | Number of Periods With Significant Positive Coefficient (Prob <0.05) | Average Coefficients Across Periods |

| C | 1 | 10 | 6 | 19 | 2.18 |

| RDP | 5 | 23 | 3 | 5 | -5.08 |

| MEANRDP | 5 | 22 | 9 | 0 | -1.41 |

| RISK | 15 | 2 | 19 | 0 | -0.01 |

| MEANRISK | 11 | 16 | 3 | 6 | 0.03 |

| LINCPRBK | 5 | 5 | 9 | 17 | 0.01 |

| LNUM | 12 | 7 | 10 | 7 | -1.92 |

| LAGE | 21 | 5 | 5 | 5 | 0.04 |

Table 2 shows the result of cross-sectional multiple regressions done through Equation 2 for the banks. The result of 36 regressions reveals that variables rdp, meanrdp, lincprbk and lnum that are significant in more than one-third of the observed periods. Surprisingly, both rd and meanrdp show negative influence on the deposit. The interest rate of RDBs might indicate the real level of risk during the application of deposit insurance. Meanwhile, the negative influence of average interest rate in an area on deposit might signal that the observed bank bore the same risk level as did the other banks in the area. Thus, in this period, depositors tended to observe risk of each bank through bank’s interest rate offer and avoid putting their money in banks offering high interest rate. On the positive side, an increase in personal real income might lead to more deposit.

The Equation 1 is employed to estimate variable Risk for t+30 (e.g, 2016.1-2018.6 for risk at 2013.8). The obtained riak is then used as independent variable in the Equation 2. The results can be seen on Tables 1 and 2.

Discussion

The results of this study found that capital adequacy, bank loan, bank size, service network coverage, bank charter, unemployment, bank income, sufficiency of liquid asset, and deposit significantly determine risk of the RDBs. Some of the above variables are widely known as risk-forming factors in various bank risk literature, such as capital adequacy, bank credit, bank size, unemployment, bank income, liquid assets, and deposit (Haq & Heaney, 2012; Stiroh, 2006; and Ahmad & Arif, 2004). Meanwhile, the scope of operations of RDBs in Indonesia determines the interest in using banking services for prospective bank customers, and in turn, the ability of banks to recruit public funds. This explains the determination of service network coverage, and bank charter against bank risk.

The logarithm of bank risk has a positive effect on the logarithm of deposits in banks. These results are in accordance with the findings of several previous studies, such as Keeley (1990) and Febrian & Herwany (2011). Both studies agreed that deposit insurance had worked effectively to prevent fund withdrawal. Nevertheless, very tight banking competition caused bank charter values to decline. This encourages banks to carry out various activities that actually increase default risk through increasing asset risk and reducing capital.

The government, through the Deposit Insurance Agency (DII), guarantees customer funds held in banks, as long as they meet the applicable provisions, including the provisions on the amount of interest. The literature above shows that the relationship between bank risk and deposit levels is also determined by deposit guarantees. Febrian & Herwany (2011) further stated that banks in Indonesia stimulated the interest of customers with high interest at the time the banks were facing liquidity difficulties. This is mainly due to high banking competition pressure (Jiménez et al., 2013). Empirically, this pattern has proven effective for increasing the level of deposits in Indonesia. DII can safeguard people's motives for using bank services, but it is not effective enough to avoid the public from the impact of excessive bank risk taking.

In addition, this study do not find any relationship between individual income and the level of deposits in the bank. The majority of RDB customers are government employees, who have fixed income and have low risk profiles, and low to middle income private sector employees. Customers tend to have consumption and investment patterns that follow a pattern of growth in family needs, amid slower revenue growth. The implication is that the growth of the family's domestic needs is faster than revenue growth, which suppresses the ability of deposits. Thus, the results of this study are not in line with conclusions of Cheng & Degryse (2010).

On the other hand, the average risk estimated at all banks in a small metropolitan or provincial area at the beginning of a certain period does not affect the level of deposits in the bank. Customers do not have sufficient capacity to accurately calculate the average risk. However, customers usually use intuition to analyze the risk level of banks in their region based on the level of interest rates offered by banks (Febrian & Herwany, 2011). If the interest rate offered is extremely high, prospective depositors will assume that there is a bank's liquidity requirement that must be met.

Finally, bank credibility is relatively more influenced by the asset size than the age of the bank itself. RDBs supported by other related larger company tend to get significant trust from customers, so that the bank's age does not significantly affect their deposit decisions.

