Research Article: 2021 Vol: 25 Issue: 1

The Existence of Day of the Week Effect in Indian Stock Market

Neha Bankoti, Amity University, Tashkent

Abstract

The common observation about calendar anomalies is that, after they are documented and analyzed in the academic literature, they often seem to disappear, reverse, or attenuate. The simple explanation behind this behavior is that investors may have exploited the patterns of previous anomalies in trading behaviors which gradually cause an opposite direction or disappearance of documented anomalies. Therefore an attempt has been made to explore the existence of day-of-the effect in Indian stock market for recent 9 years (From 2010 to 2019).The use of daily data makes it possible to examine the relationship between the changes that occur in stock prices from one trading day to the next and over weekends or, in other words, to study the weekend effect. In particular, it is possible to test whether the rapidity of the process whereby stock prices are formed changes when the market is closed, i.e. whether the process is defined in terms of market time or real time.

Keywords

Calendar Anomalies, Day of the week, Mean Return, ARCH, GARCH, National Stock Exchange (NSE), Bombay Stock Exchange (BSE).

Introduction

Consistent abnormal returns of stocks in the market other than sudden events detected by empirical research are called anomalies, Among number of Stock market anomalies, seasonal anomalies relates to the assumption that a certain pattern of stock Markets, formed on the basis of past stock prices, can be used to predict future prices. If the anomalous pattern is fixed for a specific time period, informed investors can utilize the pattern to earn a risk-free profit by trading these stocks.

Among other seasonal anomalies day-of-the-week effect is most popular anomaly. According to Day-of-the-week effect, expected returns are not same for all the week days. In most of the studies conducted in past years, it is observed that the average return on Monday is significantly negative and is lower than average returns of other week-days. On the other hand, Friday returns are found abnormally high. The returns on Mondays are found to be negative in many studies, which are commonly referred to as the weekend-effect. There are variations in some countries.

Review of Literature

Day of the week effect was first documented by Osborne (1962) in United States (US) stock market, Jaffe & Westerfield (1985) found that in US typically low mean returns are observed on Monday in comparison to the rest of the days of week while mean returns on Friday are observed positive and abnormally higher than the mean returns on other days of the week. Further in US market the well-known Monday effect occurs primarily in the last two weeks of a month.

Wang used a long time series from 1962–1993 for his empirical research. French (1980); Jaffe et al. (1989) reported that the average returns are significantly negative on Monday and these are significantly lower than the average returns for other week-days in US and many other countries of the world. On the other hand, the average returns on Friday are found to be positive and higher than the average returns for the rest of the week. Chan, et al. (2004) observed that the well-known Monday seasonal is stronger in stock with low institutional holdings. Lakonishok & Maberly (1990) documented that the individual investors tend to increase trading activity (especially sell transactions) on Monday. It indicates that Monday effect could be related to the trading pattern of individual investors.

There are some variations in day-of-the-week effect in some countries. Balban (1995), for Istanbul stock exchange and Jaffe & Westerfield (1985) for Australia and Japan found negative and lowest returns on Tuesday rather than on Monday. Negative Tuesday effect was mostly observed in European and Asian countries. Chang, et al. (1998) found that macroeconomic news significantly affect return on different days of the week. Jain & Joh (1988) observed in their study that on Monday liquidity in the market place is lower than other days of the week; they reported that total volume of New York stock exchange (NYSE) is approximately 90% of the average trading volume for Tuesday through Friday. Arsad & Coutts (1996); Bildik (2004) found in his study that if previous week are positive, negative Monday effect disappears. Many hypotheses are suggested by researchers to explain the day of- the-week effect. More prominent among them are:

Information Processing Hypothesis

Miller (1988); Lakonishok & Maberly (1990) observed that during weekdays people are engaged in other activities hence it is relatively tough for all the investors to gather and process information during weekday trading hours. For individual investors weekends provides a convenient, low cost opportunity to reach at investment decisions. Therefore, when market reopens the individual traders might be expected to be more active traders. Although, they may put some buying orders during other days of the week based on the recommendations of stock brokers, but for selling orders they rely on their own analysis. Therefore, the selling pressure exceeds the demand on Monday. On the other hand, the trading volume of institutional investors remains depressed on Monday morning. Osborne in (1962) explains that decrease in institutional trading activity is a consequence of an industry- wide practice of using the early trading hours of Monday as an opportunity to plan strategy for the upcoming week.