Conclusion & Recommendation

Conclusion

Bank customers generally punish banks that run operations that are too high risk or less prudential. They can withdraw their deposits or sell related bank shares. However, this market discipline can be weakened by deposit insurance issued by the National Financial Services Authority or financial support from local governments as bank owners. With deposit insurance, protected customers do not have much stimulation to supervise banks, so bank management is relatively free to carry out high-risk operations.

This study investigates how depositors react to the risk level of regional development banks (RDBs) in Indonesia. Types of banks that are fully supported by regional governments. This study uses monthly data from 26 RDBs operating in Indonesia, which were obtained from the Indonesian Financial Services Authority. We analyze data using Reduced Form Equation. In this approach, the first model is used to calculate the risk of each bank with the Probit equation. At this stage, the analysis uses regional bank data from 2011.2 to 2015.12. The results of this model are then used as exogenous variables in the second model, Multiple Regression Equations. The second model uses data from 2016.1 to 2018.6 to reveal depositors' sensitivity to the risk of RDB.

We find that because deposits are insured, depositors generally do not care about the observed regional development risks of the bank. The RDB market which is dominated by inner stakeholders causes this result. The close traditional relationship between regional development banks and their captive markets has effectively made the market indifferent to bank risks. The depositors also considered level of interest offered by the intended bank and other banks (competitors) in the area in their decision. This indicates that despite that most of depositors are from the bank’s captive market, they are still much interested in potential return from their deposits. However, as some of the observed RDBs are entering larger national market, the strong reliance on the limited captive market will be diminished and the management should pay more attention on other deposit motives.

Recomendation

The study of the effectiveness of market discipline amid the application of insurance insurance can be expanded by considering the quality of customer access to banking information, especially in developing countries. Similarly, future studies on this issue need to consider the impact of information technology on the interaction of banks and customers that can affect the quality of applying market discipline.

End Note

1 The Federal Deposit Insurance Corporation Improvement Act of 1991 (FDICIA), passed during the savings and loan crisis in the United States, supported Basel Pillar 1 (capital requirements) and Pillar 2 (supervisory review) to reduce banks’ risk taking incentives.

References

- Ahmad, N. H., & Arif, M. (2004). Key risk determinant of listed deposit-taking institutions in Malaysia. Malaysian Management Journal, 8(1), 69-81.

- Ahumada, A., & Budnevich, C. (2001). Some measures of financial fragility in the Chilean banking system: An early warning indicators application. Banco Central de Chile.

- Arnold, E. A., Größl, I., & Koziol, P. (2016). Market discipline across bank governance models: Empirical evidence from German depositors. The Quarterly Review of Economics and Finance, 61, 126-138.

- Asli Demirgüç-Kunt, A., & Kane, E. J. (2002). Deposit insurance around the globe: where does it work?. Journal of Economic Perspectives, 16(2), 175-195.

- Avery, R. B., & Hanweck, G. A. (1984). A dynamic analysis of bank failures. Board of Governors of the Federal Reserve System (US).

- Aysan, A. F., Disli, M., Duygun, M., & Ozturk, H. (2017). Islamic banks, deposit insurance reform, and market discipline: evidence from a natural framework. Journal of Financial Services Research, 51(2), 257-282.

- Barajas, A., Steiner, R., & Salazar, N. (2000). The impact of liberalization and foreign investment in Colombia's financial sector. Journal of Development Economics, 63(1), 157-196.

- Barr, R. S., Seiford, L. M., & Siems, T. F. (1994). Forecasting bank failure: A non-parametric frontier estimation approach. Recherches Économiques de Louvain/Louvain Economic Review, 60(4), 417-429.

- Barth, J. R., Brumbaugh, R. D., Sauerhaft, D., & Wang, G. (1985). Thrift institution failures: causes and policy issues. In Federal Reserve Bank of Chicago Proceedings.

- Benink, H., & Wihlborg, C. (2002). The new Basel capital accord: making it effective with stronger market discipline. European Financial Management, 8(1), 103-115.

- Berger, A. N. (1991). Market discipline in banking. In Federal Reserve Bank of Chicago Proceedings.

- Beyhaghi, M., D’Souza, C., & Roberts, G. S. (2014). Funding advantage and market discipline in the Canadian banking sector. Journal of Banking & Finance, 48, 396-410.

- Brewer, E., & Mondschean, T. H. (1994). An empirical test of the incentive effects of deposit insurance: The case of junk bonds at savings and loan associations. Journal of Money, Credit and Banking, 26(1), 146-164.

- Calomiris, C. W., & Jaremski, M. (2016). Deposit insurance: Theories and facts. Annual Review of Financial Economics, 8, 97-120.

- Calomiris, C. W., & Jaremski, M. (2019). Stealing Deposits: Deposit Insurance, Risk‐Taking, and the Removal of Market Discipline in Early 20th‐Century Banks. The Journal of Finance, 74(2), 711-754.

- Canbas, S., Cabuk, A., & Kilic, S. B. (2005). Prediction of commercial bank failure via multivariate statistical analysis of financial structures: The Turkish case. European Journal of Operational Research, 166(2), 528-546.

- Caprio, G., & Honohan, P. (2004). Can the unsophisticated market provide discipline?. The World Bank.

- Cheng, X., & Degryse, H. (2010). The impact of bank and non-bank financial institutions on local economic growth in China. Journal of Financial Services Research, 37(2-3), 179-199.

- Cull, R., Senbet, L. W., & Sorge, M. (2002). The effect of deposit insurance on financial depth: A cross-country analysis. The Quarterly Review of Economics and Finance, 42(4), 673-694.

- De Ceuster, M. J., & Masschelein, N. (2003). Regulating banks through market discipline: A survey of the issues. Journal of Economic Surveys, 17(5), 749-766.

- Demirgüç-Kunt, A., & Detragiache, E. (1999). Financial liberalization and financial fragility. The World Bank.

- Demirgüç-Kunt, A., & Huizinga, H. (1999). Determinants of commercial bank interest margins and profitability: some international evidence. The World Bank Economic Review, 13(2), 379-408.

- Demirgüç-Kunt, A., & Huizinga, H. (2004). Market discipline and deposit insurance. Journal of Monetary Economics, 51(2), 375-399.

- Demirgüç-Kunt, A., & Huizinga, H. (2013). Are banks too big to fail or too big to save? International evidence from equity prices and CDS spreads. Journal of Banking & Finance, 37(3), 875-894.

- Demirgüç-Kunt, A., Kane, E., & Laeven, L. (2015). Deposit insurance around the world: A comprehensive analysis and database. Journal of financial stability, 20, 155-183.

- Demsetz, R. S., & Strahan, P. E. (1995). Historical patterns and recent changes in the relationship between bank holding company size and risk. Economic Policy Review, 1(2).

- Diamond, D. W., & Dybvig, P. H. (1983). Bank runs, deposit insurance, and liquidity. Journal of Political Economy, 91(3), 401-419.

- Eberle, P. B. (1991). Deposit insurance guarantees and bank risk-taking: A model of the banking industry.

- Eling, M. (2012). What do we know about market discipline in insurance?. Risk Management and Insurance Review, 15(2), 185-223.

- Febrian, E., & Herwany, A. (2011). Depositor Sensitivity to Risk of Islamic and Conventional Banks: Evidence from Indonesia. The International Journal of Business and Finance Research, 5(3), 29-44.

- Fungáčová, Z., Weill, L., & Zhou, M. (2017). Bank capital, liquidity creation and deposit insurance. Journal of Financial Services Research, 51(1), 97-123.

- Grira, J., Hassan, M. K., & Soumaré, I. (2016). Pricing beliefs: Empirical evidence from the implied cost of deposit insurance for Islamic banks. Economic Modelling, 55, 152-168.

- Grossman, R. S. (1992). Deposit insurance, regulation, and moral hazard in the thrift industry: evidence from the 1930's. The American Economic Review, 800-821.

- Grossman, R. S. (2001). Double liability and bank risk taking. Journal of Money, Credit and Banking, 143-159.

- Gup, B. E. (2004). The New Basel Capitol Accord: Is 8% Adequate?

- Hall, J. R., King, T. B., Meyer, A. P., & Vaughan, M. D. (2004). Did FDICIA Enhance Market Discipline?.

- Haq, M., & Heaney, R. (2012). Factors determining European bank risk. Journal of International Financial Markets, Institutions and Money, 22(4), 696-718.

- Hasan, I., Jackowicz, K., Kowalewski, O., & Kozłowski, Ł. (2013). Market discipline during crisis: Evidence from bank depositors in transition countries. Journal of Banking & Finance, 37(12), 5436-5451.

- Honohan, P. (1997). Banking system failures in developing and transition countries: Diagnosis and predictions.

- Hosono, K. (2005). Market discipline to banks in Indonesia, The Republic of Korea, Malaysia and Thailand. Proceeding ADBI Conference.

- Hosono, K., Iwaki, H., & Tsuru, K. (2005). Banking crises, deposit insurance, and market discipline: lessons from the Asian crises. In RIETI Discussion Paper Series, 05-E-029.