Information Release Hypothesis

French (1980); Rogalski (1984); De Fusco (1993); Damodaran (1989) show that firms trend to report bed news on weekends (Friday) and this delayed announcement of bad news might cause the negative Monday effect. Firms and governments generally release good news between Monday and Friday, but wait until the week-end to release bad news. As a result bad news is reflected in lower stock prices on Mondays and good news is reflected in higher stock prices on Friday. However, in an efficient market rational investors should recognize this and should (short) sell on Friday (at a higher price) and buy on Monday at a lower price, assuming that the expected profit more than covers the transactions costs and a payment for risk. This type of trading should then lead to the elimination of the anomaly, since it should result in prices falling on Friday and rising on Monday.

Settlement Regime Hypothesis

Gibbons & Hess (1981); Lakonishok & Levi (1982) reported that the delay in the cash payment for the security can lead to enhancements in the rates of return on specific days due to the extra credit occasioned by the two days of the weekend.

Trading Activities of Investors

Osborn (1962) also predicts a pattern in activities of market participants. Osbern predict that, since individual investors have more time to financial decisions during the weekend, they are relatively more active in the market on Monday. He also predicts that institutional investors are less active in the market on the Monday because Monday tends to be a day of strategic planning. The increase in activity by individuals on Monday, which implies that low trading volume on Monday, is a result of less trading by institutions. However Empirical studies conducted across markets provide differing evidence over the period of time. This might be due to time-varying nature of the stock market returns and significant volatility clustering. Therefore, it has become necessary, from time to time, to conduct empirical studies to investigate the day-of-the-week effects on market returns and volatility, especially in the case of emerging stock markets.

Objective of the Study

To examine the existence of day-of-the-week effect in Indian Stock market.

Hypothesis

The null hypothesis of this study are as follow:

1. There is no significant difference among the mean stock returns for different days of the week.

2. There in significant difference between Monday and other days.

3. There is no significant difference between Friday and other days.

Data and Methodology

In this study presence of Day-of-the week effect has examined on stock return. The study covers a sample period of 9 years from April 2010 to March 2019. The sample data has been collected from the indices of two major stock markets of India- Bombay Stock Exchange (BSE) and National Stock Exchange (NSE). The stock prices are represented by price indices − S&P CNX Nifty Index (hereafter called ‘Nifty’), CNX Nifty Mid Cap Index (hereafter called ‘Nifty Mid cap.’) and CNX Small-cap Index (hereafter called ‘Small-cap’. The closing prices of these indices (in terms of Rs.) at National Stock Exchange of India (NSE) were obtained from its website (www.nseindia.com.) and closing prices of BSE indices were obtained from its website (www.bseindia.com). There were trading on certain weekly closing days (i.e. Saturday and Sunday); these days were excluded from the sample. The data series are log-transformed and differenced to obtain daily index-returns and the stationarity of the data is examined using Augmented Dickey-Fuller (ADF) and Phillips-Perron (PP) unit root tests and the differenced series are found stationary.

The analysis has been divided into two parts – a primary analysis followed by confirmatory econometric modeling. In primary analysis the null hypothesis that the mean return across all the days of the week is not same has been tested. F-test has been used to detect the significance of presence of day-of-the-week effects in index returns. Further we used econometric modeling as confirmative analysis, for this purpose an autoregressive model of returns has been used and the error term has been specified as a GARCH (1, 1) process. The dummy-variable repressors are included in mean and variance equations to examine the presence of day-of-the-week effect. We have examined two week days Monday and Friday which have been very prominent in past studies.

Software Packages

SPSS 16 has been used for the primary analysis of the data. EVIEWS 8 has been used for the econometric modeling. In this study an attempt has been made to examine the presence of the Day of the week effect in Indian stock market.