- Ioannidou, V., & Dreu, J. D. (2006). The impact of explicit deposit insurance on market discipline.

- Iyer, R., Puri, M., & Ryan, N. (2016). A tale of two runs: Depositor responses to bank solvency risk. The Journal of Finance, 71(6), 2687-2726.

- Jiménez, G., Lopez, J. A., & Saurina, J. (2013). How does competition affect bank risk-taking?. Journal of Financial Stability, 9(2), 185-195.

- Kane, E. J. (2000). Designing financial safety nets to fit country circumstances. The World Bank.

- Karas, A., Pyle, W., & Schoors, K. J. (2006). Sophisticated discipline in nascent deposit markets: Evidence from post-communist Russia.

- Karas, A., Schoors, K., & Weill, L. (2010). Are private banks more efficient than public banks? Evidence from Russia. Economics of Transition, 18(1), 209-244.

- Kareken, J. H., & Wallace, N. (1978). Deposit insurance and bank regulation: A partial-equilibrium exposition. Journal of Business, 413-438.

- Keeley, M. C. (1990). Deposit insurance, risk, and market power in banking. The American Economic Review, 1183-1200.

- Khorassani, J. (2000). An empirical study of depositor sensitivity to bank risk. Journal of Economics and Finance, 24(1), 15-27.

- Kiss, H. J., Rodriguez-Lara, I., & Rosa-García, A. (2014). Do social networks prevent or promote bank runs?. Journal of Economic Behavior & Organization, 101, 87-99.

- Laeven, L. (2000). Financial liberalization and financing constraints: evidence from panel data on emerging economies. World Bank, Financial Sector Strategy and Policy Department.

- Lane, T. D. (1993). Market discipline. Staff Papers, 40(1), 53-88.

- Llewellyn, D. T. (2005). Inside the black box of market discipline. Economic Affairs, 25(1), 41-47.

- Martinez Peria, M. S., & Schmukler, S. L. (2001). Do depositors punish banks for bad behavior? Market discipline, deposit insurance, and banking crises. The Journal of Finance, 56(3), 1029-1051.

- Merton, R. C. (1977). An analytic derivation of the cost of deposit insurance and loan guarantees an application of modern option pricing theory. Journal of Banking & Finance, 1(1), 3-11.

- Murata, K., & Hori, M. (2006). Do small depositors exit from bad banks? Evidence from small financial institutions in Japan. The Japanese Economic Review, 57(2), 260-278.

- Nier, E., & Baumann, U. (2006). Market discipline, disclosure and moral hazard in banking. Journal of Financial Intermediation, 15(3), 332-361.

- Niinimäki, J. P. (2003). Maturity transformation without maturity mismatch and bank panics. Journal of Institutional and Theoretical Economics JITE, 159(3), 511-522.

- Park, S. (1995). Market discipline by depositors: evidence from reduced-form equations. The Quarterly Review of Economics and Finance, 35, 497-514.

- Romera, M., & Tabak, B. (2007). Testing for market discipline in the Brazilian banking industry.

- Rose, L., Pinfold, J., & Wilson, W. (2004). Market discipline in New Zealand: Can retail depositors exercise it?.

- Santos, J. A. (2014). Evidence from the bond market on banks too-big-to-fail subsidy. Economic Policy Review, Forthcoming.

- Shy, O., Stenbacka, R., & Yankov, V. (2016). Limited deposit insurance coverage and bank competition. Journal of Banking & Finance, 71, 95-108.

- Stiroh, K. J. (2006). New evidence on the determinants of bank risk. Journal of Financial Services Research, 30(3), 237-263.

- Valensi, M. (2003). The Indonesian Commercial Power Centre and the Existence of Market Discipline.

- VanHoose, D. (2007). Market discipline and supervisory discretion in banking: reinforcing or conflicting pillars of Basel II?. Journal of Applied Finance, 17(2): 105.

- Wheelock, D. C. (1992). Deposit insurance and bank failures: New evidence from the 1920s. Economic Inquiry, 30(3), 530-543.

- Wheelock, D. C., & Kumbhakar, S. C. (1994). The Slack Banker Dances: Deposit Insurance and Risk-Taking in the Banking Collapse of the 1920s. Explorations in Economic History, 31(3), 357-375.

- Yeyati, E. L., Peria, M. S. M., & Schmukler, S. (2004). Market discipline under systemic risk: Evidence from bank runs in emerging economies. The World Bank.