Results

Primary Analysis

In primary analysis the presence of weekly seasonality in stock returns has been tested using ANOVA. Table 1 Present the difference among average daily returns for all trading days across the weeks at aggregate (index) level for 9 years (2010-2019). Data show the opposite results as of earlier studies as most of the return generated on Monday.

| Table 1 BSE Small and NSE Indices | |||||||

| BSE INDICES | NSE INDICES | ||||||

| BSE Sensex | BSE Mid cap |

BSE Small Cap | NSE NIFTY 50 |

NSE MID CAP | NSE SMALL CAP | ||

| Weekday | |||||||

| x̄ | 0.0007 0.0100 |

0.0009 0.0112 |

0.0012 0.0122 |

0.0007 0.01012 |

0.0029 0.03371 |

0.0009 0.01514 |

|

| Monday | σ | ||||||

| x̄ | 0.000 0.0096 |

0.0001 0.0102 |

0.000 0.01068 |

0.000 0.00972 |

-0.0001 0.01259 |

0.0003 0.01374 |

|

| Tuesday | σ | ||||||

| x̄ | 0.0006 0.0084 |

0.0006 0.0095 |

0.0008 0.01016 |

0.0006 0.00849 |

0.0004 0.01178 |

0.0003 0.01288 |

|

| Wednesday | σ | ||||||

| x̄ | 0.0003 0.0097 |

0.000 0.0099 |

0.0000 0.01045 |

0.0002 0.00981 |

-0.0005 0.0132 |

-0.0004 0.01353 |

|

| Thursday | σ | 0.0002 0.0101 |

0.0002 0.0105 |

-0.0008 0.01108 |

0.0004 0.01026 |

0.0005 0.01309 |

-0.0007 0.01426 |

| x̄ | |||||||

| Friday | σ | 0.354 | 0.637 | 2.23 | 0.33 | 2.136 | 0.875 |

| F-test | |||||||

For Nifty 50 average daily return on Monday is 0.007 which is highest among other days of the week, the similar behavior of the returns can be seen in case of Nifty mid cap and small cap. For BSE indices average daily returns are highest on Monday. However, the differences are statically insignificant. Similarly, for in case of BSE mid cap, highest returns were observed on Monday but mean returns across the different days of the week were not found statistically significant. Surprisingly Negative returns on Friday found for small cap indices of both BSE and NSE however the results are not statistically significant.

Econometric Modeling

The results of statistical tests presented in the preceding section are valid only when the variable under consideration is identically and independently distributed Gaussian variable. However, this assumption is not valid for asset returns because asset returns are found to be autoregressive and usually depict the phenomenon of volatility clustering. Therefore, the true nature of the seasonal anomalies cannot be known unless the adjustment is made for conditional mean and volatility.

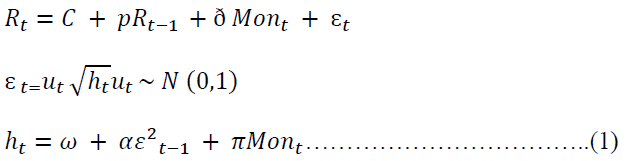

Two popular effects Monday and Friday have been checked through econometric modeling. To check Monday has same trend as in primary analysis we tried to examination of the Monday effect in returns and volatility, one dummy variable representing the Monday is included as follow:

The first line of the above equation is called the mean equation while the third line is called a variance equation. The second line establishes a link between mean and conditional variance. The mean equation signify that the return generating process is assumed to follow AR (1) process; therefore, today’s return is dependent on yesterday’s returns through coefficient ρ. Such dependence is generally observed in empirical research.

In variance equation the conditional variance for a given day ht depends on yesterday’s squared residuals ε2 t-1 through coefficient α and on yesterday’s conditional variance through coefficient β. In this standard GARCH (1,1) model, coefficient α is called the news coefficient while coefficient β governs the persistence of volatility. To ensure consistency in volatility estimation both of the coefficient should be non-negative and their sum must be less than 1.

This standard AR (1)-GARCH (1,1) model is augmented by a dummy variable mont. This is Monday dummy and takes the value of ‘1’ Monday and ‘0’ on other days. In mean equation coefficient δ captures the Monday effect. If this coefficient is positive and significant it implies that the returns on Monday are significantly higher than the returns on other days of the week. On the other hand, if δ is negative and significant it implies that Monday returns are lower than the returns on other week days. A non-significant δ coefficient signifies the absence of Monday anomaly in returns.

Similarly, coefficient π captures the Monday effect in volatility. A positive and significant value of π indicates that volatility increases on Monday while a negative and significant value of this coefficient is an indicator of reduction in volatility on Monday. A nonsignificant value will show absence of Monday effect on volatility. In this specification the Monday dummy is present only in mean equation. A significant value of coefficient δ1 indicates the presence of Monday effect while the positive or negative sign of this coefficient shows whether the volume on Monday is higher or lower than the volumes on other days of the week. Similar econometric models have been used to test other important week days effects that is Friday.

Monday Effect

Table 2 presents the results obtained using equation (4.1) for aggregate market returns (index level) from the year 2010 to 2019. No significant Monday effect was observed for all three BSE indices (Sensex, BSE Midcap and BSE 500). Further same result find out indices that there is no significant Monday effect in the return of NSE indices.

| Table 2 Monday Effect | |||||||||

| Mean Equation | Variance Equation | ||||||||

| Index | Constant | AR | Monday | Constant | α | Monday | Adjusted R2 |

||

| BSE | |||||||||

| Coefficient | 0.0007 | 0.0655 | -0.0001 | -8.04E-0 | 0.05321 | 0.9358 | 9.39E-0 | 0.0026 | |

| t-test | 2.9801** | 2.7615** | -0.3576 | -0.8976 | 6.3813** | 90.8296** | 2.1112* | ||

| coefficient | 0.0007 | 0.1668 | -0.0002 | 4.53E-0 | 0.1156 | 0.8123 | 1.61E-0 | 0.0233 | |

| t-test | 2.5867** | 7.1551** | -0.4429** | 2.1545* | 8.2990** | 33.9742** | 2.3902* | ||

| coefficient | 0.000784 | 0.242301 | -0.001292 | 7.74E-06 | 0.173384 | 0.734146 | 1.85E-05 | 0.0574 | |

| t-test | 2.8635** | 10.4896** | 2.8183** | 3.7677** | 9.8441** | 28.0768** | 2.9159** | ||

| NSE | |||||||||

| S&P CNX nifty 50 | t-test | 0.000549 | 0.06786 | 0.06786 | 1.14E-06 | 0.05883 | 0.92951 | 2.31E-07 | 0.0030 |

| Coefficient | 2.53705* | 2.87867** | 2.87867 | 1.25028 | 6.75338** | 88.0178** | 0.05165 | ||

| Nifty mid 50 Index | t-test | 5.42E-05 | 0.072503 | 0.00367 | 0.000147 | 0.093625 | -0.009064 | 0.000962 | 0.0030 |

| coefficient | 0.162022 | 0.072503 | 3.112804** | 27.92615** | 3.88849** | -2.050508* | 80.96135** | ||

| Nifty small | t-test | 0.000348 | 0.175329 | 0.00096 | 2.51E-05 | 0.146092 | 0.739737 | -1.37E-05 | 0.0288 |

| Coefficient | 0.96795 | 7.097874** | 81.562869 | 5.660433 | 7.967621 | 23.14122 | -1.461012 | ||

In the variance equation, the coefficient of Monday dummy is positive for BSE Sensex and is significant at 1% level. But in case of BSE small cap the coefficient is positive and significant at 5% level. While for BSE midcap the coefficient is not significant.

In case of NSE indices the coefficient of Monday dummy is positive and highly significant for Nifty mid cap and Nifty mid cap and significant at 5% level for S& P CNX Nifty. The positive coefficient in variance equation indicates that the volatility in Market is higher on Monday.

Friday Effect

Table 3, In the mean equation the coefficient of Friday dummy is negative significant at 1%level for BSE mid cap and small call. It indicate that Friday returns are lower and negative than returns of other days, there is no significant Friday effect found in BSE Sensex return. In case of NSE indices although all three indices has negative return on Friday but the result is significant only for NSE mid cap.

| Table 3 Friday Effect | |||||||||

| Mean Equation | Variance Equation | ||||||||

| Index | Constant | AR | Monday | Constant | α | Monday | Adjusted R2 |

||

| BSE | |||||||||

| Coefficient | 0.0007 | 0.0655 | -0.0001 | -8.04E-0 | 0.05321 | 0.9358 | 9.39E-0 | 0.0026 | |

| t-test | 2.9801** | 2.7615** | -0.3576 | -0.8976 | 6.3813** | 90.8296** | 2.1112* | ||

| coefficient | 0.0007 | 0.1668 | -0.0002 | 4.53E-0 | 0.1156 | 0.8123 | 1.61E-0 | 0.0233 | |

| t-test | 2.5867** | 7.1551** | -0.4429** | 2.1545* | 8.2990** | 33.9742** | 2.3902* | ||

| coefficient | 0.000784 | 0.242301 | -0.001292 | 7.74E-06 | 0.173384 | 0.734146 | 1.85E-05 | 0.0574 | |

| t-test | 2.8635** | 10.4896** | 2.8183** | 3.7677** | 9.8441** | 28.0768** | 2.9159** | ||

| NSE | |||||||||

| S&P CNX nifty 50 | t-test | 0.0007 | 0.066 | -1.64E-05 | -7.76E+01 | 0.060277 | 0.926947 | 1.05E-05 | 0.0028 |

| Coefficient | 2.9911** | 2.7880** | -0.0377 | -0.8008 | 6.9124** | 84.9361** | 2.2244* | ||

| Nifty mid 50 Index | t-test | 9.35E-05 | 0.179876 | -0.0138 | 9.00E-05 | 1.425118 | 0.053521 | 0.000188 | -0.13028 |

| coefficient | 0.278 | 9.2784** | -246475** | 13.2150** | 18.5693** | 4.0243** | 5.6529** | ||

| Nifty small | t-test | 0.000659 | 0.174353 | -0.000958 | 1.64E-05 | 0.1452 | 0.73967 | 3.07E-05 | 0.02892 |

| Coefficient | 1.8173 | 7.0996** | -1.5073 | 3.7200** | 7.9497** | 22.4754** | 2.77457** | ||

In variance equation Friday is positive and significant at 5% level for BSE Sensex and Mid cap but there is no significant result for BSE small cap. For NSE indices result is positive and significant for all three indices Nifty, Mid cap and small cap at the level of 5%, 1% and 1% respectively.

Conclusion

The data analysis did not show any evidence of day of the week effect in Indian stock market in recent time period as there is no considerable day-of-the-week effect has been found in stocks return for the period from 2010 to 2019. It can be concluded from the empirical study that in most of the cases null hypothesis that there is no significant difference among the mean stock returns could not be rejected for different days of the week. However In some cases like BSE small and NSE midcap Monday return were positive. Strangely there is negative Friday effect found in mid and small cap indices of both BSE and NSE which insist for further research to find the explanation for such behavior of stock market. This is the area from where this study will be further carried on for the next level of research.

References

- Bildik, R. (2004). Are calendar anomalies still alive?: Evidence from Istanbul Stock Exchange. Evidence from Istanbul Stock Exchange (May 27, 2004).

- Chan, S.H., Leung, W.K., & Wang, K. (2004). The impact of institutional investors on the Monday seasonal. The Journal of Business, 77(4), 967-986.

- Chan, S.H., Leung, W.K., & Wang, K. (2004). The Impact of Institutional Investors on the Monday Seasonal. The Journal of Business, 77(4), 967-986.

- Chandra, A. (2011). “Stock Market Anomalies: A survey of Calendar Effect in BSE-SENSEX”, Indian Journal of Finance, 5 ,1-4.

- Gibbons, M.R., & Hess, P. (1981). Day of the week effects and asset returns. Journal of Business, 579-596.

- Jaffe, J., & Westerfield, R. (1985). Patterns in Japanese common stock returns: Day of the week and turn of the year effects. Journal of financial and quantitative analysis, 261-272.

- Jain, P. & Joh G., (1988). The Dependence Between Hourly Prices and Trading Volume”, Journal of Financial and Quantitative Analysis, 23, 269-284

- Lakonishok, J., & Levi, M. (1982). Weekend effects on stock returns: a note. The Journal of Finance, 37(3), 883-889.

- Lakonishok, J., & Maberly, E. (1990). The weekend effect: Trading patterns of individual and institutional investors. The Journal of Finance, 45(1), 231-243.

- Rogalski, R.J. (1984). New findings regarding day‐of‐the‐week returns over trading and non‐trading periods: a note. The Journal of Finance, 39(5), 1603-1614.